The AI disintermediation narrative is driving macro markets, despite the economic data moving in the opposite direction. We offer some conceptual pushback to this idea at the macro level, and highlight that inflation risks in the near term seem tilted to the upside, largely because of the interaction of AI capex, a decline in immigration and tariffs.

AI Disintermediation Fears Are Dominating Markets

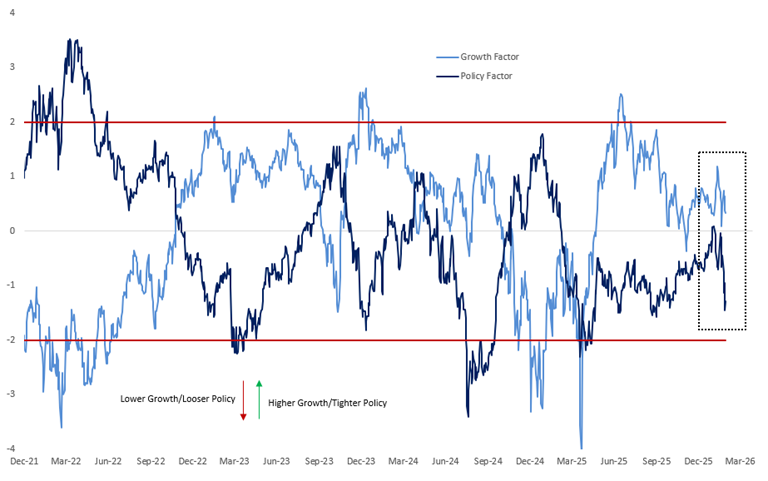

Much has been written in the last two weeks on the risks to employment and inflation from recursive AI and macro markets have repriced in a dovish direction (see the decline in our policy factor below). This repricing comes despite a substantial improvement in labor market data (private payrolls 170k), and a CPI report that implies underlying inflation pressures are stubborn (market based core PCE forecasts >50bp mom). Despite this, macro (and micro) markets have focused on risk of AI disintermediation. The AI disintermediation narrative rests on the idea that recursive (self-improving) AI unlocks non-linear model performance pathways that speed up the timelines over which AI can displace human labor, with parallels drawn to the early days of the pandemic.

FCI Decomposition Demonstrates the Policy Factor is Dominant Driver of Macro Complex

1y Z-Score of PC1 and PC2 of US Financial Conditions

Source: Bloomberg, Citadel Securities, Feb 2026. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

Whilst the market focus here is understandable, we’d highlight two main pushbacks. Firstly, AI performance currently appears to scale sub-linearly with compute – meaning that each incremental improvement in model capability requires disproportionately more compute. In other words, there are diminishing marginal returns to compute. We think that absent imminent breakthroughs that reduce compute intensity, near term scaling of advanced models will increasingly depend on hard infrastructure constraints (compute and power) which are naturally unlikely to autonomously self-scale and therefore could represent real physical bottlenecks to recursive AI expansion at scale.

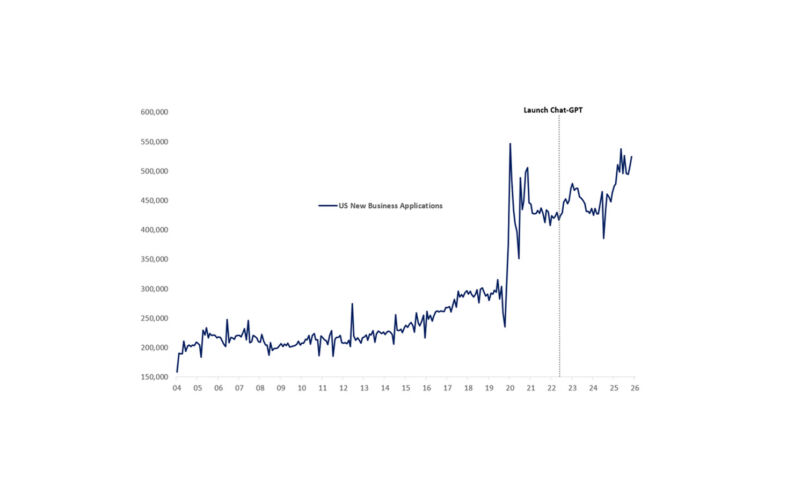

Secondly, markets often approach AI with a fixed pie mentality. Historically, major technological shifts have expanded total economic output – increasing the size of the pie – rather than merely rebalancing labor and capital intensity. The economic data shows that prime working age employment is at historically high levels, new business formation is accelerating and news articles such as IBM plans to triple entry-level hiring this year because of AI serve as some offset to the AI related layoff concerns. Additionally recent research from UC Berkley published in HBR found that “in an eight-month study of how generative AI changed work habits at a U.S.-based technology company with about 200 employees, [researchers] found that employees worked at a faster pace, took on a broader scope of tasks, and extended work into more hours of the day, often without being asked to do so”, implying AI increases task breadth and work intensity, enabling employees to take on a wider scope of activities and operate at higher throughput. We touched on similar themes in Verif-AI-ng the Macro Consensus earlier this year.

There are good reasons for concern with respect to the impact of AI on labor markets and inflation. However we think that the current narrative may have swung too quickly towards AI disintermediation and that both inflation and labor market data is pointing in the opposite direction, at least in the near term. Markets historically struggle to maintain pricing of a narrative in forward space when the spot reality moves in another direction. We see that risk here and think the more immediate story is one of inflation; as a generational capex cycle meets easy financial condition and a procyclical fiscal stimulus, whilst an immigration driven decline in labor supply weighs on trend growth, and tariffs create a vulnerable starting point for a demand driven inflation process.

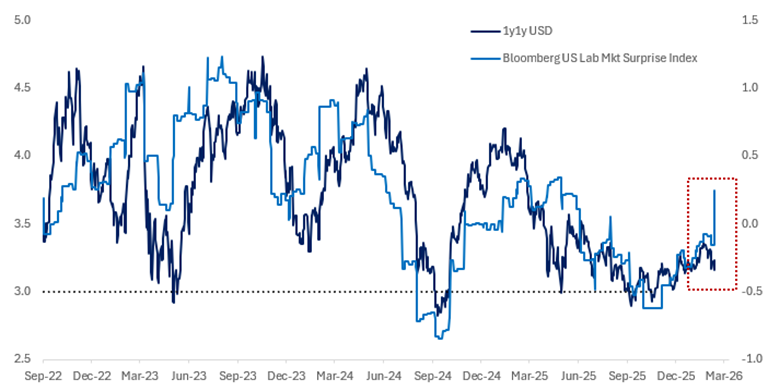

Markets Have Thus Far Ignored the Rebound in the US Labor Market

1y1y SOFR vs Labor Market Surprise Index

Source: Bloomberg, Citadel Securities, Feb 2026. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

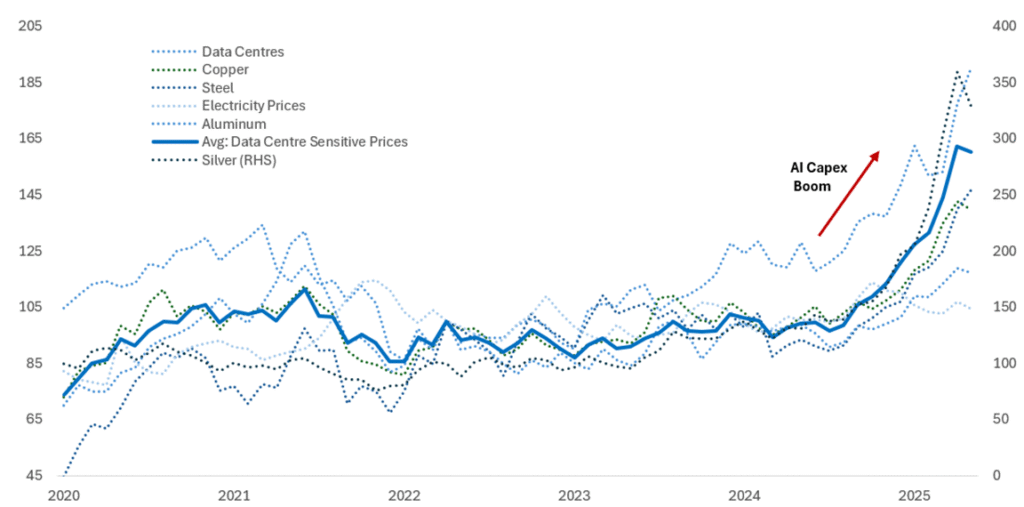

Data Centers, AI Commodities and Construction Workers

The AI capex boom is driving substantial pressures in AI related commodities. We construct a simple index of AI related commodities from futures markets and ETFs and index those prices to 100 in Jan-2023. The index has appreciated 64% since Jan-2025 inclusive of silver and 44% excluding silver.

AI is Already Creating Price Pressures in Commodities

Market Prices for Various AI Related Inputs, Indexed Jan-23 = 100

Source: Bloomberg, Citadel Securities, Feb 2026. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

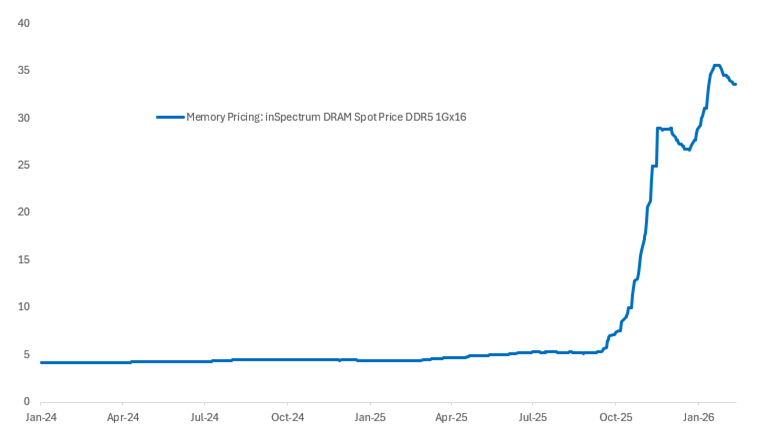

Furthermore, knock on demand from AI appears to have caused a 660% increase in the cost of memory prices since Jan-2025, reminiscent of price increases during the supply bottlenecks following the pandemic. Memory pricing is an intermediate good and so enters CPI through categories like electronic goods, which has just a 1.7% weighting in the basket. However industry expert reporting implies memory now represents 30-40% of a smartphone’s assembly costs, which is a salient cost for consumers.

AI Demand Has Driven Memory Prices Up 660%

Memory Pricing: inSpectrum Tech DRAM Spot Price DDR5 1Gx16

Source: Bloomberg, Citadel Securities, Feb 2026. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

Consumer Electronic Goods Prices are Rising at Similar Pace to 2021

United States, BLS, Import/Export Price Indexes for capital goods, IPI, NAICS, % YoY

Source: BLS, Citadel Securities, Feb 2026. Figures are for illustrative purposes only. Past performance figures do not guarantee future results

Immigration Policy: A Cyclical Amplifier

The data center boom is driving a revival in construction hiring and we expect this to continue. Estimates imply that 2,873 data center projects have been announced in the US. On average each data center requires roughly 1,500 construction workers for 18 months in order to complete construction. This implies that 4.3 million construction jobs will be created in the US by the data center boom. That would suggest average monthly construction employment growth of between 60k-120k jobs per month for the next three years. Naturally we’d expect overlap and substitution effects to absorb some of this pressure, but we think the current market narrative looks at odds with this dynamic.

Data Centre Construction is Boosting Construction Hiring

United States, Employment, Payroll, Construction, SA

Source: BLS, Citadel Securities, Feb 2026. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

Importantly, the data center construction hiring tailwind intersects with the US immigration story, as the construction sector is both highly cyclical and heavily reliant on immigrant labor. Our estimates suggest that roughly 29% of US construction workers are foreign-born, a higher share than in any other industry. With the Trump administration’s border enforcement policies leading to a substantial decline in immigration, the sector is simultaneously facing expanding demand and constrained labor supply, creating upward pressure on wages. The Atlanta Fed wage tracker implies construction wages are running at roughly 5.5%, materially above the aggregate wage tracking. Indeed, wages appear to be accelerating more quickly than the aggregate wage data suggests in many of the immigrant reliant sectors of the economy (chart below). We think the rebound in construction hiring and wages are the leading age of brewing wage pressure in the US, despite the heavy market consensus that the labor market is not a source of inflationary risk.

Wage Growth Accelerating in Immigrant Sensitive Sectors

3mma Wage Growth by Sector

Source: BLS, Citadel Securities, Feb 2026.

Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

The reason we are more concerned about wage pressure in the US economy is because we have been significantly more optimistic on the labor market for some time now, and we continue to expect a rebound in cyclical hiring to persist as uncertainty continues to dissipate and policy tailwinds lift growth. At the same time, current demographic/immigration trends seem to skew towards ongoing pressure on labor supply and a tightening in the labor market should hiring continue to rebound, which could see the unemployment falling below the NAIRU this year. Consider that if our 3% growth outlook were to be proven correct, and trend growth is just 15-25bp below the long run average (1.9-2.0%) in 2026 (as a result of lower labor supply), then the implied output gap could be as large as 1.25%.

Restrictive Immigration Policy is Reducing Trend Growth via the Population Channel

United States, Population Growth and Immigration Estimates

Source: William H. Frey analysis of U.S. Census Bureau population estimates: vintage 2020 and vintage 2025, released January 27, 2026 *July 1 to June 30 of each year, Brookings Institute

Tariff Inflation Creates a Vulnerable Starting Point

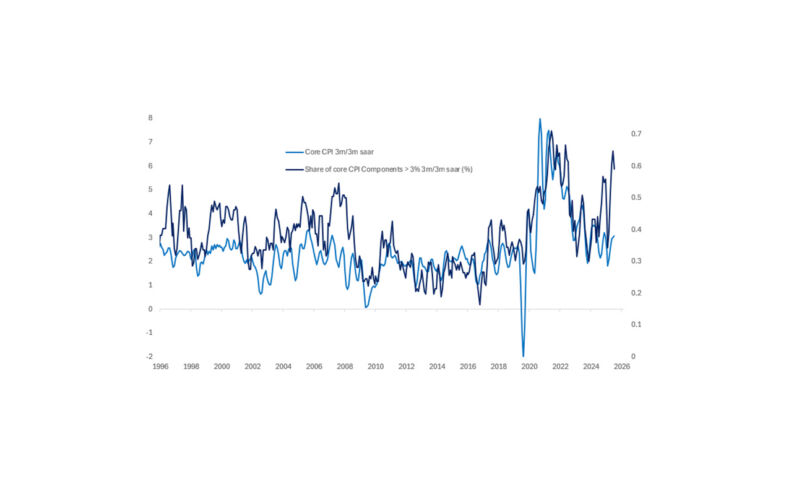

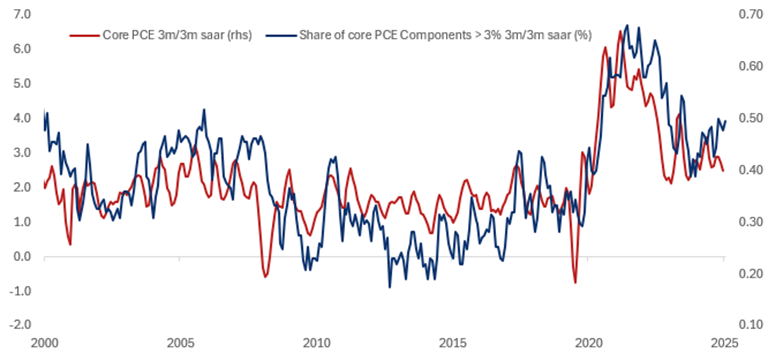

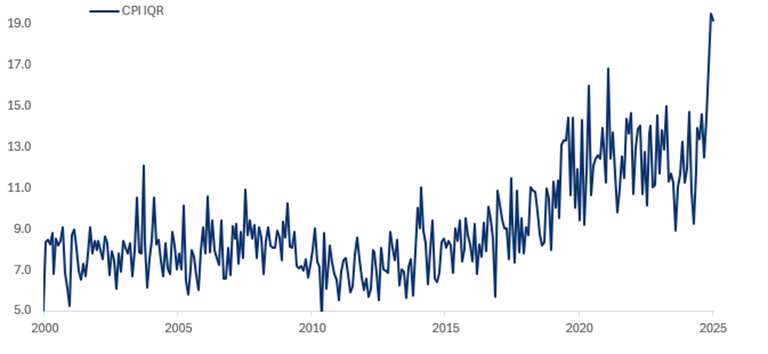

Tariff pass through to CPI has been more moderate but more drawn-out than expected. We noted comments from Amazon CEO Andy Jassy in January that imply inventory depletion is starting to translate into an uptick in product prices. Furthermore, the breadth of inflation – as measured by the share of components running above 3% 3m/3m annualized is reaccelerating and inflation dispersion, as measured by the interquartile range – is the highest its level in 35 years.

Tariffs Create a Vulnerable Starting Point

Share of Core PCE Components >3% 3m/3m SAAR

Source: BLS, Citadel Securities, Feb 2026.

Figures are for illustrative purposes only. Past performance figures do not guarantee future results

Tariffs Create a Vulnerable Starting Point

Interquartile Range of CPI

Source: BLS, Citadel Securities, Feb 2026.

Figures are for illustrative purposes only. Past performance figures do not guarantee future results

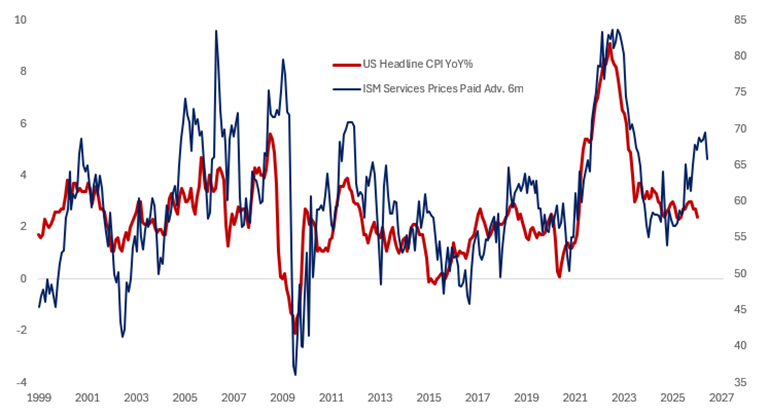

FWD Looking Indicators Show Upside Risk

Headline CPI vs ISM Services Prices Paid

Source: Bloomberg, ISM, Citadel Securities, Feb 2026.

Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

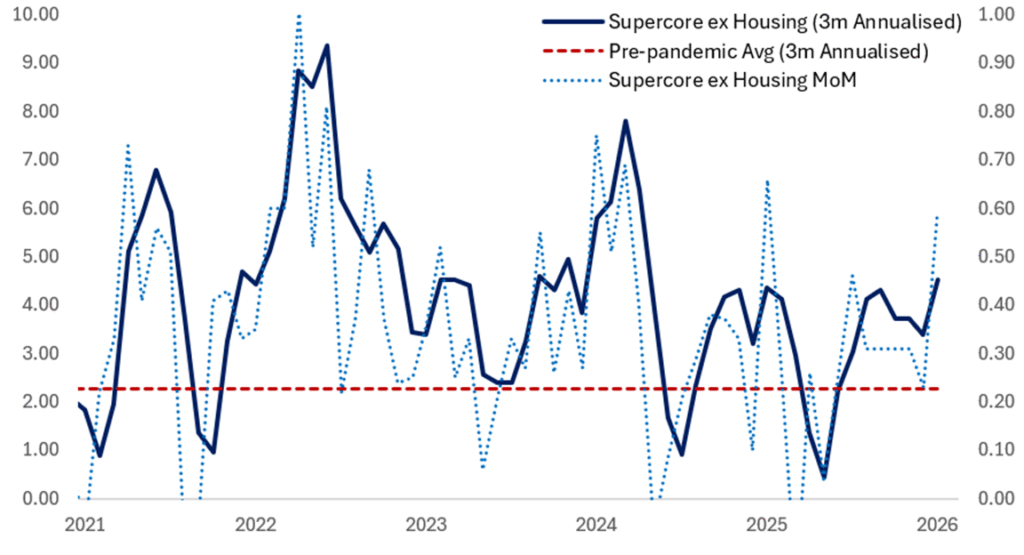

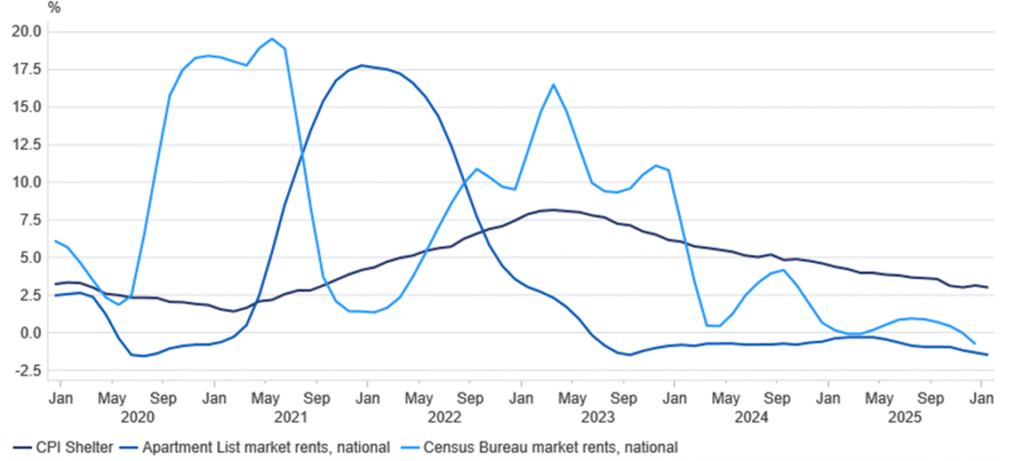

The more dovish interpretation of the inflation process is that ex tariffs core inflation in 2025 would have been circa 2.25%. However, that argument makes no account for how much stronger the labor market and demand driven inflation would have been in 2025 in the absence of the tariff driven uncertainty shock. Furthermore – supercore inflation remains sticky and has shown little progress in the last couple of years. In addition, ongoing disinflation in shelter is the core tenant of most inflation forecasts and yet the Q1 news-flow and fall out from the government shutdown at the end of last year is already causing upward revisions to the shelter forecast profile for 2026, adding yet another delayed to the expected catch down to market rents.

Supercore Inflation Remains Sticky Above Pre-Pandemic Levels

Supercore inflation, MoM SA, 3m Annualised and Pre-Pandemic Avg

Source: BLS, Citadel Securities, Feb 2026. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

Shelter Disinflation Has Been Persistently Slower Than Expected

BLS Shelter Inflation, Apartment List Market Rents, Census Bureau Market Rents

Source: BLS, Apartment List, Census Bureau, Citadel Securities, Feb 2026. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

Conclusion

It appears markets are focused on the medium term impact of AI on jobs and inflation, and a dovish impulse is reverberating around macro markets. However we see the inflation risk profile as skewed to the upside in the near term, as AI capex drives scarcity in AI commodities and data center build out lifts construction hiring. The interaction of the AI capex boom with restrictive immigration policy is a dual edged sword for construction wage inflation, which could easily spread into other sectors as the cyclical pick up in the economy – driven by fiscal stimulus, easing uncertainty and easy financial conditions – meets labor supply constraints and lower than average trend growth. We think this mix results in an inflation inducing output gap.

Copyright © Citadel Enterprise Americas LLC or one of its affiliates. All rights reserved.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CDGE”) authorized and regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch authorized and regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the Japan Financial Services Agency (“JFSA”); and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”), Financial Industry Regulatory Authority (“FINRA”), and Securities Investor Protection Corporation (“SIPC”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC, FINRA, and SIPC, or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity. Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at www.citadelsecurities.com/GlobalSalesTrading.