-

Who We Are

- What We Do

Dear Clients,

As I complete my first year at Citadel Securities, I’ve had the pleasure of connecting with many of you. In each interaction, I’ve been gratified by your level of engagement and curiosity about our business.

Going forward, I will reach out periodically to provide insights on major trends impacting our respective businesses. Today, I’ll address a question I’m frequently asked: how does Citadel Securities’ business model compare to traditional bank market makers?

The world is changing rapidly around us. Accelerating technological trends are impacting every company on the planet. As you navigate these changes, our experience and client-centric approach make us a valuable long-term partner.

We’ve become the fintech firm leading the capital markets forward with constant innovation. Built to scale, our platform operates with a relentless focus on reliability and durability, especially in times of volatility when our client market shares tend to increase. Moreover, we automate systems and processes by default with a sharp eye towards rooting out complexity.

All of this is grounded in our ‘origin story’ when, back in the early 2000s, a young Ken Griffin and his partners embraced the leading edge of electronic market making at a time when much of the industry was bogged down under the weight of manual processes. Our origin story defines who we are today.

Citadel Securities’ global scale and operating efficiency, paired with our service-oriented approach, provides our clients a completely differentiated execution experience. We serve institutional investors who require analytical tools, deep liquidity, competitive pricing, and seamless front-to-back execution to transact across a broad array of financial products.

We are a source of unmatched liquidity in three distinct client channels: on-exchange market making, support for retail traders, and direct institutional coverage. The deep liquidity we generate lowers transaction costs for buyers and sellers alike. To serve clients, we execute nearly 25% of all daily US equity volumes. We deliver 25 billion option quotes per day. We transact 35%+ of daily US retail volumes. We rank #1 on Tradeweb for US Treasury flows and command 15%+ market share for block size Investment Grade Credit. 1

How do we achieve this scale with a team of just 1,800 team members around the globe? Of them, 260 hold a PhD, the foundation for our deep analytical problem-solving chops. Leveraging skills in mathematics, statistics, and engineering, we’ve built an industry-leading platform that continuously and simultaneously prices hundreds of thousands of securities across markets and geographies, while warehousing risk to support our clients’ liquidity needs.

We want our clients to benefit not only from our platform, but also from our unique experience and perspective. I am excited that we have added a handful of extraordinary client-facing colleagues to provide more differentiated insights to help inform your market view. Nohshad Shah’s weekend macro note is a must read, as are Scott Rubner’s valuable insights into what market flows imply for future direction (recent examples linked below). While we won’t aspire to be your largest content provider, we strive to be your most valued, giving you unique insights into segments of the market where we have a meaningful presence and a differentiated view.

Looking forward, we endeavor to serve you in more areas as we make further investments in our client franchise across fixed income, in Europe and APAC, and in new products. You’ll also see us accelerate in high touch equities with our recent hire of Elan Luger. We will continue to invest in exceptional talent as we are firmly of the view our best days lie ahead.

Many of you have interacted with our resident experts directly as we bring our technology-first mindset to the systems challenges that our clients face and we welcome further engagement around helping you solve your biggest and most complex problems.

I’m grateful for your trust in Citadel Securities. Together we will navigate this complex world, and its challenges, in a mutually beneficial way. Please don’t hesitate to reach out to me directly, or members of our team, if we can help in any way.

Enjoy the remainder of precious summer. In closing, for fun, a flashback to where it began for me here.

All the best.

Jim Esposito, President

Citadel Securities

SEC Policy Recommendations: Enhancing Competition and Innovation in U.S. Financial Markets

As the SEC’s new leadership formulates its agenda, Citadel Securities provided a detailed series of policy recommendations with respect to equities, options, U.S. Treasuries, credit and digital assets. Across these diverse asset classes, our recommendations are aimed at:

1. Increasing market competition and transparency, and reducing trading costs for investors;

2. Reducing regulatory inefficiencies and unleashing a new wave of innovation; and

3. Ensuring that critical market infrastructure is secure, resilient, and efficient.We are proud to consistently advocate for measures designed to enhance market efficiency, resiliency, competition, and transparency.

Read our policy recommendations here.

A Look Across the Firm

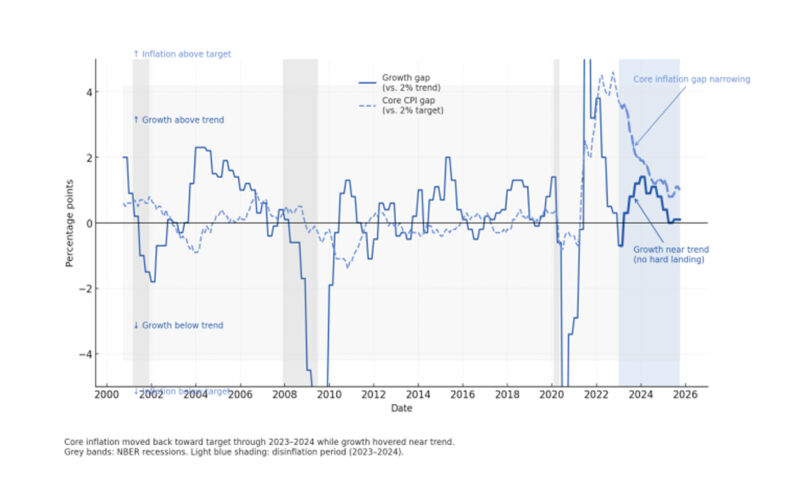

Some Macro Thoughts… This Is Not 2024

Nohshad Shah, Head of Fixed Income Sales – EMEAFront-end rates are inconsistent with cyclically sensitive areas of the equity markets and the forward outlook for US economic growth. Market pricing for the September FOMC shows a 65% chance of a 25bp cut with a total of 50bps still priced for 2025. This looks wrong to me…in the context of stocks which are at all-time-highs (and going higher)…the easiest financial conditions (FCI) we’ve seen in 3 years…an unemployment rate that is going down…and core inflation that remains elevated – with both a weak dollar and incoming tariffs posing a further risk to this.

Read Nohshad’s take here.

Global Market Intelligence – August Views

Scott Rubner, Head of Equity and Equity Derivative StrategySince joining Citadel Securities, I’ve received numerous client inquiries about the same daily markets question: “Is it time to fade the equity market rally?” My response: “We are not there yet.” Retail “buy the dip” behavior in equities and options represents an important dynamic in the U.S. equity market. Low institutional positioning and the return of the corporate buyback bid are important market technicals. I put the current set up in baseball terms – inning 7 out of 9. Institutional investors have some FOMU “Fear of Materially Underperforming” the benchmark indices if earnings come remotely in line and equities rally higher.

Read Scott’s take here.

A Word from Our Tech + Quantitative Research Teams

Testing Google’s Project Starline

Our team recently helped Google, our long-term cloud partner, test use cases for Project Starline, a/k/a Google Beam, a new platform that uses breakthrough 3D video technology designed for true-to-life human connection.

“Google Beam’s 3D communication experience represents the closest digital simulation of an in-person meeting that I’ve ever seen. The real potential is the behavioral impact of the experience. Since you truly feel like you are in the room with someone and can establish eye contact, it demands your full attention, driving higher engagement and focus than a traditional video call.” – Richard Leong, Head of Employee Experience and Technology

Beach Read/Listen

Some recommendations from my colleagues across the firm…

Chart Topping

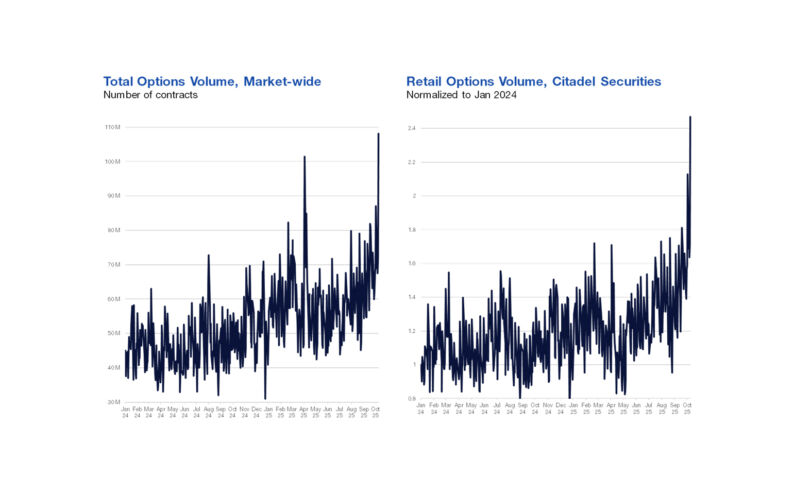

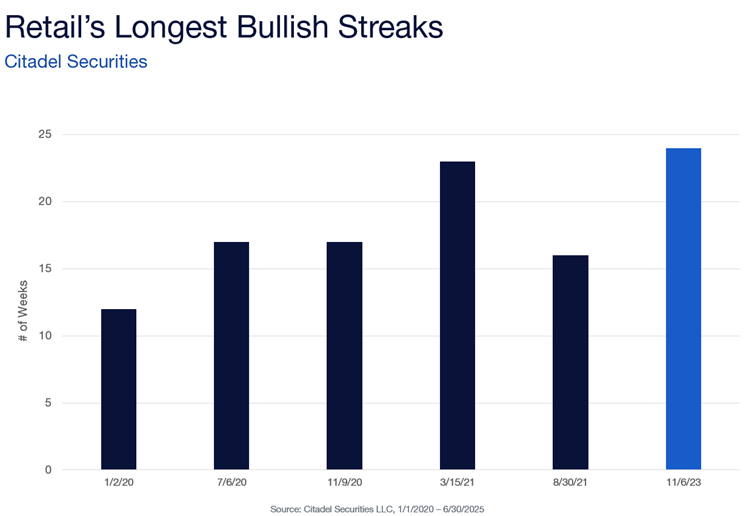

Retail traders are in the midst of one of the longest bullish streaks we’ve ever seen. July 11th marked 11 consecutive weeks of bullish sentiment from retail options traders at Citadel Securities, measured by our Call/Put Direction Ratio*. There have only been 6 other times in our platform’s history with a bullish retail options skew for 10 weeks, and those instances tell us that there could be more in store: These 6 previous streaks have an average duration of 18 weeks. The most recent bull run from November 6, 2023, to April 19, 2024 lasted 24 weeks. In that time, SPX rallied +14%, NDX +12% and GSOX +28%.

Commentary from Allie Becher, Equity Derivative Sales

*Call/Put Direction Ratio takes bullish directional flow (buy call + sell put) relative to bearish directional flow (sell call + buy put).

Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

1 Equities market share measured based on publicly reported total transaction volume averaged over the past 12 months.

Options quotes based on Citadel Securities internal data averaged for trailing 3 months daily quotes sent as of March 31, 2025.

Retail volumes measured based on executed shares for marketable orders publicly reported by direct competitors pursuant to SEC Rule 605 as of May 2025.

US Treasury ranking based on Tradeweb dealer reports for period January 1-July 1, 2025.

Investment Grade Credit market share based on block trades >$5 million and > 7 years duration.Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CDGE”) authorised and regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch authorised and regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the Japan Financial Services Agency (“JFSA”); and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”), Financial Industry Regulatory Authority (“FINRA”), and Securities Investor Protection Corporation (“SIPC”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC, FINRA, and SIPC, or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity. Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at www.citadelsecurities.com/GlobalSalesTrading.

https://www.citadelsecurities.com/privacy/Explore

Market Insights - What We Do