-

Who We Are

- What We Do

Series: Global Macro StrategyPolitics & Policy (RBA/BOE/BOJ)

By Frank Flight

Long end JGBs have performed well since we turned constructive earlier in the week, but sustained performance will be more challenging. The UK political outlook remains a headwind to policy rate pricing that – based on the economic data – should look increasingly dovish. We continue to think the RBA is on track for a February rate hike, and market pricing is starting to reflect that following stronger jobs data.

- RBA: Increased Conviction in Our Call for a Feb Rate Hike

- BOE: UK Political Risk Hinders an Increasingly Dovish Outlook

- BOJ: April is Live, Long End JGBs No Longer Technically Stretched

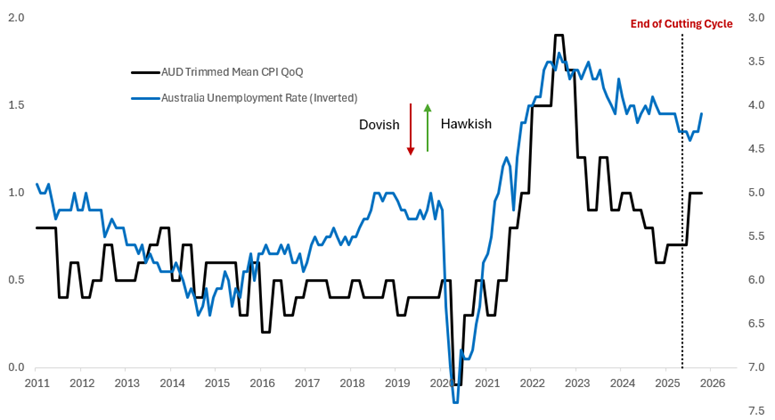

RBA: Increased Conviction in Our Call for a Feb Rate Hike

We highlighted in early January that we thought the case was building for a February rate hike from the RBA, despite markets pricing just 6bps. The market pricing at 15bps has now started to reflect that view following a material beat in employment data. We are increasingly convicted that the RBA will raise rates in February.

Source: Bloomberg, Citadel Securities, January 2026. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

Since the RBA ended their cutting cycle, the policy relevant data has clearly moved in a hawkish direction with inflation rising materially and the labour market tightening both via strong job gains and a lower unemployment rate. The composition of the inflation acceleration is particularly concerning for the RBA as it is largely driven by persistent factors, mostly notably housing, where there appears to be a generalized pick up in property prices that is now feeding into the CPI basket via the new dwellings category (n.b. Q3 data implies nationwide property prices grew at an 8.8% annualized rate).

The RBA’s concerns about upside risks to inflation have been prevalent since November. The Statement on Monetary Policy highlighted the below focus on capacity pressures, despite their then lingering concerns around the labour market (which have since resolved):

Overall, recent data add weight to the possibility – identified as a risk in the August Statement – that there is slightly more capacity pressure in the economy than we previously assessed. Notwithstanding the recent easing in the labour market, a range of indicators – including the low underemployment rate, elevated ratio of vacancies to employed workers, above-average share of firms experiencing difficulty finding workers, high unit labour cost growth, and model estimates of full employment – continue to suggest some remaining tightness in the labour market. A wider set of indicators also continue to point to some capacity and price pressures in the economy more broadly, including elevated capacity utilisation and high output price inflation. While our assessment of spare capacity is uncertain, recent data on inflation, increases in capacity utilisation and the increase in the quits rate all lend support to the possibility that there is slightly more capacity pressure in the labour market and broader economy than we thought in August. RBA November Statement on Monetary Policy – Nov 25

During the December meeting presser, Governor Bullock indicated that rate cuts were off the table and that the discussion centered around the conditions that would merit a rate hike. When asked about the chance of a rate hike in February, Governor Bullock pointed out that the RBA would receive more labour market and inflation data between the December and February meetings (link).

Since that statement, the unemployment rate has declined 20bps to 4.1% and the RBA’s inflation forecast for Q4 2025 of 76bps QoQ looks likely to be too low by around 15bp QoQ, with a consensus for this week’s print centered on 90bp QoQ. It seems difficult to avoid hiking rates given the likely evolution of the data since the December meeting, and the baseline set in the December presser which already implied a hike was a live consideration in February.

The Australian experience is a stark reminder to central banks of the risk of cutting rates to uncertain estimates of neutral, with strong labour markets, elevated fiscal spending and inflation that never sustainably reached target. The RBA appears poised to do the right thing and take back the 2-3 rate cuts that pushed policy too easy for the prevailing macro environment. The Federal Reserve may soon face a similar test.

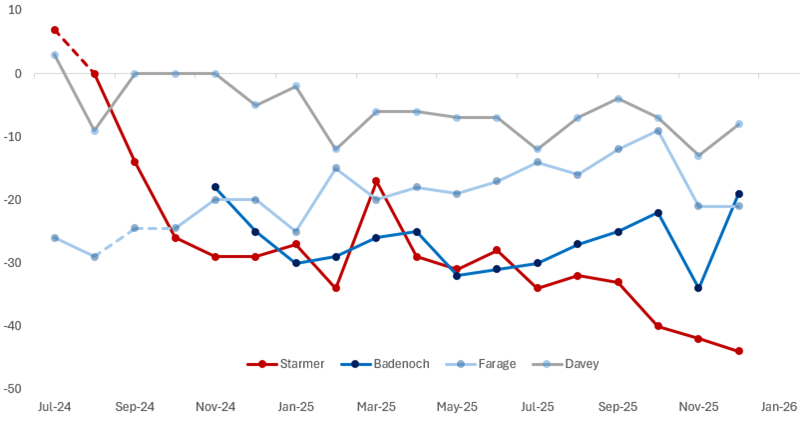

UK Political Risk Hinders an Increasingly Dovish Outlook

Andrew Gwynne this week announced his retirement as an MP, triggering a by-election (mostly likely held alongside or before the local elections in May), which was widely seen as a pathway for Andy Burnham (current Mayor of Manchester) to return to the House of Commons and challenge Keir Starmer for the leadership of the Labour Party (and hence become PM). To trigger a formal leadership election a challenger must meet the nomination threshold of 20% of parliamentary Labour party members and must be a sitting Labour MP.

Labour party rules state that elected mayors need to seek permission from the NEC before standing as an MP and today Starmer and the NEC effectively blocked Burham’s candidacy to replace Gwynne. The effectiveness of this strategy is up for debate as it risks inflaming divisions within the party and the Guardian reported “widespread anger among Labour MPs and union backers” in response to the NEC’s decision to prevent Burnham from running. The decision also raises the stakes with respect to the party’s performance in the by-election and May’s local elections, underlining the fact that political risk remains elevated.

Furthermore polling suggests that Keir Starmer is in a vulnerable position. His approval ratings have been consistently declining and he is the least popular of the current party leaders according to survey data (link). That said – the Gorton and Denton constituency in which Burnham was hoping to compete by no means a safe seat and recent polling gives Reform UK the edge (link), which is now a more important political focal point following the PM’s personal intervention.

Net Favorability Rating of UK Party Leaders

Ipsos Polling Data, July 2024 – Present

Source: Ipsos, Citadel Securities, January 2026. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

The localized market reaction on Thursday implies that a Labour leadership challenge would be negative for UK risk premium as leadership contest could shift Labour’s fiscal direction (link), potentially towards more activist spending or a rethinking of fiscal constraints — depending on who emerges as the challenger. Potential challengers include Angela Rayner, Wes Streeting, Lucy Powell, Ed Milliband, Shabana Mahmood as well as Andy Burnham who still occupies a senior position as Mayor of Manchester.

The risk of a lurch towards less stringent fiscal rules is compounded by the fact that both Rayner and Burham (the two further left potential challengers) have historically been strategically aligned, and an alliance would avoid splitting the left wing of the party. Whether nor not Burnham finds a pathway to challenge Starmer, his curiously timed op-ed in the Guardian this week is important context for the debate around the future direction of the Labour party, as it underlines the risk that a future leader’s approach to fiscal policy could see an increase in both capital and current expenditures.

“These structural weaknesses in our economy were to some degree masked by the higher growth we had in the EU. But the combined effects of austerity and Brexit in the 2010s laid them bare…we are stuck in a rut and in hock to the bond markets because of the resulting volatility and uncertainty… to plot our way out of that and develop a new economy…could mean putting electoral reform centre stage as the means to create a more collaborative politics and consensus on the public investment needed to free the country from the pernicious pincer movement of the simultaneous cost-of-living and housing crises.” – Andy Burham, Guardian Op-Ed (link).

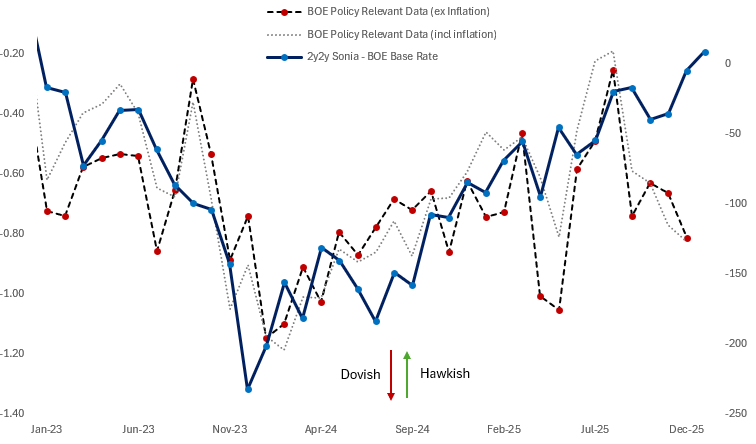

The overhang of UK political risk and the potentially inflationary implications of higher fiscal spending are a material headwind to the market being able to price a materially more dovish policy path for the Bank of England. The well flagged acceleration in CPI (driven by administered prices) has slowed the pace of rate cuts in the last 6 months, however the recent evolution of policy relevant data looks to suggest around five of further rate cuts may be required in the UK.

To highlight this, we construct our own indicator of UK policy relevant data from various official and private sector sources, normalize it and average across the indicators. The indicator contains 16 different metrics that cover the labour market (e.g. hiring, wages, vacancies), inflation (headline, core, services), activity (PMIs) and expectations (inflation expectations, 2y RPI, wage expectations). The metric generally correlates very well the inversion in OIS forwards relative to the base rate, which is a proxy for how much additional easing markets expect. We then feed the policy relevant data index into a simple regression model vs market pricing. The fitted value implies forward rates should be roughly 118bp below the current base rate – which would be equivalent to 4-5 additional rate cuts and putting the terminal rate closer to 2.5%.

The political overhang is a key obstacle to markets pricing a policy rate pathway more closely aligned with economic data. Clarity on the political outlook is likely the catalyst for markets and policy makers refocusing on the evolution of the macro data.

Policy Relevant Macro Data Points to A More Dovish Pathway for the BOE than Priced

1y Z-score of cross-sectional macro data vs 2y2y SONIA – BOE Base Rate

Source: Bloomberg, Citadel Securities, January 2026. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

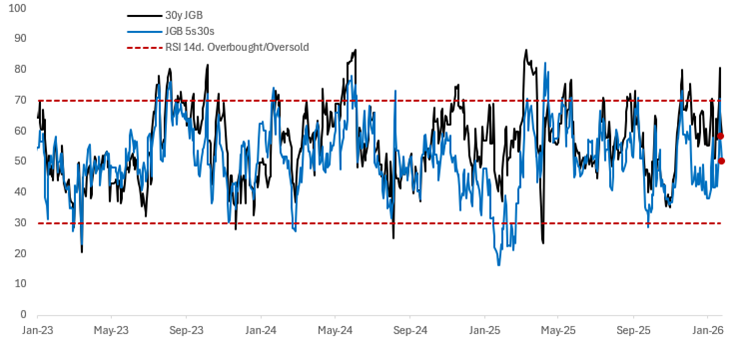

BOJ: April is Live, JGBs No Longer Technically Stretched

As a result of the long end driven rally/flattening in the second half of this week, our momentum indicators have normalized as one would expect. This suggests that some of the market functioning risk premium has come out of the curve and implies the path forward for long end JGBs will be more challenging as valuations are no longer as stretched on a technical basis.The core pillar of our constructive view was that the policy options to lean into the price action were not out of reach and comments from Gov. Ueda in Friday’s post meeting presser did indeed imply a relatively low bar for the temporary long end purchases we thought the BOJ would be inclined to hint towards, as well as for co-ordination with the MoF.

“We will conduct nimble market operations to respond to irregular moves” – Gov Ueda, BOJ Presser, Jan26

“Regarding the pace of long-term interest rate increases — whether it is fast or too fast, and whether it warrants flexible operations — we will make judgments while closely co-ordinating with the government and carefully monitoring the situation,” – Gov Ueda, BOJ Presser, Jan26

On a standalone basis, this kind of intervention on the long end clearly skews negative for trade weighted JPY, although reports of a rate check on USDJPY perhaps imply a two sided intervention strategy (link). In the medium term, both international and domestic asset manager sponsorship are the key to unlocking sustained performance in Japanese duration and JPY FX.

On the policy rate outlook, the BOJ’s forecast upgrade (growth revised +0.2% and +0.3% higher to 0.9% and 1% in 2025 and 2026, inflation revised +0.2% higher in 2025 and 2026 to 3% and 2.2% respectively) is consistent with the faster pace of hikes we had been flagging. Ueda highlighted spring price data and greater confidence in the outlook as relevant for the policy path however we think April is the most likely meeting for the next hike.

Technical Indicators That Caught the Turn in Long End JGBs are Now Neutral

14d RSI on 30y JGB and 5s30s JGB Curve

Source: Bloomberg, Citadel Securities, January 2026. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

Copyright © Citadel Enterprise Americas LLC or one of its affiliates. All rights reserved.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CDGE”) authorized and regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch authorized and regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the Japan Financial Services Agency (“JFSA”); and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”), Financial Industry Regulatory Authority (“FINRA”), and Securities Investor Protection Corporation (“SIPC”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC, FINRA, and SIPC, or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity. Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at www.citadelsecurities.com/GlobalSalesTrading.

Explore

Market Insights - What We Do