Markets need to see safe passage of international ships through the Strait of Hormuz soon, or financial conditions will need to shift focus from inflation to growth risks. We think there maybe scope for global front end rates to rally and are turning neutral on US fixed income having held a short bias for some time.

Our core conviction this year has been that inflation risks were skewed to the upside, and specifically that fixed income markets were not appropriately discounting the risk of an inflation resurgence amid easy financial conditions and a generational AI capex boom. An oil shock was not in our base case. However, the shift in valuations following the Iran conflict implies that markets now discount meaningful inflation risk, and the moves in interest rate markets have generally been consistent with our outlook for unchanged policy rates in the US. As a result, we are turning neutral on US fixed income after leaning short for some time.

In our modal case, we continue to think the Fed will not cut rates this year. However, we see scope for global front ends to rally from here for two reasons. Firstly, if the trajectory of the conflict in Iran skews toward de-escalation, central bank pricing would likely relax meaningfully as the energy outlook improves. Should tanker flows resume through the Strait of Hormuz, markets may begin to price a risk skew for central banks to be on hold or cutting rather than on hold or hiking, even if an inflation acceleration is likely already locked in at this point. Secondly, markets do not appear to be discounting much downside risk in cross-asset growth pricing. If markets begin to price a more drawn-out conflict in which the Strait remains closed, we would expect equities and credit to move materially lower and wider as demand destruction emerges in response to expectations of a more prolonged disruption to global oil and trade flows.

This would materially tighten financial conditions, which in turn would further weaken the growth outlook. That deterioration would likely feed back into risk assets through the risk appetite and volatility channels. These FCI spirals tend to be self-reinforcing and often only end when central banks deliver a circuit breaker in the form of sharp policy easing. At this juncture global front end pricing feels highly conditional on risk and growth expectations holding up relatively well. This in turn is likely conditional on expectations of a quick resolution, although prediction markets imply only around a 60% probability of a ceasefire between the US and Iran by the end of June, enough time to cause material disruption to the global economy.

Relatedly, we do not see $100 per barrel oil as a particularly sustainable equilibrium. Instead, we think the pricing appears closer to a bimodal probability distribution in which oil trades either around $70 or closer to $150. Paradoxically, in the $150 per barrel scenario, rate hikes would likely be less probable than if oil remains near current levels. The reason being that the implications for risk assets and financial conditions would reduce the need for central banks to tighten policy rates, as markets bring forward materially weaker growth expectations. That FCI tightening dynamic would likely weigh on both inflation and inflation expectations.

So far, markets have observably focused largely on the inflationary implications of the Iran conflict and have paid less attention to the growth implications. The echoes of the 2022 energy shock following the Russian invasion of Ukraine likely explain this dynamic. However, the macro backdrop today is somewhat different. The previous shock occurred alongside a large positive demand shock as economies reopened after the pandemic, supported by significant global fiscal easing. While fiscal deficits remain elevated today, the fiscal impulse itself is considerably smaller.

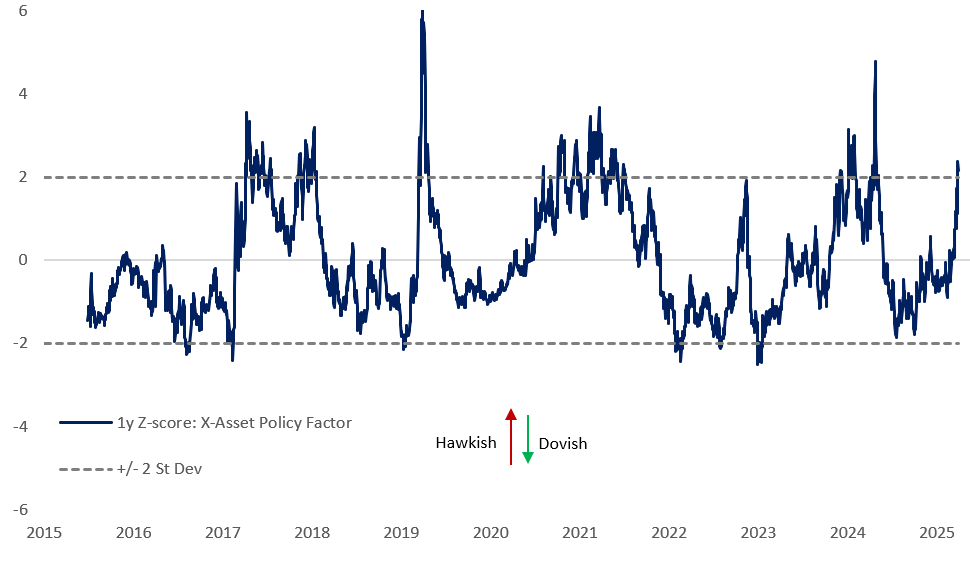

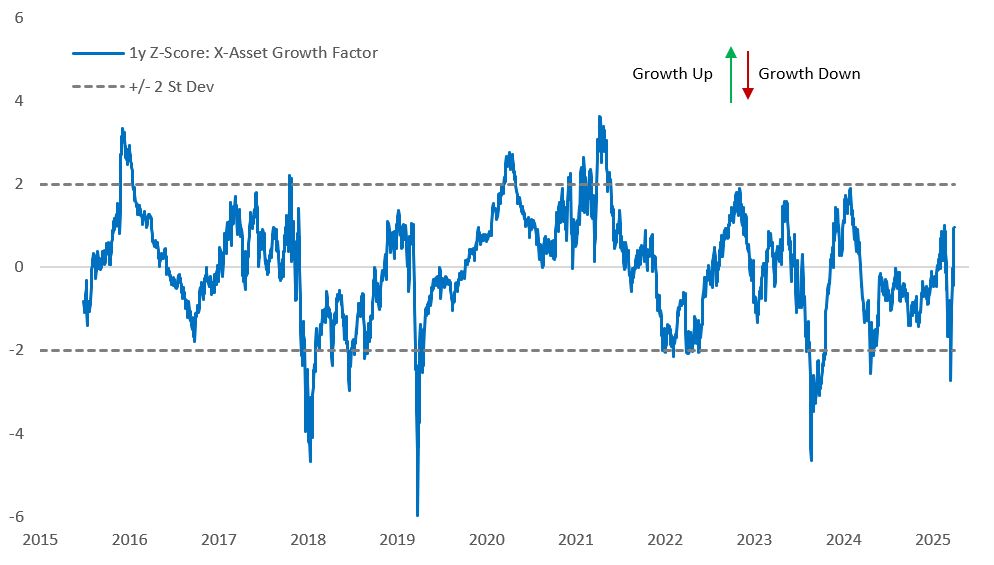

We can quantify the extent to which markets are emphasizing inflation risks over growth risks by turning to our cross-asset framework. This framework decomposes movements in broad financial conditions into their macro drivers, namely growth expectations and policy expectations, using a sign-restricted principal components analysis. The charts below show that the policy factor has tightened materially, now sitting above two standard deviations, while the growth factor remains largely unchanged. Historically, valuations in the policy factor around these levels have tended to mark turning points for markets. Looking back at the limited instances where the policy factor has reached similar valuations, we find that roughly 70% of the time yields are lower one month forward, by around 10bp on average. The growth factor sitting close to unchanged levels suggests a concerning degree of complacency and implies downside risk to equities and credit should the market grow concerned about a more protracted conflict and closure of the Strait.

Cross Asset Policy Pricing is Now Relatively Hawkish

Principal Component Decomposition of Changes in US Financial Conditions, 1y Z-Score

Source: Bloomberg, Citadel Securities. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

Cross Asset Growth Pricing is Largely Unchanged

Principal Component Decomposition of Changes in US Financial Conditions, 1y Z-Score

Source: Bloomberg, Citadel Securities. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

In addition, the localized downside risk we flagged to the February employment report materialized (see “Downside Risks to NFP,” 5 March 2026), and concerns around private credit are likely being amplified as these shocks accumulate on top of one another. As a result, we do not see much left to play for in US fixed income shorts at these valuations. It increasingly feels as though the tails for inflation upside and growth downside are asymmetrically fat.

In our modal scenario, we still expect US policy rates to remain on hold, but we prefer expressing this view through hold-to-maturity option structures. We also note that our above-consensus US growth outlook is now conditional on a quick resolution to the conflict.

The best protection lies in the shape of the curve. The curve should likely steepen if the conflict resolves and the front end relaxes, but it also provides protection if a global recession emerges from a sharp tightening in financial conditions. The moderately inflationary but non-recessionary scenario that flattens the curve appears largely priced. In addition, we think the market could struggle to price rate hikes into the early part of Kevin Warsh’s term. This suggests the curve could bear steepen if inflation accelerates and risk assets remain supported, as well as bull steepen in a downside growth scenario.

Copyright © Citadel Enterprise Americas LLC or one of its affiliates. All rights reserved.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CDGE”) authorized and regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch authorized and regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the Japan Financial Services Agency (“JFSA”); and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”), Financial Industry Regulatory Authority (“FINRA”), and Securities Investor Protection Corporation (“SIPC”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC, FINRA, and SIPC, or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity. Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at www.citadelsecurities.com/GlobalSalesTrading.