-

Who We Are

- What We Do

Dear Clients,

Peng often reminds me that an organization’s internal rate of change must exceed the external rate of change – or it risks falling behind. Today, AI is accelerating the pace of change across every sector of the economy.

Equity markets are adjusting in real time, repricing businesses as investors weigh both opportunity and disruption. The average SaaS stock has declined 38% over the past 12 months, even as annual recurring revenue has grown approximately 16% over the same period. Markets are working to reconcile sustained growth with rapidly shifting competitive dynamics.

When I wrote about AI in September, I cautioned against unfocused adoption and the risk of generating “work slop” – output that appears productive but delivers little real value. That concern remains. A meaningful gap persists between an impressive demonstration and a production deployment that delivers measurable, repeatable results. Leadership teams must remain disciplined and clear-eyed about that distinction.

At the same time, progress since September has been substantial. Advancements in models and tooling are compounding quickly. Claude’s performance improvements, for example, reflect not only stronger underlying models but also better integration of tools, memory, and workflow design. These systems are demonstrating gains in sustained reasoning, multi-step execution, and domain-specific knowledge application. Similarly, the release of Gemini 3.0 and related tools have driven measurable improvements across knowledge-intensive workflows.

AI is also expanding into increasingly specialized domains, including legal workflows and financial analysis – areas that require precision, contextual awareness, and professional judgment. Innovation cycles in software engineering are accelerating, and productivity gains are likely to place meaningful pressure on incumbent software and services providers. Many believe we are approaching a turning point: a shift from AI as novelty to AI as broadly adopted infrastructure with tangible, real-world impact.

Integration and value capture, however, will take time. Organizations must be deliberate in determining where these tools are reliable and how best to deploy them. Hallucinations remain a real challenge. Yet recent developments have materially shifted expectations about what is achievable in the near term.

Our skills and experience position us well to support you in this rapidly evolving environment. We will continue to share our observations and lessons as we further integrate AI into our capabilities, always with the goal of delivering differentiated value to you. We appreciate the consistent encouragement you provide us to innovate and improve – strong partnerships are built between firms that challenge each other to create meaningful value.

Our vision remains clear: to build a fully integrated ecosystem that delivers advanced content and pre-trade analytics, seamlessly extending through end-to-end execution. We are leveraging our technology to place new applications directly into clients’ hands – combining flow data with interactive experiences and designing mobile-native tools that reduce complexity, enhance decision-making, and integrate naturally into the way you operate.

As always, we look forward to continuing the conversation.

Jim Esposito, President

Citadel Securities

From the Library

🖥️ Google Ironwood: The first Google TPU for the age of inference ✏️ Sandia National Laboratories Not the largest supercomputer, but maybe the most interesting 🖥️ Noahpinion You are no longer the smartest type of thing on Earth 📑 IEEE Computer Society How AI Is Transforming Fraud Detection in Financial Transactions 📰 Fortune Something big is happening in AI – and most people will be blindsided 🎧 Dwarkesh Dario Amodei – The highest-stakes financial model in history 📑 Harvard Business Review AI Doesn’t Reduce Work—It Intensifies It ✏️ Columbia Business School, Kiel University, University of Amsterdam Inefficiencies in the Securities Lending Market Winter Reads, Watches, and Listens

Chart Topping

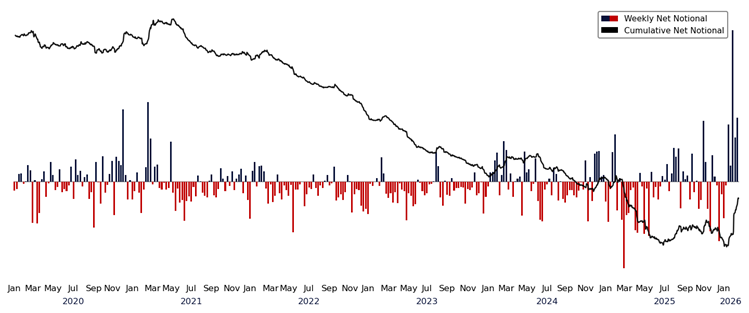

Amid a broader equity market rotation to begin the year – with positioning reset, prior leadership challenged, and unprecedented AI-led capex spending – retail investors have leaned in aggressively into software industry weakness at historically extreme levels.

Year-to-date inflows into software from our retail channel are the largest on record. The chart below highlights weekly net flows alongside the cumulative total, underscoring the unprecedented scale and conviction from retail behind this move.

Retail Cash – Software Industry Net Notional

Weekly, Since 2020

Source: Citadel Securities, GMI, as of February 18, 2026. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

A Look Across the Firm

Some Macro Thoughts | A.I. Versus the Real Economy Narrative

Nohshad Shah, Head of Fixed Income Sales – EMEAThe US labor market is beginning to catch up with the growth outlook… that was the clear signal from this week’s jobs report. Nonfarm payrolls rose +130k, well above expectations (+68k), while the unemployment rate fell below 4.3% (4.28% unrounded). Private payrolls increased a healthy +172k and average hourly earnings rose +0.4%, both meaningfully above consensus. Regular readers will know I have been decidedly bullish on the US growth outlook for some time.

Read Nohshad’s take here.

Global Market Intelligence | February

Scott Rubner, Head of Equity and Equity Derivative StrategyThe January Effect saw robust demand across both retail and institutional channels at Citadel Securities. Heavy capital deployment, active rotation, and elevated participation provided strong early-year support for risk assets, allowing markets to absorb headline volatility without meaningful drawdowns. US equities are at an all-time high today and Citadel securities client flows are hitting records. Citadel Securities retail net cash flows to start the year are off to a record start, running just about 50% higher YTD than the next highest year (2021).

February marks a transition to a more nuanced technical regime. As the initial deployment impulse fades, market focus shifts from the speed of inflows to the durability of support. Selectivity rises, positioning matters more, and flow dynamics become increasingly decisive as the month progresses.

Read Scott’s take here.

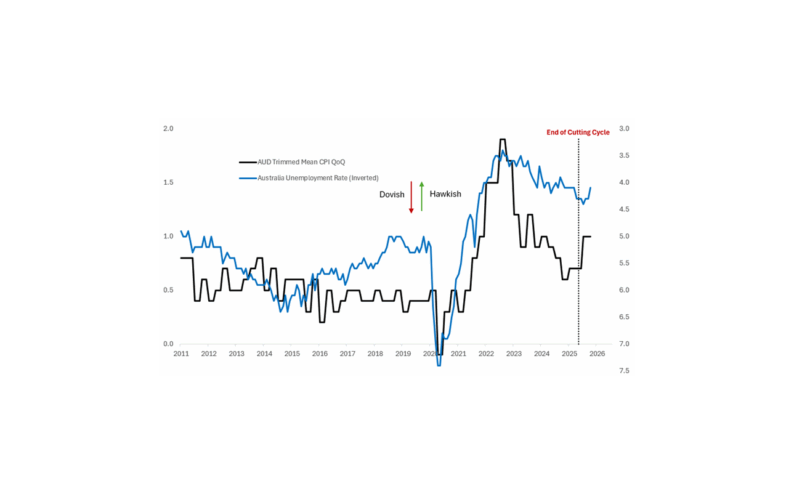

Global Macro Strategy | US Macro Views: Infl-AI-tion Risks

Frank Flight, Macro StrategistThe AI disintermediation narrative is driving macro markets, despite the economic data moving in the opposite direction. We offer some conceptual pushback to this idea at the macro level, and highlight that inflation risks in the near term seem tilted to the upside, largely because of the interaction of AI capex, a decline in immigration and tariffs.

Read Frank’s take here.

1. This material is simply a compilation of otherwise publicly available data, and neither Citadel Securities Corporate Solutions nor Citadel Securities LLC has undertaken any analysis of such information beyond such compilation. This information does not constitute either “Research” or “Investment Advice”, as those terms are defined under the applicable securities laws, and should not be construed as such. Neither Citadel Securities Corporate Solutions is not an investment advisor and makes no recommendation as to the advisability of transacting in any securities or other financial products.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CDGE”) authorised and regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch authorised and regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the Japan Financial Services Agency (“JFSA”); and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”), Financial Industry Regulatory Authority (“FINRA”), and Securities Investor Protection Corporation (“SIPC”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC, FINRA, and SIPC, or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity. Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at www.citadelsecurities.com/GlobalSalesTrading.

Explore

Market Insights - What We Do