We are more constructive than consensus on the prospects for a US-Iran deal that reopens the Strait in a timely manner. In markets, we see scope for global duration to rally, while thematic equity sectors such as Retailers, Homebuilders and Airlines could serve as high-beta proxies for a reopening. Central bank pricing can also relax further in Europe, the UK and Australia. While we expect USD rates to participate fully in the initial leg of the rally, we are skeptical that move can be sustained once the dust settles, given accelerating economic fundamentals.

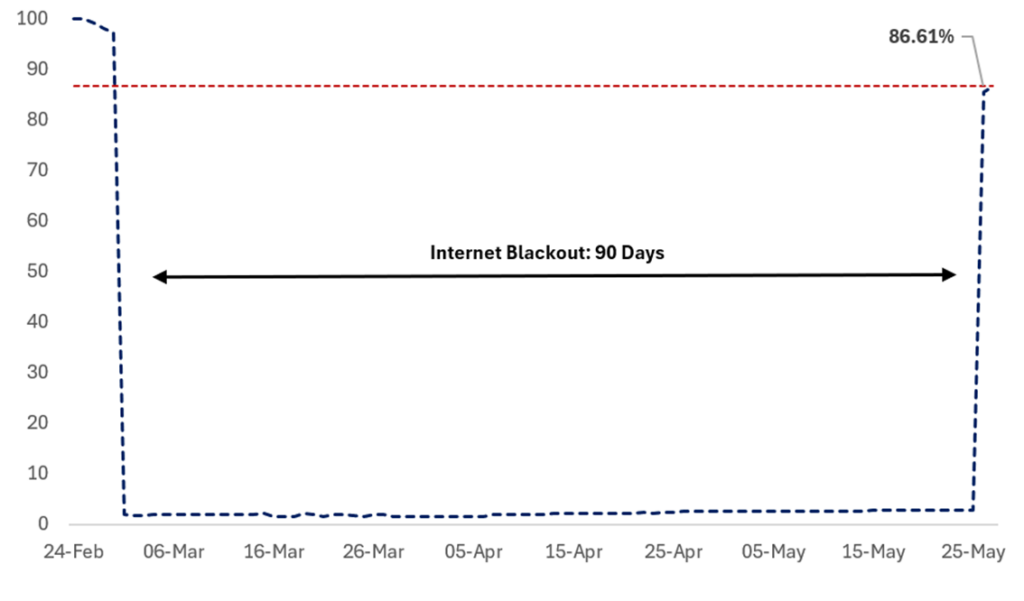

We note two specific sources of incremental conviction that we think hold some edge vs the widely reported progress on negotiations, which point to a significant probability of a permanent US/Iran deal that reopens the Strait of Hormuz quickly: firstly internet connectivity in Iran data has normalized to 86% of pre-conflict levels in recent days, following a 90day blackout initiated at the start of the war. Whilst data is imperfect and internet use remains heavily censored; we think the reports of restoration of connectivity implies the Iran regime expects a conclusion of the conflict is imminent. Secondly, recent public appearances of senior military figures, suggests Tehran may believe the risk of near-term escalation or targeted strikes has fallen, which in turn points to a higher perceived probability that talks between the US and Iran are moving toward a deal.

We think these two factors, alongside widely circulated reports of progress, point to a deal being potentially imminent. We would also expect any memorandum of understanding (MoU) to include a rapid reopening of the Strait of Hormuz, given its strategic importance to the US and the low likelihood that Washington would accept an agreement that left the Strait effectively or partially closed. While it is possible that the two sides are describing the state of negotiations differently, our judgmental lean is that the reported progress may be real and that an MoU including a reopening of the Strait is likely to be announced in the coming days.

Iran Internet Traffic Appears to be Normalizing

Network Connectivity, Iran: Data Digitized from NetBlocks

Source: NetBlocks, Citadel Securities, May26. Figures are for illustrative purposes only.

Market Reaction to Strait Reopening

Naturally, the next question for markets is how much further they can extend on a reopening of the Strait. The timing of the latest headlines is helpful in this respect: reports of progress in the negotiations and of a draft MoU emerged over a holiday weekend, when there was very little other market-relevant newsflow. We can therefore use the change in prediction-market-implied probabilities of a normalization of traffic through the Strait of Hormuz, from the US close on 22nd May to the Asia reopen on 25th May, to benchmark the moves in macro assets and estimate how much further markets could run. On that basis, our estimates suggest that a full reopening of the Strait by end-July would imply a 12.5bp rally in 10y USTs, a 1.71% rally in the S&P 500 and a 0.53% decline in the broad dollar.

This analysis benchmarks to the probability of a full normalization of flows through the Strait by end-July, which we think may prove conservative. If an MoU is announced in the coming days, tanker flows through the Strait could begin to recover quickly, and may even surge in the days immediately following the announcement. In our view, logistical preparations are likely already underway to restore passage as soon as it is formally sanctioned by a US-Iran MoU, which could allow for faster tanker flow than currently priced. Our first principles reasoning here is simple: physical commodity markets are likely to be most stretched at the point of minimum flow, when the marginal deliverable barrel carries the highest scarcity premium. That premium should be largest early in the reopening process, before flows have normalized and inventories have been rebuilt, creating a strong profit incentive for physical traders and cargo owners to move barrels through the Strait as quickly as possible once passage is viable. As those incremental barrels begin to move, physical tightness should start to ease, leaving upside risks to the estimates above for how much markets can normalize if our scenario is realized.

Estimates of Market Moves on Strait Re-Opening

Market Moves Based on Changes in Prediction Market Odds Over Holiday Weekend

Source: Bloomberg, Citadel Securities, May-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

High Beta Thematic Equity Sectors

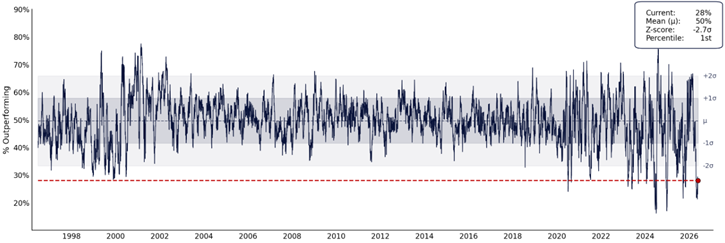

We think the highest-beta equity exposures are sectors with leverage to three related impulses from a Strait reopening: lower oil prices, lower rates and a still-resilient economic backdrop. Retailers, Homebuilders and Airlines could be high beta beneficiaries. A reopening could reduce the effective oil tax on consumers and corporates, lifting real disposable income and easing pressure on energy-intensive cost bases. That is most directly supportive for Retailers and Airlines, where margins and demand are both sensitive to fuel prices and discretionary consumer cash flow. Furthermore, if lower oil reduces inflation risk premium and allows central bank pricing to relax, duration-sensitive sectors should benefit, with Homebuilders a natural focus. These sectors have naturally lagged the AI-led growth complex and may have more catch-up beta if the market rotates away from narrow capex-led leadership toward cyclicals and consumer discretionary exposures, boosted by a relaxation of energy prices amid a resilient macroeconomic backdrop. Importantly, Scott Rubner in his note today flags that breadth remains historically narrow beneath the surface of the rally – just 28% of S&P 500 constituents have outperformed the index over the past 30 trading days, a 1st percentile observation relative to the past 30 years and 67% of the S&P 500’s rally since the end of March has come from just 10 companies. He also notes that investors are beginning to focus to the lagging parts of the index including cyclicals, small caps, financials, industrials, and rate-sensitive sectors, a broadening theme that is consistent with the quicker reopening view we articulate here. Whilst an breath is likely a healthy market dynamic it may come at the expense recent winners in the semis space, and hence poses some risk to momentum.

S&P 500 Breadth – Very Few Names Have Outperformed the Index

Rolling 30-Day Stock Returns – SPX Return, 30-Year Lookback

Source: Bloomberg as compiled by Citadel Securities, GMI, as of May 17, 2026. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

Central Bank Reaction Function

In the global central bank complex, we think the first move under a quick reopening scenario would be for markets to price out energy-shock tightening premium, which could be worth roughly 20 to 25bp in 2026 forwards.

We would expect the BoE and RBA to be firmly on hold in that scenario, the ECB to likely deliver insurance hikes in June and possibly September but with a lower probability of an extended hiking cycle, and the BoJ to move toward a fully priced June hike. For the Fed, we would expect markets to move toward pricing an on-hold scenario through 2026.

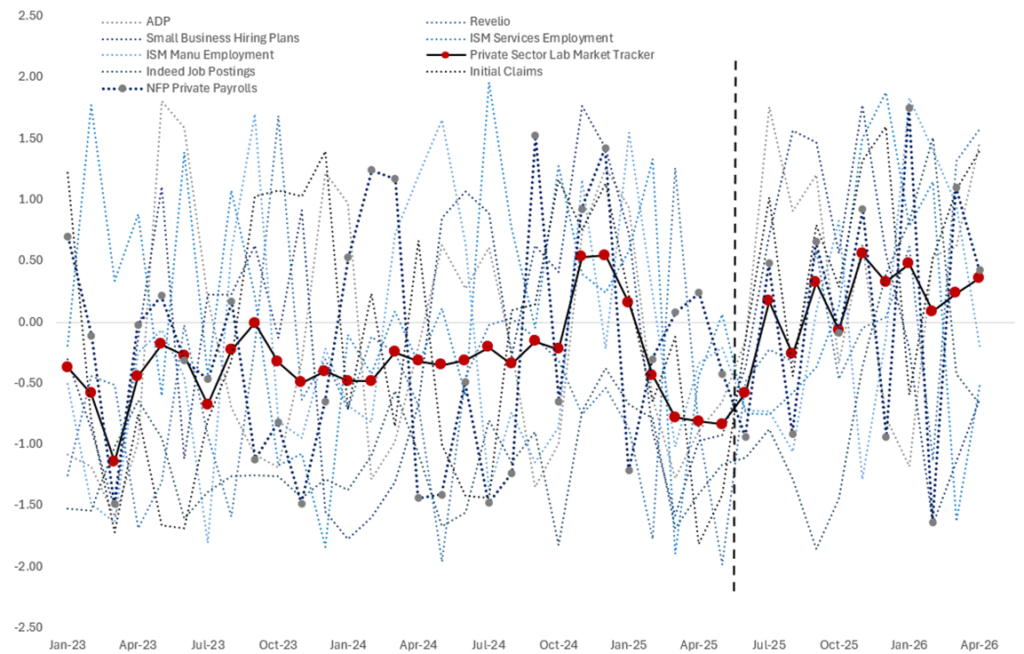

Once the dust settles, however, we think markets are likely to price much greater cross market divergence in 2027 forwards. In Europe and the UK, where the underlying growth and inflation picture appeared relatively benign before the Iran shock, a reopening should allow markets to move back toward pricing cuts in 2027. In the US, by contrast, the collision of accelerating activity data, easy financial conditions, a generational AI capex boom with large economic multipliers, and emerging bottlenecks in compute and data centres leaves the inflation outlook materially more vulnerable. This is particularly true given that our tracking of the US labor market increasingly points to re-acceleration against a constrained labor-supply backdrop, which lowers the threshold for demand growth to translate into a lower unemployment rate and then wage pressure. When the pool of available labor is limited, incremental hiring demand does not need to be especially strong to absorb slack quickly, and that is the channel through which resilient nominal demand can become a more durable inflation problem. We think markets may be underpricing the inflation risk from an improving US labor market, and this can drive hike pricing in the 2027 forwards once the initial reopening rally burns off.

Our US Labor Market Tracking Points to Moderate Acceleration

Citadel Securities Labor Market Tracker, 6m Z-Scores

Source: Bloomberg, Citadel Securities, May-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

Copyright © Citadel Enterprise Americas LLC or one of its affiliates. All rights reserved.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CDGE”) authorized and regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch authorized and regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the Japan Financial Services Agency (“JFSA”); and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”), Financial Industry Regulatory Authority (“FINRA”), and Securities Investor Protection Corporation (“SIPC”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC, FINRA, and SIPC, or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity. Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at www.citadelsecurities.com/GlobalSalesTrading.