Markets appear to be underpricing US growth, particularly relative to Europe. This is most apparent in the valuation of 10y rates both outright and cross market. We continue to think risks to the US labor market are overstated and see upside risk to this week’s US employment data.

Source: Bloomberg, Citadel Securities, Jan-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

We see scope for a material outperformance of US economic activity relative to consensus. Our top down model for 2026 sees US economic growth to be at 2.75% with risks skewed to the upside due to a supportive policy backdrop and a historically significant financial conditions tailwind. Specifically we assume US trend growth is 1.75% (a little lower than its long run average due to restrictive immigration policy) and add the fiscal impulse from OBBBA (50-100bp of GDP) and the FCI impulse which should add 50bp to growth. Hence we see an implied range for US growth of 2.75-3.25%, and with inflation likely stuck around its underlying trend of 2.75% then US nominal growth is likely to be close to 6% this year. We continue to think that market and policy maker fears around the US labor market are misplaced, we wrote back in Q4 of last year that there were tentative signs that the US labor market was improving following the tariff driven uncertainty shock last year. We now think the US labor market is on a solid footing, and that the improvement in the US economic trajectory will support cyclical hiring. On the flip side, we see risks that European growth disappoints somewhat relative to consensus due to international export competition, tight financial conditions, and the risk that the disbursement of German fiscal spend is somewhat slower than markets anticipate. We therefore expect to see US duration underperform on a cross-market basis as divergent economic realities are priced in.

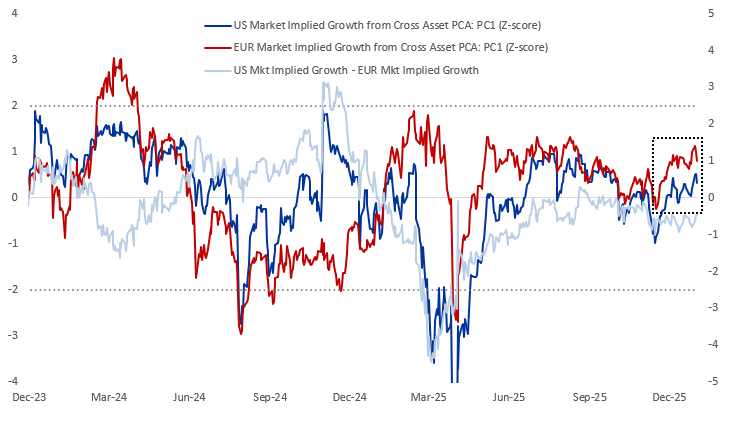

Our X-Asset Macro Framework Suggests More Room to the Topside in US Growth Pricing Relative to EUR |

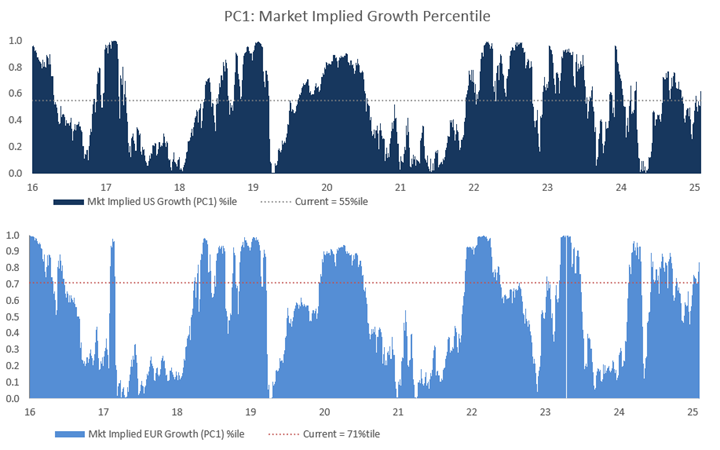

We use a principal components analysis to extract the common signal from major US and European macro assets across rates, FX, credit and equities (index level + internals). We apply a sign restriction such that higher equity prices and bond yields result in a higher first principal component and infer from the factor loadings that the first principal component represents market implied growth in each region. We plot market implied growth for the US and Europe to demonstrate how cross asset market pricing has evolved relative to its own history (rather than level). We find that European growth pricing sits at the 71st percentile relative to US growth pricing which sits at just the 55th percentile (10y history). This tends to confirm our intuition that the market does not appropriately discount the upside to US growth and implies a relatively higher bar for European growth to outperform market pricing.

Source: Bloomberg, Citadel Securities, Jan-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results

Source: Bloomberg, Citadel Securities, Jan-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results

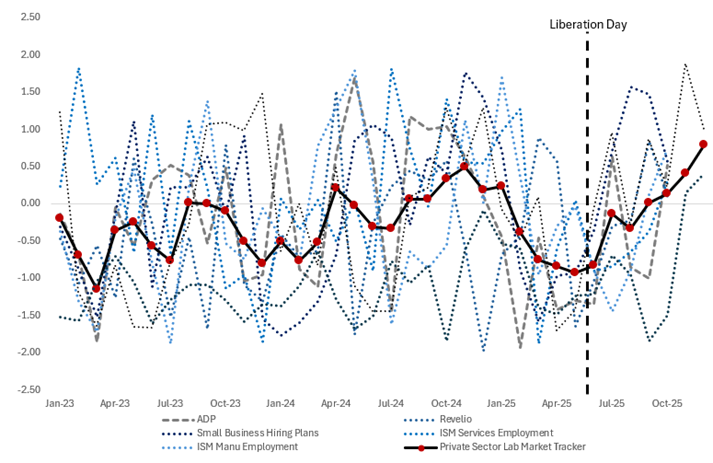

NFP Risks Tilted to the Upside + US Labor Market Recovery Ongoing |

We think Dec NFP will print above the Bloomberg consensus. We run three iterations of our NFP framework and all of them lean to an above consensus print. As a reminder the methodology is a truncated consensus forecasting framework. This is an aggregation approach that deliberately concentrates on the strongest forecasters in a panel rather than treating all contributors equally. The core idea is that forecast panels tend to be highly uneven in quality: a small subset of forecasters typically accounts for most of the predictive value, while the remainder add noise or systematic bias. By ranking forecasters on recent or rolling performance and retaining only the top group, the forecast becomes cleaner, more stable, and more informative. Unlike simple performance-weighted averages that merely down-weight weak forecasters, the truncated approach effectively excludes them, preventing persistent underperformers from influencing the final forecast. The retained forecasters can then be combined using equal or performance-based weights, producing a smart forecast that reflects performance. This type of smart consensus is particularly useful in large, heterogeneous panels where forecast skill is persistent over time. The rolling hit rate of the three models sits in a 60-65% range.

Source: Bloomberg, Citadel Securities, Jan-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

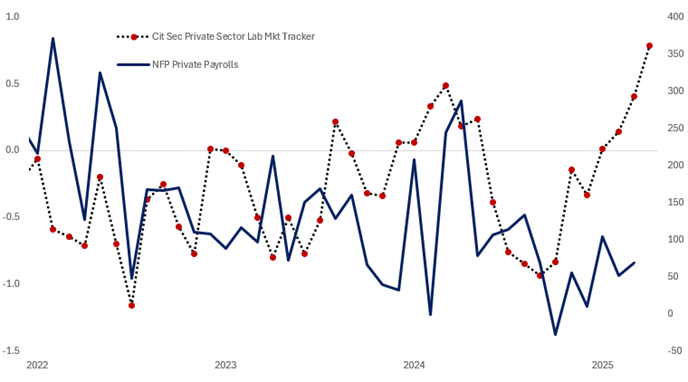

Furthermore our tracking of the US labor market using timely data (that was unaffected by the government shutdown) continues to point to a meaningful improvement. The dispersion of inputs within our tracking has also declined as the tracker has picked up, which reflects the transition from the forward–looking indicators sequentially improving to improvements in data reflective of spot labor market conditions.

Source: Bloomberg, Citadel Securities, Jan-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

US Growth Surprises Not Appropriately Discounted by Front End Rates |

A more simplistic approach to assessing the relative risks to growth pricing in US vs European rates is to simply compare the change in 1y1y forward rates to the evolution of data surprises. The Bloomberg Growth Surprise Index aggregates surprises across a fixed basket of growth-sensitive macro releases, where a surprise is defined as the deviation of the actual print from consensus (normalized by its volatility). These surprises are aggregated using fixed weights and time decay so the index captures the recent momentum of expectation errors. As a result, the index reflects how growth expectations are being repriced at the margin, not whether growth is strong or weak in absolute terms, which makes the index comparable to market levels which shift based on the incoming marginal information. We see that front end US rates have failed to price in the uplift in US growth surprises, whereas the European front end looks fairly valued based on this metric. The reason why it seems the US front end has become detached from the growth outlook is likely twofold: 1) risk premium for a dovish Fed chair is keeping the front end depressed, and 2) concerns around the labor market are dominating the growth outlook for now.

Source: Bloomberg, Citadel Securities, Jan-26 Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

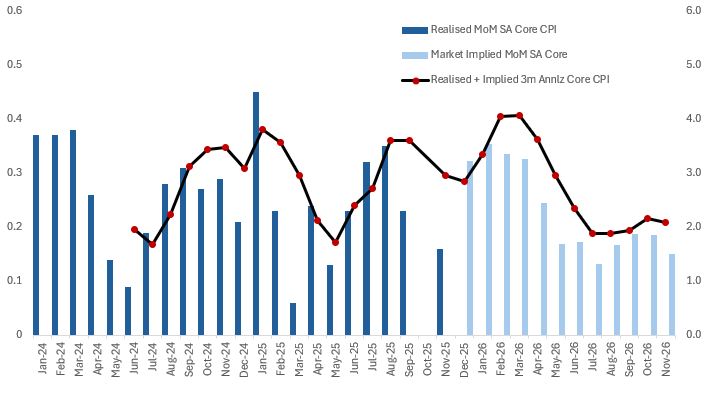

US Inflation Forwards Suggest a Significant Acceleration in 3m Annualized Core |

Markets are sanguine on inflation risks, largely because tariff pass through has been more benign than initially expected and forecasters expect ongoing cooling in shelter inflation to continue to bring inflation lower over the coming year. We would also highlight that methodological changes around the government shutdown have dragged down recent inflation prints, and we expect payback in coming months. However all of this is largely understood by inflation traders and is baked into the inflation fixes. That is why a material acceleration in core inflation is implied by the market pricing of CPI fixes. We can use the market implied core rates to project the path of 3m and 6m annualized inflation, which market pricing implies will peak at 4% and 3.5% respectively in H1 2026. Furthermore, there is a risk that next week’s CPI looks especially elevated due to the payback from technical distortions in last month’s print.

Source: BLS, Bloomberg, Citadel Securities, Dec-25. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

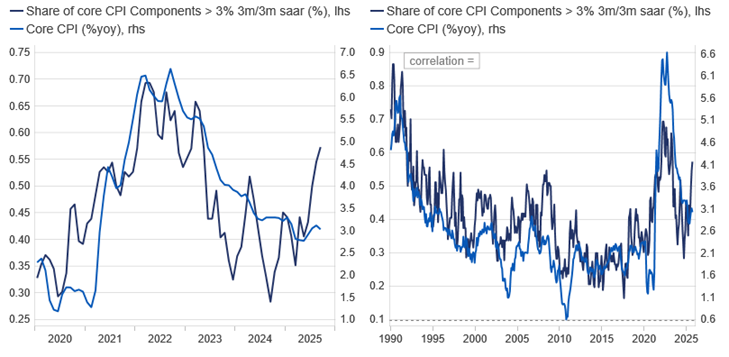

The market prices this inflation acceleration with a relatively low growth forecast and with ongoing concern about the labor market already discounted by markets. If markets move closer to our growth outlook and become less concerned about the labor market, confidence in a return to disinflation after the H1 boost may start to evaporate. Specifically we would point to the moves in precious metals as a potential harbinger of forward inflation pressure, but also note the increase breadth of inflation at a component level and that survey-based indicators of inflation continue to emphasize upside risk, which may not dissipate if we are correct that the output gap in the US economy could be upwards of 100bps this year (2.75% rGDP vs trend at 1.75%).

Source: BLS, Citadel Securities, Dec-25. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

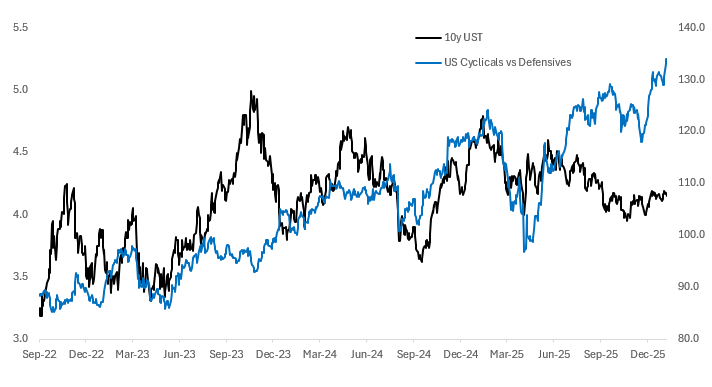

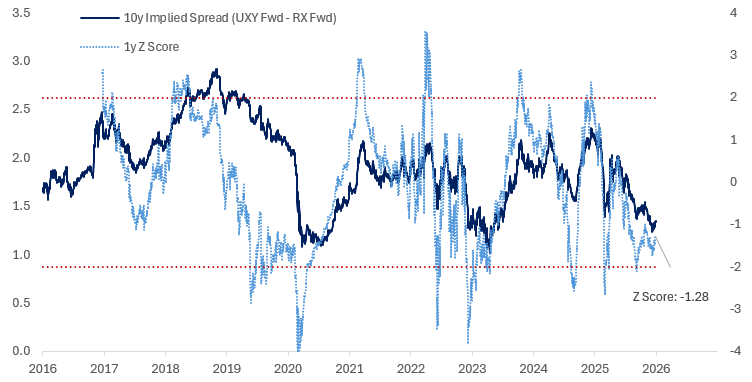

USD vs EUR 10y Cross Market Valuation at Lower End of Range |

Source: Citadel Securities, Dec-25. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

Copyright © Citadel Enterprise Americas LLC or one of its affiliates. All rights reserved.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CDGE”) authorized and regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch authorized and regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the Japan Financial Services Agency (“JFSA”); and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”), Financial Industry Regulatory Authority (“FINRA”), and Securities Investor Protection Corporation (“SIPC”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC, FINRA, and SIPC, or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity. Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at www.citadelsecurities.com/GlobalSalesTrading.