-

Who We Are

- What We Do

Series: Global Macro StrategyVerif-AI-ng the Macro Consensus

By Frank Flight

Citadel Securities conducted an institutional client survey on how AI will impact productivity, labor markets, inflation, monetary policy and bond yields. We use this to map out a macro consensus on AI and then try to present some balanced and thoughtful challenges to that consensus. We highlight that the consensus may be too negative on the labor market impact, rightfully split on the implications for monetary policy and shifting towards AI as a bearish rather than bullish duration impulse. Finally, with nearly 90% of respondents expecting AI to drive a positive productivity shock, we note that markets tend to overhype the immediate benefits of technological change and under-index to the long term total factor productivity compounding that can occur over decades as a result of generational technological shifts.

The AI super-theme has dominated the investment thesis for US tech for the last 2 years. The next phase of AI hinges on the adoption and integration of AI into the broader economy. If markets are internally consistent with one another, then one could argue the fact that hyper-scaler valuations are built on an expectation of AI capex delivering a significant ROI, then macro markets should already embed some AI-premium by discounting expected productivity gains, potentially explaining why markets are relaxed on US inflation risks and focused on labor markets as a key downside risk.

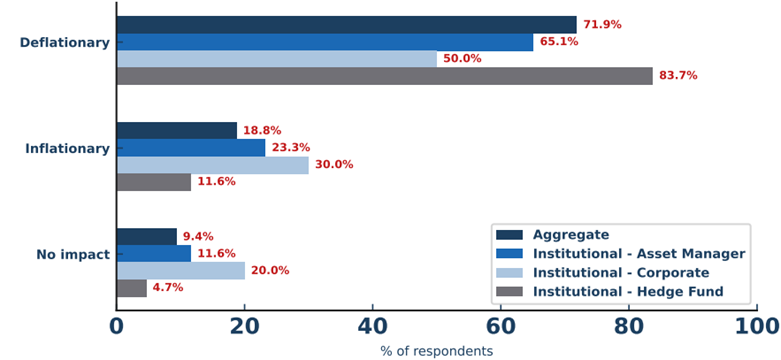

SURVEY RESULT: In the medium term (2-5yrs) AI will be:

Source: Citadel Securities Client Survey, Nov-25

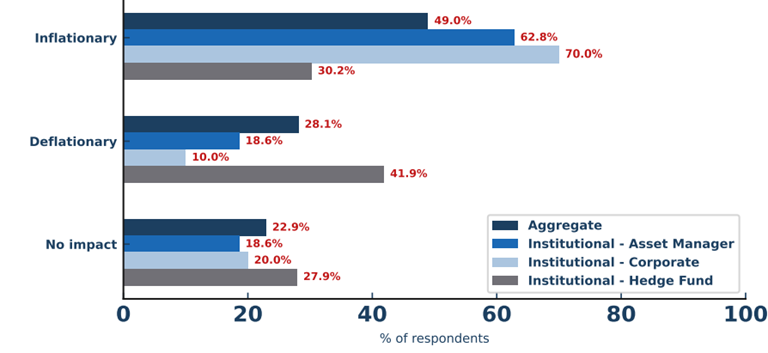

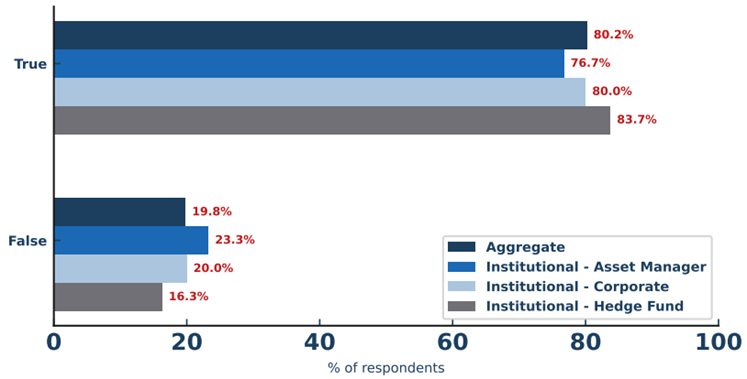

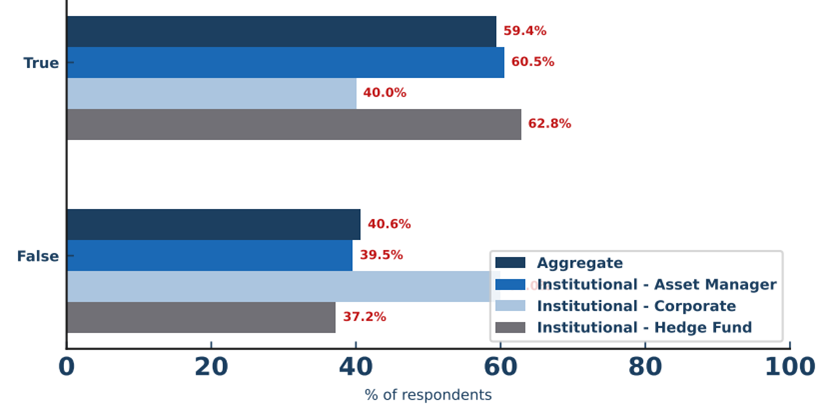

The results of our client survey are broadly consistent with this idea, with 71.9% of respondents believing that AI will be deflationary in the medium term, and 80.2% believing that it will result in an increase in unemployment. However, the short run impact of AI on inflation is much less clear, given the power intensity of AI compute and the implications for electricity pricing. Furthermore, the labor intensity of the data center build outs is a key source of uncertainty given the high share of foreign-born labor in the US construction industry in the context of recent immigration restrictions, which may amplify cyclical wage dynamics in the construction sector. The corporate community appears more convinced of the short run inflationary impact of AI at 70%, relative to the aggregated results in which 49% see AI as inflationary, 28.1% see it as disinflationary and 22.9% see no impact.

In the short run (1-2yrs) AI will be:

Source: Citadel Securities Client Survey, Nov-25

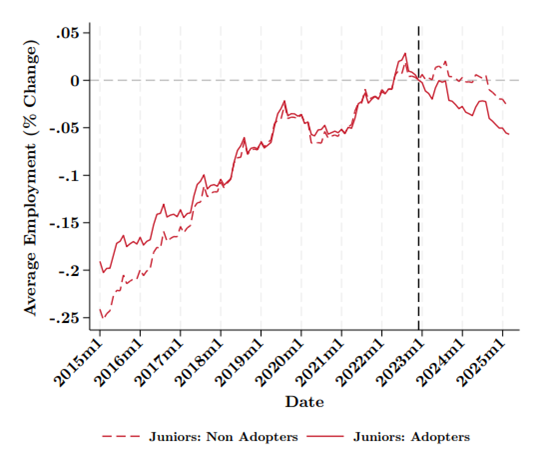

Historically speaking, episodes of widespread technological change have created more jobs than they have destroyed, and the disinflationary impacts have generally been hard to isolate. That said there are good conceptual arguments as to why an AI singularity moment may prove to be non linear for global labor markets and why “this time is different”. However there are conflicting studies as to how AI has impacted job markets and productivity thus far. For example, Maasoum and Lichtinger (2025) used a novel methodology taking job openings + resume data covering 62 million workers across 285,000 firms to capture the impact of AI on the labor market. They track companies that hired “generative-AI integrators” and measure how employment changed at these firms vs firms that did not hire AI integrators and found that the firms integrating AI saw a 7.7% decline in hiring for junior roles relative to non-adopter firms but found no discernible difference for hiring at senior level for adopters vs non adopters.

Average Junior Employment Change: AI Adopters vs Non Adopters

Source: Maasoum and Lichtinger (2025)

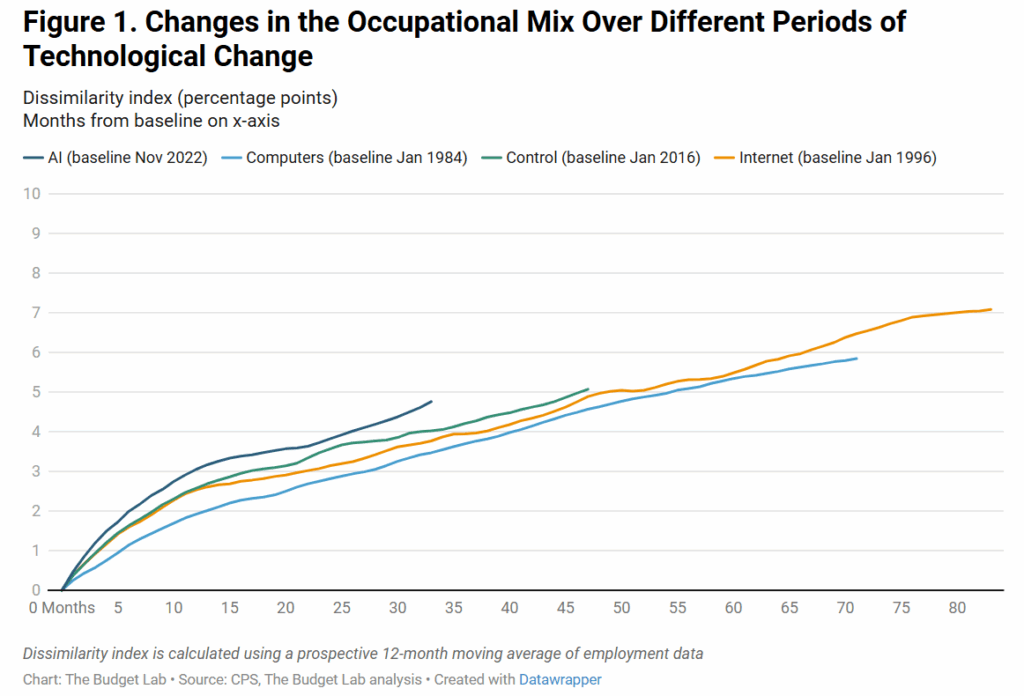

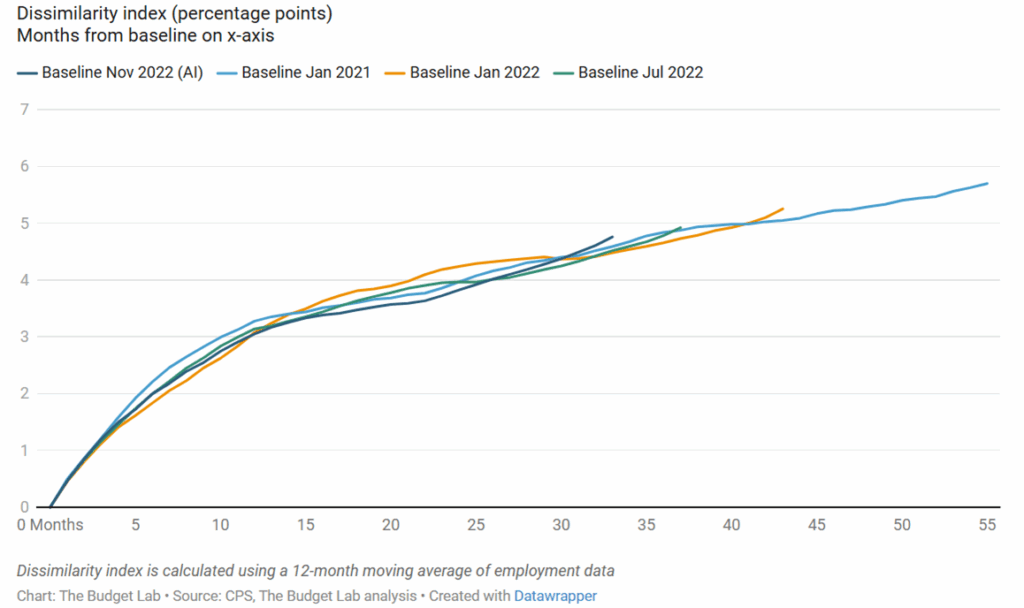

These results go some way to explain the puzzle of the low hire, low fire dynamics in the US labor market. It also helps explain the gap between the seemingly weak spot of labor market data vs other US macro data, and is consistent with the official data which shows the U-rate has risen disproportionately for young workers vs the general workforce. However – recent work from the Yale budget lab (Gimbel et al. 2025) pushback on this idea too, by creating dissimilarity indexes (that measure how the occupational mix of the labor force is changing month to month to get a sense of if AI (or anything else) is disrupting existing labor market patterns), in order to assess if there are obvious changes relative to pre-pandemic baselines since the advent of Chat-GPT. The changes in occupational mix appear to be only ever-so-slightly quicker than in previous periods of technological change (internet and computers) – which notably did not result in labor market disruptions. Furthermore the authors note that “taking a closer look at recent years, the data suggests that this recent trend is not necessarily attributable to AI (Figure 2). Shifts in the occupational mix were well on their way during 2021, before the release of generative AI, and more recent changes do not seem any more pronounced, even as the use of AI continues to grow in popularity” (Gimbel et al. 2025).

Aggregate Level Data Shows Little AI Impact Thus Far

Source: Yale Budget Lab

Indeed in a systematic literature review Hotte et al (2023) analyzed “127 studies published in academic peer-reviewed journals between 1988 and 2021 that provide evidence on technological change in industrialized economies in the post-1980s…[they] find the number of studies supporting the labor replacement effect is more than offset by the number of studies supporting the labor-creating reinstatement and real income effect.” The theoretical reason for the offset to a productivity driven decline in labor intensity is two fold. Firstly a productivity shock is generally associated with an increase in r*, which provides a material offset to declining labor intensity for aggregate employment levels because economic output should expand in response to an easing of the policy stance relative to an unchanged policy rate. Furthermore higher neutral rates/easier policy impulses in the short term likely drive an increase in risk appetite/animal spirits which in turn drive wealth effects via equity valuations, which in turn drive financial conditions looser and ultimately better growth outcomes. However in the medium term these episodes are typically associated with an increase in leverage and tend to end badly, as we saw in the dot com bubble, where ultimately technology did prove transformative, but not on a timeline that was able to justify dotcom valuations. Acemoglu and Restrepo (2019) argue that new technologies create complementary labor demand in adjacent sectors (eg tech installation, maintenance and supervision), Vivarelli (2014) highlights the redeployment of resources following productivity upturns toward non-automated activities and Baldwin et al. (2021) note that if demand is sufficiently elastic then productivity can lower consumer prices and result output expanding along the aggregate demand curve which can paradoxically increase labor demand. Additionally increases in the marginal product of labor should drive higher real wages all else equal, which tends to feed into stronger consumption – a dynamic highlighted by Bessen (2020). These dynamics offer some theoretical offset to the relatively dismal consensus with respect to the impact of AI on the Labor market, at least from a medium term perspective.

Will AI cause unemployment to rise?

Source: Citadel Securities Client Survey, Nov-25

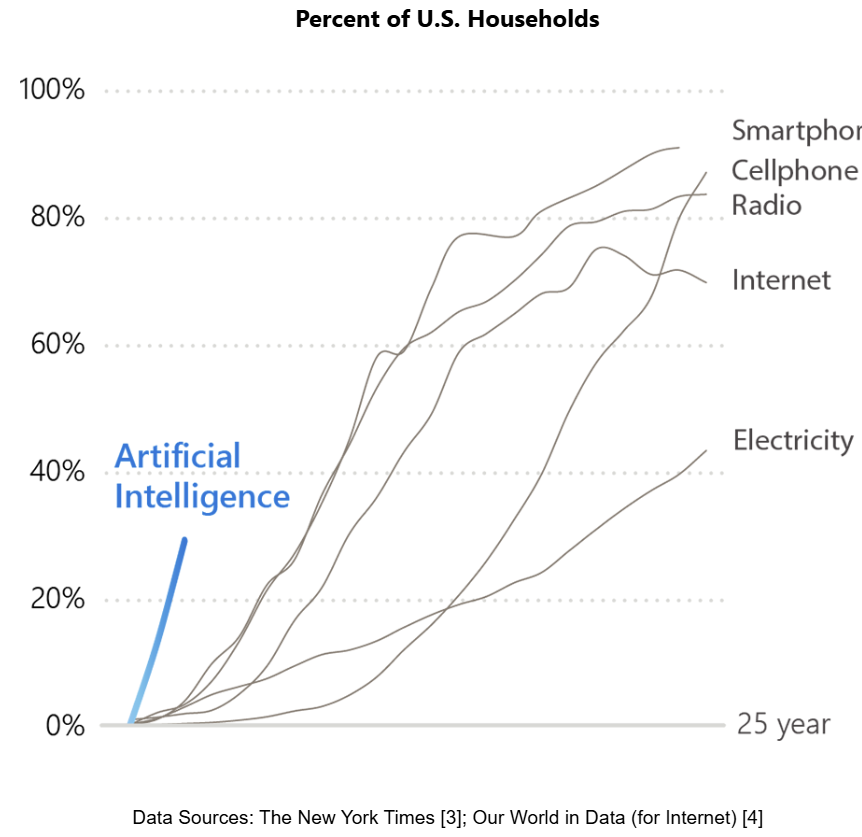

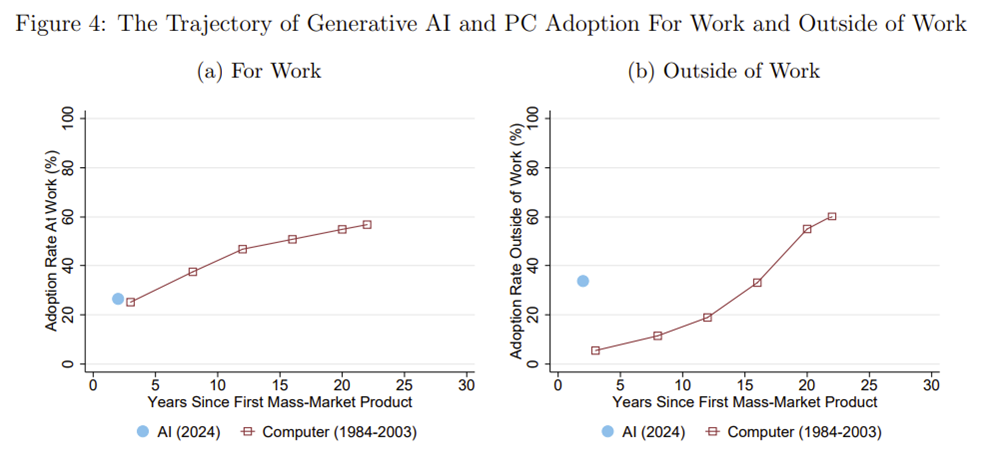

The extent to which AI will have a disruptive impact on the labor market is likely to be somewhat determined by the speed of adoption, given the historical precedent of labor markets adapting to technological change through time. The evidence thus far on AI adoption is that it is running ahead of recent modern technological innovations. A Microsoft report on AI adoption implies AI is “the fastest-spreading technology in human history. In less than three years, more than 1.2 billion people have used AI tools, a rate of adoption faster than the internet, the personal computer, or even the smartphone.” Furthermore Bick et al (2024) “report the combined results of two surveys fielded in August and November 2024, which collectively included more than 10,000 respondents” and demonstrate that 39 percent of respondents report using genAI either for work or outside of work. However the novel contribution of this study is to differentiate between professional and personal use. The study implies “the adoption of genAI has so far been at least as fast as adoption of computers and the internet. In 1984, 25 percent of workers reported using computers for their job, compared with 27 percent of workers who report using genAI for their job in 2024…In contrast, genAI has been adopted at a faster rate than computers outside of work.” These comparisons index to similar t=0 points and so provide a somewhat more balanced perspective on AI adoption in a professional capacity seeing something more similar to the adoption of computers, which is important when considering the macroeconomic impact of AI on labor markets in particular.

AI Adoption: Microsoft AI Economy Institute

Source: Microsoft AI Economy Institute

Trajectory of Generative AI vs PC Adoption For Work and Outside of work

Source: The Rapid Adoption of Generative AI. Alexander Bick, Adam Blandin, and David J. Deming

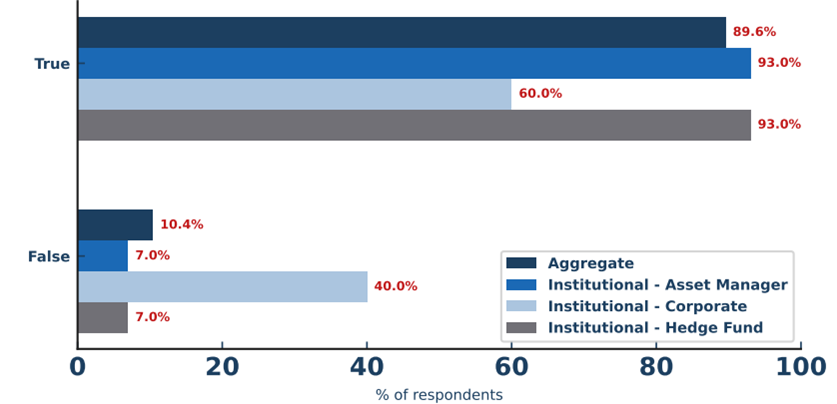

The primary channel via which AI should impact macroeconomic variables is of course productivity. Generally speaking our survey results suggest that institutional respondents expect AI to deliver a meaningful increase in productivity, but the composition of respondents is interesting. 89.6% of respondents expect AI to deliver a positive productivity shock however among corporate respondents the expectation of a positive productivity shock was meaningfully lower at just 60%. We would note that corporate client responses represented only around 10% of total respondents, so we would not over index to these results due to small sample size, but the contrast vs hedge fund and asset manager respondents is interesting.

Will AI deliver a positive productivity shock?

Source: Citadel Securities Client Survey, Nov-25,

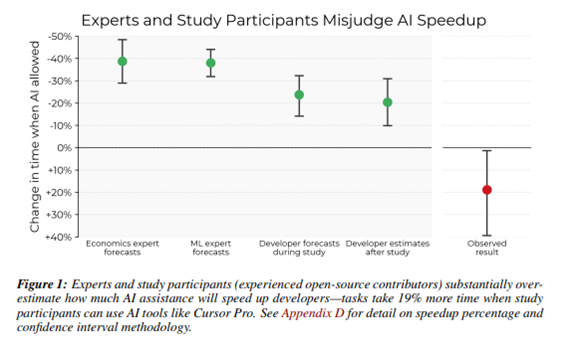

An interesting question is the interaction of AI driven shifts in working patterns with aging populations. With the inevitable rise in baby-boomer generation retirements, it may well be that AI provides an offset to an otherwise very growth negative demographic trend. In fact one could argue that it is only because of sustained technological leaps throughout history that the global economy has been able to sustain a roughly 2% long run growth trajectory, despite increasingly challenging demographics and diminishing returns to long run capital accumulation. However the confidence expressed by respondents in our survey with respect to the likelihood of a positive productivity shock is not consistent with the findings from a Brookings survey of 1,000 American adults which found that only 19% of all respondents report that AI increased their productivity in their daily tasks, and only 4% say it increased their productivity significantly. Naturally, there is a horizon mismatch to address here which is a function of the fact the Brookings survey is measuring spot productivity impacts which could of course scale as the technology evolves but it is an important reminder of the sequencing and timeline to expect an AI dividend, particularly when thinking about the impact at a macroeconomic level. To put some further quantitative framing around this point, Becker et al (2025) conduct randomized controlled trial to understand how AI tools affect the productivity of software developers. 16 developers with moderate AI experience were asked to complete 246 tasks and each task was randomly assigned to allow or disallow usage of early 2025 AI tools. A priori the participants forecast that AI would reduce completion time by 24% however the study found that AI actually increased completion time by 19%, implying a negative productivity impact. Naturally there are many counterarguments to this finding, most notably that AI tools are improving at a rapid pace and one cannot assume a static impact on productivity. There are many published studies that have found worker productivity uplifts as a result of AI: Brynjolfsson et al (2023) note 14% increases in call centre agent issue resolution, Cui et al (2025) see a 26% increase in completed tasks in coding experiments, Dell’Acqua et al (2023) note low double digit productivity gains for knowledge workers and Noy and Zhang (2023) note 40% faster writing task completion, but the academic literature also notes that these time saving benefits only translate into economic benefit if time savings are monetized in the form of higher output, higher quality or reduced labor input rather than that time simply just being reallocated to non-economic tasks. Its highly likely that time savings over the medium term are monetized, but in the short term its worth noting that the bar is relatively high to exceed a productivity gain which according to our survey is priced by 90% of respondents. The extent of that productivity increment is therefore pivotal to the broader AI theme. Generally speaking history suggests that markets tend to overhype the immediate benefits of technological change and under-index to the long term total factor productivity compounding that can occur over decades as a result of generational technological shifts.

One Randomized Control Trial Implied Developer Productivity Declined Using AI

Source: Joel Becker, Nate Rush, Beth Barnes, David Rein, “Measuring the Impact of Early-2025 AI on Experienced Open-Source Developer Productivity”, METR, 2025

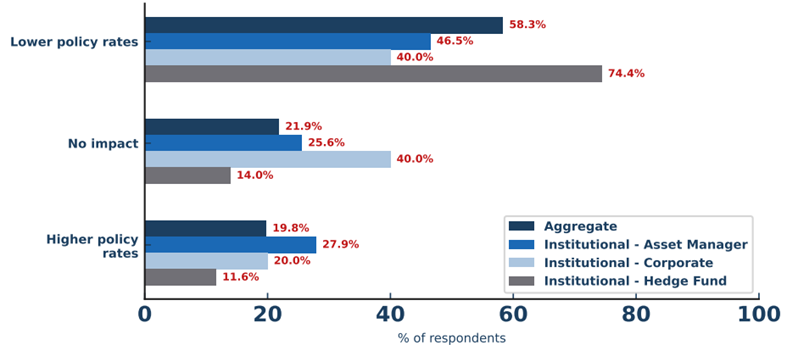

The implications of AI for monetary policy are interesting in that a positive productivity shock would tend to have dovish implications for monetary policy, as it would generally be associated with lower inflation and higher unemployment. However a positive productivity shock generally causes neutral rates to rise and drives risk appetite expansion, which tends to ease financial conditions via risky asset performance, making the implications for monetary policy less clear. One can think of AI as raising the speed limit for the economy, in terms of the growth achievable without creating inflation, however its difficult to assess the neutral rate and interaction with prevailing economic impulses and hence the risks of miscalibrating policy are high in the context of the AI boom, especially given the countervailing forces of tariff policy, immigration restrictions and the debasement theme. Furthermore the impact of AI on productivity needs to realise very quickly relative to history in order to offset some of the clearly inflationary forces associated with data centre build out, energy intensity of compute and potential commodity price appreciation in order to neutralize monetary policy implications which skew more hawkish in the short term. Regarding the medium term implications for monetary policy – the Greenspan Fed during the 90s is a relevant analog here as the Maestro responded to the technological productivity gains of the 90s by allowing the economy to run hot via easier policy/lower policy rates than would have been implied by policy rule models, as growth averaged 3.5-4% in the second half of the decade and unemployment fell below 5% (and estimates of NAIRU) without eliciting pre-emptive rate hikes. Despite his caution against “irrational exuberance” Greenspan de-emphasized the policy relevance of significant asset price inflation until it showed up in measured consumer price inflation which, subsequently resulted in sharp policy tightening and the end of the dot-com bubble. Interestingly hedge fund respondents to our survey see the impact of AI on monetary policy as clearly skewed dovish as 74.4% expect lower policy rates relative to just 58.3% of aggregate respondents, potentially reflecting an expectation of a productivity driven easing of the monetary stance similar to the 90s.

When thinking about monetary policy, AI will likely result in:

Source: Citadel Securities Client Survey, Nov-25

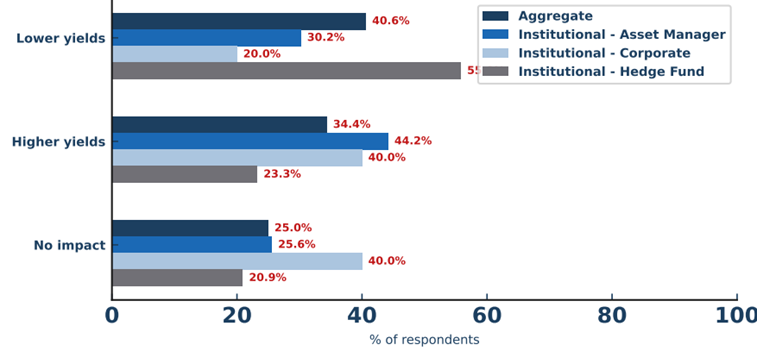

The extent to which AI will drive bond yields higher or lower is a function of the policy rate outlook, term premium, and breakevens. If one assumes that AI generates a positive productivity shock then its possible that disinflation drives fed rate cuts and that ongoing disinflation is reflected in the inflation forwards in the form of lower breakevens. Furthermore a positive productivity shock can reduce term premium because it causes trend growth to improve, which in turn improves sovereign debt sustainability. In a MIT working paper Andrews and Farboodi (2025) studied US bond market reaction around 15 major AI model releases from Jan 2023 to Dec 2024 and found that both nominal and real rates decline on average by >10bps and remain depressed through 15 trading days following the model release. This lends support to the disinflationary/dovish dynamic being the key driver of the initial phase of bond markets response to AI. However, AI has transitioned from an earnings funded theme to an increasingly debt funded theme, with McKinsey estimating that data centre investment alone will reach c$7tn by 2030 and Apollo estimating that AI related issuance doubled in its share of US IG credit supply from 7% in 2024 to 14% in 2025. Furthermore AI capex estimates continue to be revised higher with the consensus estimate for hyperscaler capex now $527bn for 2026 alone. The sheer scale of investment expenditure may flip the bond market’s response to AI towards higher yields through the crowding out channel as corporate supply increasingly weighs on global duration at a time when existing sovereign supply continues at historically elevated levels. Furthermore economic theory supports this dynamic through two additional channels, firstly a textbook DSGE (Dynamic Stochastic General Equilibrium) model of an economy would imply that Savings = Investment, and therefore as investment rises via the AI theme then savings must rise to fund such an investment. In the absence of a global savings glut, that generally means that real rates must rise in order incentivize the savings to fund such investment. Secondly – given the ROE on AI investment is assumed to be profitable and as such macro markets should increasingly price a more positive growth forward as the benefits of AI eventually come online and a higher growth potential is unlocked, this raises the equilibrium or neutral rate (r*) which should drive yields higher (particularly fwd such as 5y5y). The results of our survey are quite evenly split in terms of the impact of AI on bond yields, perhaps reflecting the shifting dynamic from the bullish early stage impact of AI on yields to the new reality of a tremendous amount of relatively inelastic hyperscaler IG credit supply and potentially higher neutral rates.

When thinking about 10y UST yields, AI will likely result in:

Source: Citadel Securities Client Survey, Nov-25

As discussed a major productivity boom is often cited as the key hope for long term fiscal sustainability, indeed a 1% increase in productivity can be the difference between a non-linear fiscal deterioration and a declining debt to GDP ratio. However our survey results imply a relatively high level of conviction that if AI should cause increases in unemployment then governments will be forced to provide additional fiscal stimulus to displaced workers above and beyond existing unemployment programs, likely dampening the improvement in fiscal sustainability as a result.

Taken together we note that the consensus may be too negative on the labor market impact, rightfully split on the implications for monetary policy and shifting towards AI as a bearish rather than bullish duration impulse. Finally, with nearly 90% of respondents expecting AI to drive a positive productivity shock, we note that markets tend to overhype the immediate benefits of technological change and under-index to the long term total factor productivity compounding that can occur over decades as a result of generational technological shifts.

Will govts add further fiscal support if AI displaces workers?

Source: Citadel Securities Client Survey, Nov-25

Bibliography

Hosseini Maasoum, S.M. & Lichtinger, G., 2025. “Generative AI as seniority-biased technological change: Evidence from U.S. résumé and job posting data”. SSRN Scholarly Paper 5425555, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5425555

Gimbel, M., Kinder, M., Kendall, J. & Lee, M., 2025. “Evaluating the impact of AI on the labor market: Current state of affairs” The Budget Lab at Yale, 1 October, https://budgetlab.yale.edu/research/evaluating-impact-ai-labor-market-current-state-affairs

Hötte, K., Somers, M., & Theodorakopoulos, A. (2023). Technology and jobs: A systematic literature review. Technological Forecasting and Social Change, 194, 122750., https://www.sciencedirect.com/science/article/pii/S0040162523004353

Acemoglu, D., & Restrepo, P. (2019). Automation and New Tasks: How Technology Displaces and Reinstates Labor. Journal of Economic Perspectives, 33(2), 3–30, https://www.aeaweb.org/articles?id=10.1257/jep.33.2.3

Baldwin, R., Forslid, R., & Ito, T. (2021). Digitalization and the Productive Transformation of Growth. In R. Baldwin & B. di Mauro (Eds.), Mitigating the COVID Economic Crisis: Act Fast and Do Whatever It Takes (pp. 247–260). CEPR Press, https://cepr.org/system/files/publication-files/60118-mitigating_the_covid_economic_crisis_act_fast_and_do_whatever_it_takes.pdf

Bessen, J. (2020). AI and Jobs: The Role of Demand. NBER Working Paper No. 24235, https://www.nber.org/system/files/working_papers/w24235/w24235.pdf

Vivarelli, M. (2014). Innovation, Employment and Skills in Advanced and Developing Countries: A Survey of the Literature. Journal of Economic Issues, 48(1), 123–154, https://www.jstor.org/stable/43905774

Alikhani, M., Harris, B. and Patnaik, S. (2025) How are Americans using AI? Evidence from a nationwide survey, Brookings, https://www.brookings.edu/articles/how-are-americans-using-ai-evidence-from-a-nationwide-survey/

Bick, Alexander, Adam Blandin, and David J. Deming. “The Rapid Adoption of Generative AI.” NBER Working Paper Series, September 2024, https://www.nber.org/system/files/working_papers/w32966/w32966.pdf

Microsoft AI Economy Institute, “AI Diffusion Report: Where AI is most used, developed and built”, October 2025, https://www.microsoft.com/en-us/research/wp-content/uploads/2025/10/Microsoft-AI-Diffusion-Report.pdf

Joel Becker, Nate Rush, Beth Barnes, David Rein, “Measuring the Impact of Early-2025 AI on Experienced Open-Source Developer Productivity”, METR, 2025, https://metr.org/blog/2025-07-10-early-2025-ai-experienced-os-dev-study/

Erik Brynjolfsson, Danielle Li, and Lindsey R. Raymond, “Generative AI at Work,” NBER Working Paper 31161 (2023), https://doi.org/10.3386/w31161

Cui, Zheyuan and Demirer, Mert and Jaffe, Sonia and Musolff, Leon and Peng, Sida and Salz, Tobias, “The Effects of Generative AI on High-Skilled Work: Evidence from Three Field Experiments with Software Developers” (August 20, 2025). https://ssrn.com/abstract=4945566

Dell’Acqua, Fabrizio and McFowland III, Edward and Mollick, Ethan R. and Lifshitz-Assaf, Hila and Kellogg, Katherine and Rajendran, Saran and Krayer, Lisa and Candelon, François and Lakhani, Karim R., “Navigating the Jagged Technological Frontier: Field Experimental Evidence of the Effects of AI on Knowledge Worker Productivity and Quality” (September 15, 2023). Harvard Business School Technology & Operations Mgt. Unit Working Paper No. 24-013, The Wharton School Research Paper, https://ssrn.com/abstract=4573321

Noy, Shakked and Zhang, Whitney, “Experimental Evidence on the Productivity Effects of Generative Artificial Intelligence” (March 1, 2023). https://ssrn.com/abstract=4375283 or http://dx.doi.org/10.2139/ssrn.4375283

Isaiah Andrews and Maryam Farboodi, “Do Markets Believe in Transformative AI?,” NBER Working Paper 34243 (2025), https://doi.org/10.3386/w34243.

McKinsey & Company, “Who’s funding the AI data center boom? McKinsey & Company”, (2025) https://www.mckinsey.com/featured-insights/themes/whos-funding-the-ai-data-center-boom

Apollo Academy AI’s growing share in public credit markets. Apollo Global Management, (2025). https://www.apolloacademy.com/ais-growing-share-in-public-credit-markets/

Notes

Citadel Securities ran a client survey on the macro impact of AI, with approx. 100 institutional client responses across hedge funds, asset managers and corporates.

Copyright © Citadel Enterprise Americas LLC or one of its affiliates. All rights reserved.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CDGE”) authorized and regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch authorized and regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the Japan Financial Services Agency (“JFSA”); and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”), Financial Industry Regulatory Authority (“FINRA”), and Securities Investor Protection Corporation (“SIPC”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC, FINRA, and SIPC, or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity. Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at www.citadelsecurities.com/GlobalSalesTrading.

Explore

Market Insights - What We Do