-

Who We Are

- What We Do

Series: Global Market IntelligenceThe January Effect

By Scott Rubner

Markets enter the year with momentum, but January brings a distinct set of dynamics. Capital is being deployed, positioning is rebuilding, and volatility is compressed even as the January catalyst calendar ramps up.

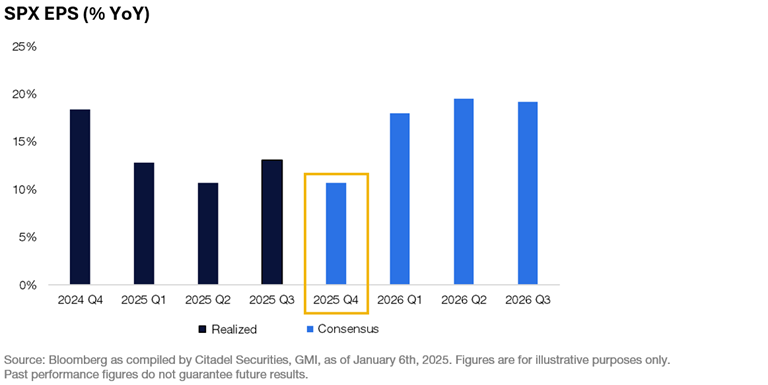

Q4 2025 earnings would mark the tenth consecutive quarter of positive year-over-year earnings growth for the S&P 500, reinforcing a supportive fundamental backdrop as early-year allocations are put to work.

Early-year flows, retail participation, and institutional activity all point to continued near-term support for risk assets. Global equities are at new all-time highs today.

It is time for a thread.

🧵

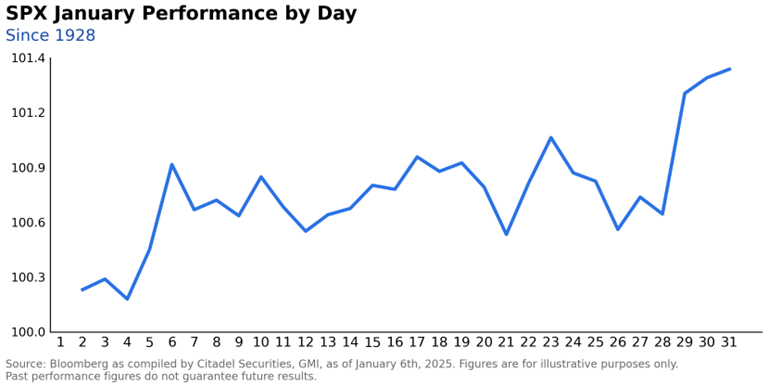

I. #The January Effect

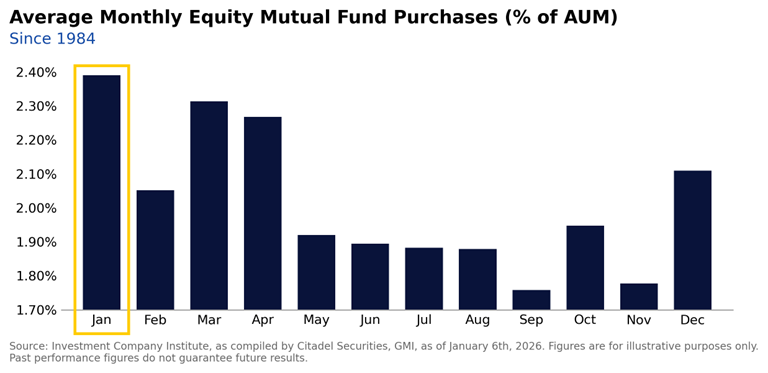

January marks the year’s most active allocation window of the year. As markets reopen after the holiday pause, capital tied to retirement contributions (401k, 529), year-end bonuses, and discretionary PWM mandates moves quickly from cash into passive risk assets. This is particularly true when money market yield levels have declined.

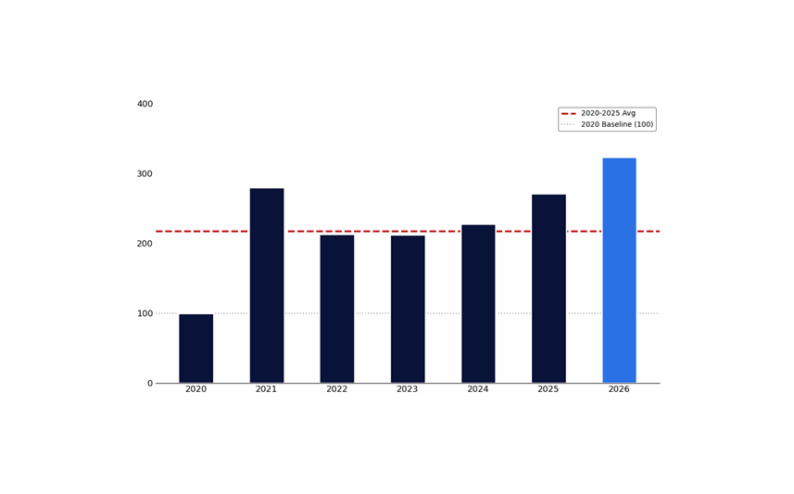

New Year = New Inflows. Historically, January stands out as the strongest month for equity capital deployment, as money market cash levels sit at a record $7.6 Trillion.

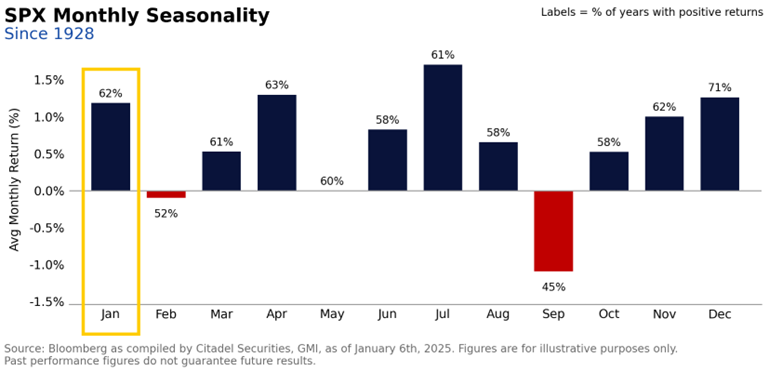

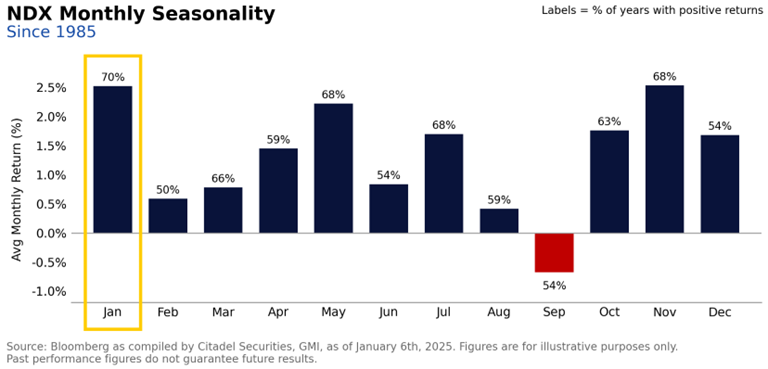

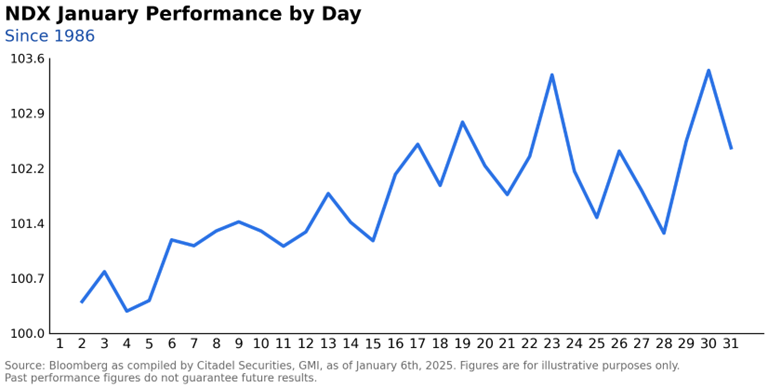

This early-year flow has aligned with favorable January performance across major indices. Since 1985, the Nasdaq 100 has risen in 70% of Januarys, with an average return of 2.5% and average gains of roughly 5.8% when January is positive.

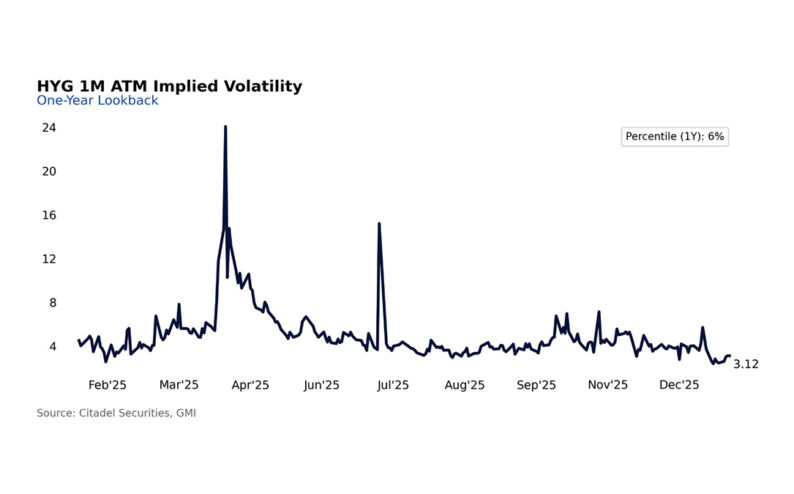

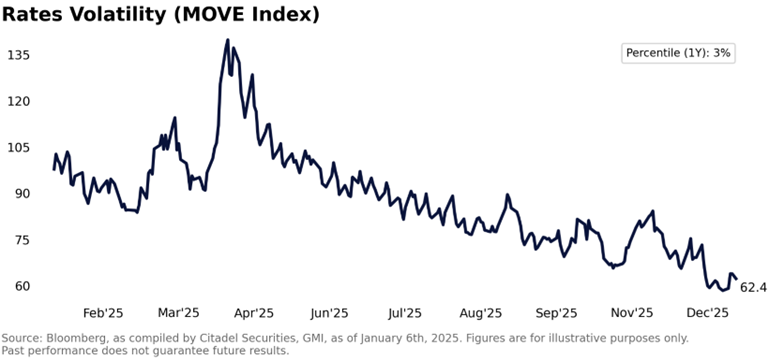

II. Volatility is Low 📌

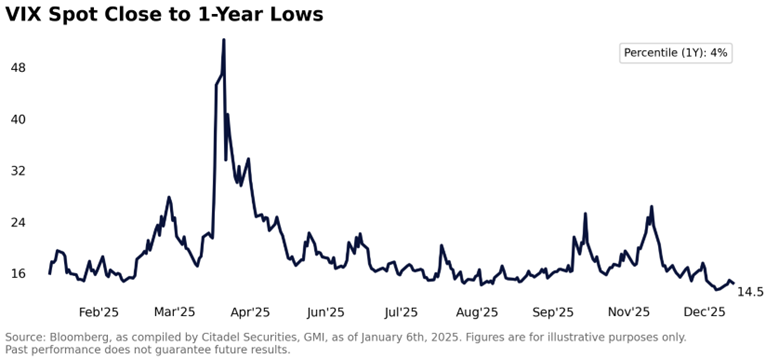

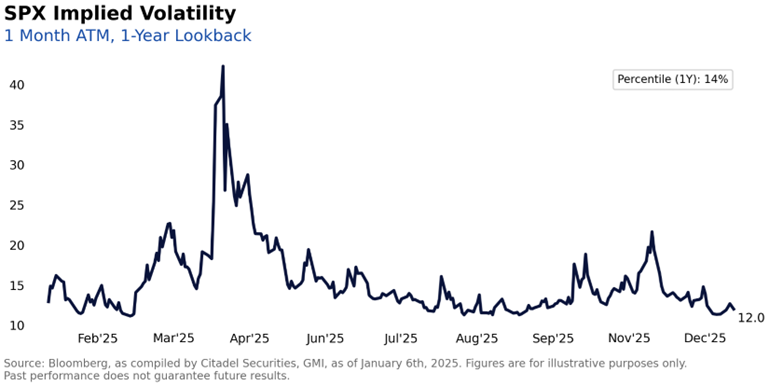

The VIX dipped below 14 heading into Christmas and now sits around 14.5, even as markets kick off the year with a dense stretch of conferences, macro data, and earnings. SPX 1-month at-the-money implied volatility hit a one-year low on December 26th and remains near ~12 vol, in the 14th percentile of its one-year range.

At the same time, the January macro calendar is very active:

- Consumer Electronics Show (CES) Conference – January 6-9

- Non-Farm Payrolls – January 9

- ICR Consumer Conference – January 12-14

- JPM Healthcare Conference – January 12-15

- December CPI, Earnings Kickoff – January 13

- November PPI, Retail Sales – January 14

- FOMC Rate Decision, TSLA earnings – January 28

- META, MSFT, AAPL earnings – estimated January 29-30

- December PPI – January 30

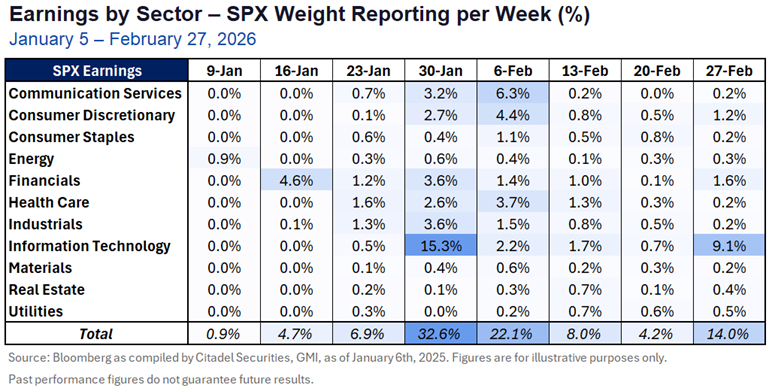

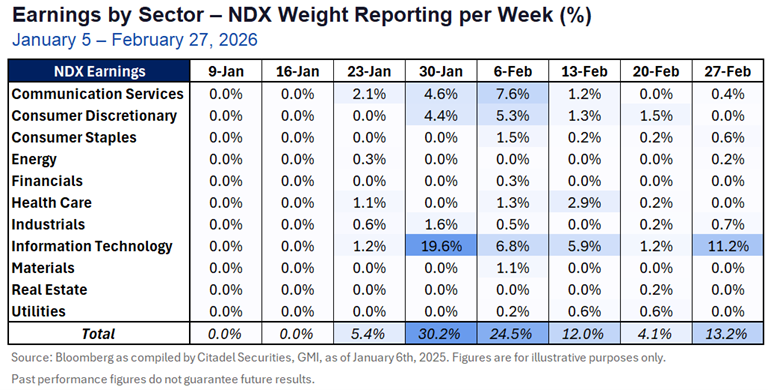

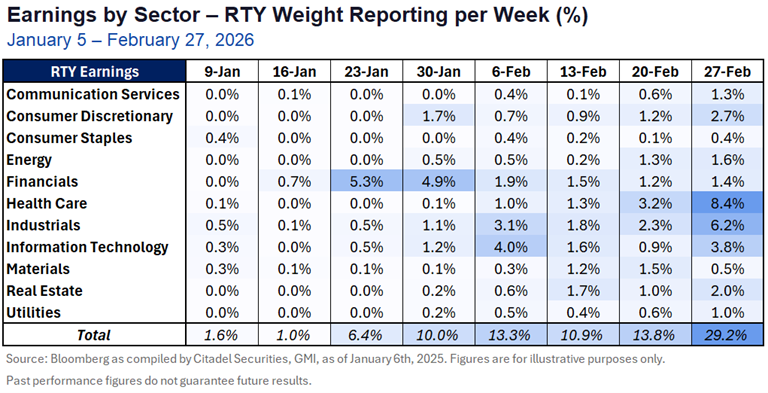

- 45% of SPX, 36% of NDX, and 19% of RTY by weight reporting by the end of the month

- New FOMC Chair announcement expected by Feb 1

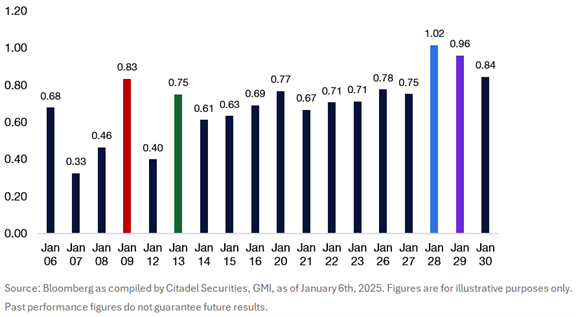

SPX Implied Daily Move (%)

Next Tuesday kicks off Q4 earnings season with financials and a hopeful outlook for M&A:

III. Profits – Earnings Remain Supportive

Earnings momentum is broadening beyond a narrow group of mega-cap leaders. What began as an AI-led profit cycle is increasingly diffusing across sectors, reinforcing market breadth and supporting a more durable earnings expansion for the entire equity market.

Importantly, profit growth is becoming less concentrated. While mega-cap technology continues to deliver strong results, earnings momentum is increasingly visible across industrials, healthcare, energy, and financials, reducing reliance on a single cohort to drive index-level growth.

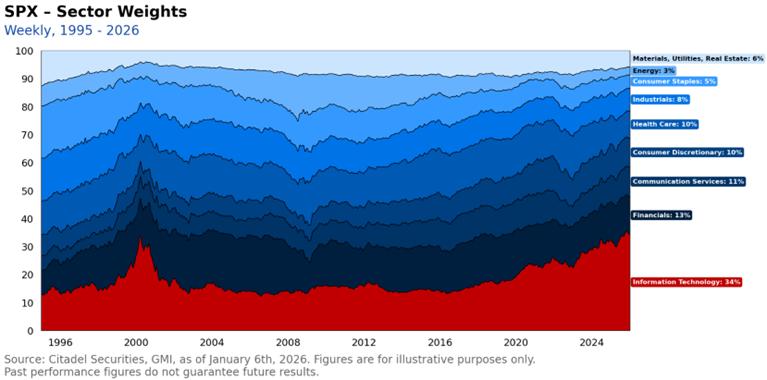

That said, index concentration remains elevated – allocating one dollar of your new 401k capital to SPX directs roughly 39 cents into the top ten mega-cap constituents. This leaves ample room for earnings-driven catch-up elsewhere.

The US energy sector remains topical, with the sector accounting for just 2.9% of the S&P 500 – far below its 2008 peak of ~16.1% and only marginally above its 2020 trough near ~2%. The current energy weight sits well below the long-term average of roughly 7.5% since 1995. Investors will move into sector based ETFs and single names to gain exposure.

IV. Retail is Strong 🔑

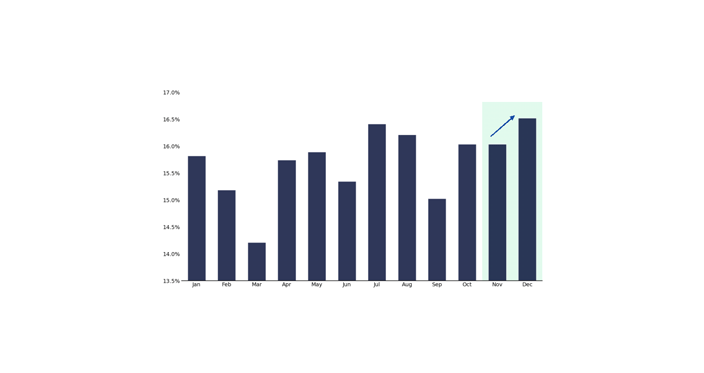

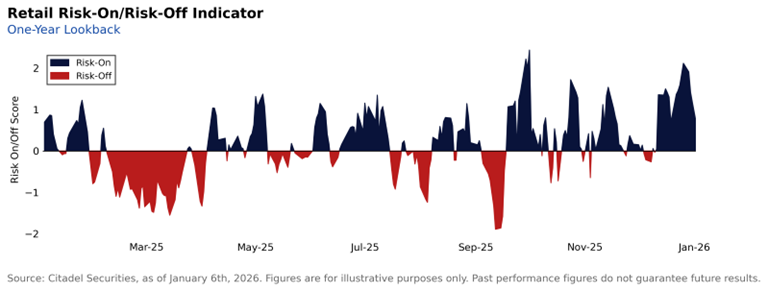

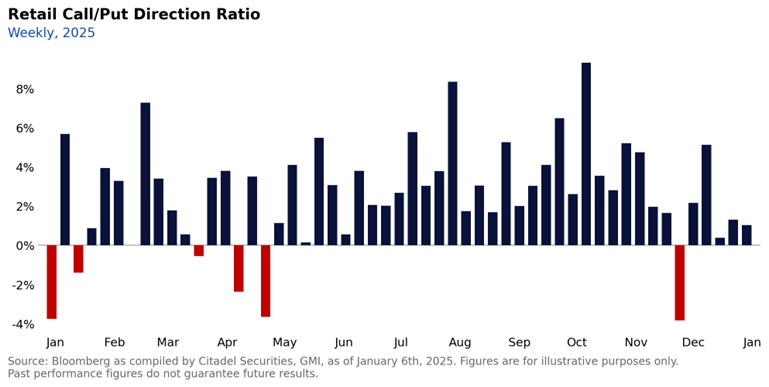

As highlighted in yesterday’s Retail Conviction at Scale: Top Themes into 2026 note, we estimate that retail traders now account for 60% of all OCC customer volume. At this level of participation, retail is no longer marginal to market outcomes – they are a driver.

The defining feature of retail activity in 2025 was persistent, directional bullishness, expressed through options with notable scale and consistency. After earning more than $20 billion in options on our platform over the course of the year, retail investors enter January armed with capital to deploy.

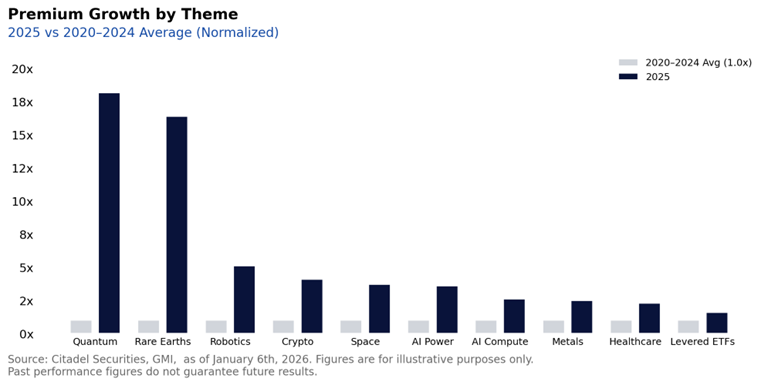

This demand remains a steady source of upside pressure, amplifying early-year flows and contributing to January momentum. We expect this dynamic to reassert itself early in the year, particularly in retail-favored themes such as Quantum Computing, Robotics & Automation, and Space, which saw premium growth far above historical norms in 2025.

Retail has been buyers of calls in 35 out of the past 36 weeks, where SPX gained +24.1% over that period.

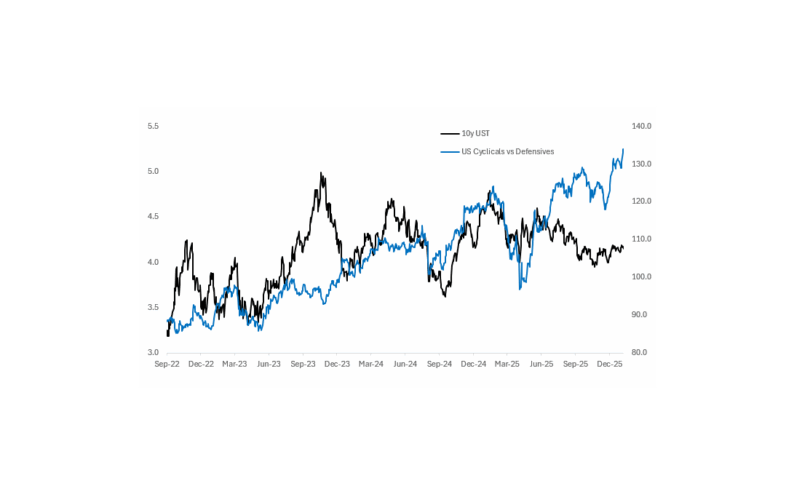

V. Citadel Securities Client Flows are Bullish – and Broadening 🌏

There is a pro-growth, pro-cyclical, pro-expansionary, vibe to the market and our client activity to start 2026.

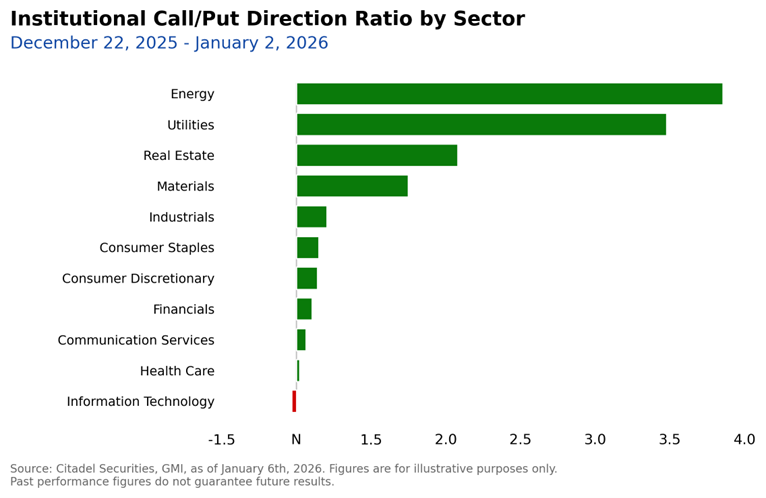

Beyond retail, Citadel Securities’ institutional clients are leaning risk-on. Last week, institutional options flow was skewed 5% better to buy, with demand concentrated in Energy, Utilities, Real Estate, and Materials.

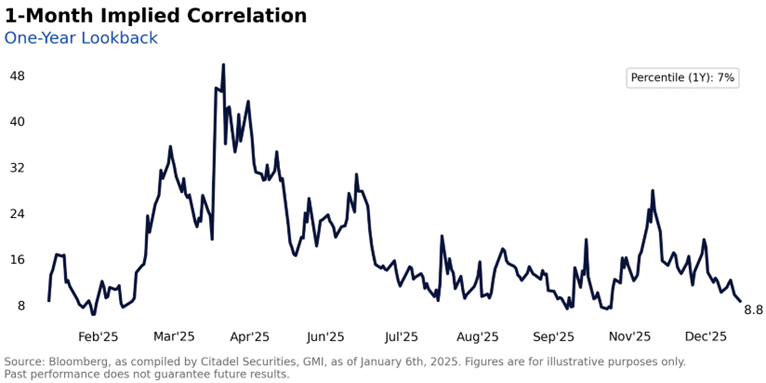

At the same time, cross-asset correlations are compressing. One-month implied correlations are approaching one-year lows, a signal of healthier market structure and greater scope for idiosyncratic alpha to re-emerge.

2026 is shaping up to be a stock pickers market and active management to return.

This activity reflects a deliberate shift toward areas of the market that have lagged prior leadership. With index concentration still elevated, clients are increasingly directing new allocations toward sectors outside the most crowded trades.

VI. The Playbook – GMI BOTTOM LINE ⬇️

👉 2026 GMI Framework: 2 R’s and 3 P’s

- Retail: conviction buying

- Rotation: market breadth expanding

- Positioning: re-leveraging underway

- Profits: acceleration phase

- Policy: increasingly accommodative

January begins with a constructive macroeconomic setup driven by early-year capital deployment, supportive seasonality, and rebuilding positioning. Flows are being put to work across both retail and institutional channels, while participation continues to broaden beyond the most crowded parts of the market.

At the same time, volatility remains compressed relative to the January catalyst calendar, creating an attractive opportunity to participate in early-year strength through options rather than committing balance sheet at current levels. Low correlations also provide an opportunity to reintroduce index- and sector-level hedges while volatility is cheap.

Looking ahead, we expect some healthy digestion in February as early-year allocations normalize and volatility has scope to reprice. Any pullback or volatility reset would represent an opportunity to re-engage risk at more attractive levels.

Copyright © Citadel Enterprise Americas LLC or one of its affiliates. All rights reserved.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CDGE”) authorized and regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch authorized and regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the Japan Financial Services Agency (“JFSA”); and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”), Financial Industry Regulatory Authority (“FINRA”), and Securities Investor Protection Corporation (“SIPC”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC, FINRA, and SIPC, or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity. Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at www.citadelsecurities.com/GlobalSalesTrading.

Explore

Market Insights - What We Do