We see focus starting to shift from the first order impact of the conflict – which has been characterized by a hawkish repricing of global policy during the kinetic phase – onto the second phase, in which the growth implications start to take center stage, as markets are forced to confront the reality of at least some demand destruction and the myriad butterfly effects of the conflict. We think lower forward real rates will become the primary channel via which markets trade the growth narrative once global front ends stabilize. News-flow of potential de-escalation this morning has naturally offered some relief to risk assets, but we think some lasting damage has been done to global supply chains, and that it is unlikely that markets will snap back entirely to the pre-war modus operandi. Nohshad Shah’s last two notes are a must-read to understand the escalation trap that has been driving the cascade of the conflict. It seems likely that we are approaching a crossroads for the conflict, in which it either meaningfully escalates or a pathway to a ceasefire is established. We see both scenarios as consistent with focus shifting to the negative growth implications of the conflict.

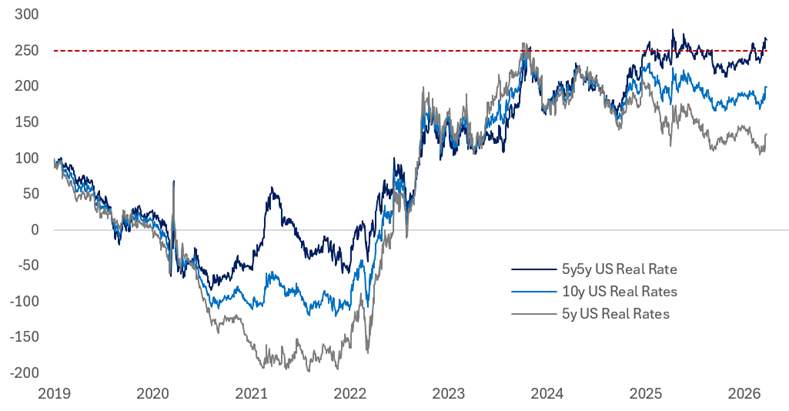

5y5y Real Rates Are Approaching Cycle Highs

5y5y, 5y and 10y USD Real Rates (bp)

Source: Bloomberg, Citadel Securities, Mar-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

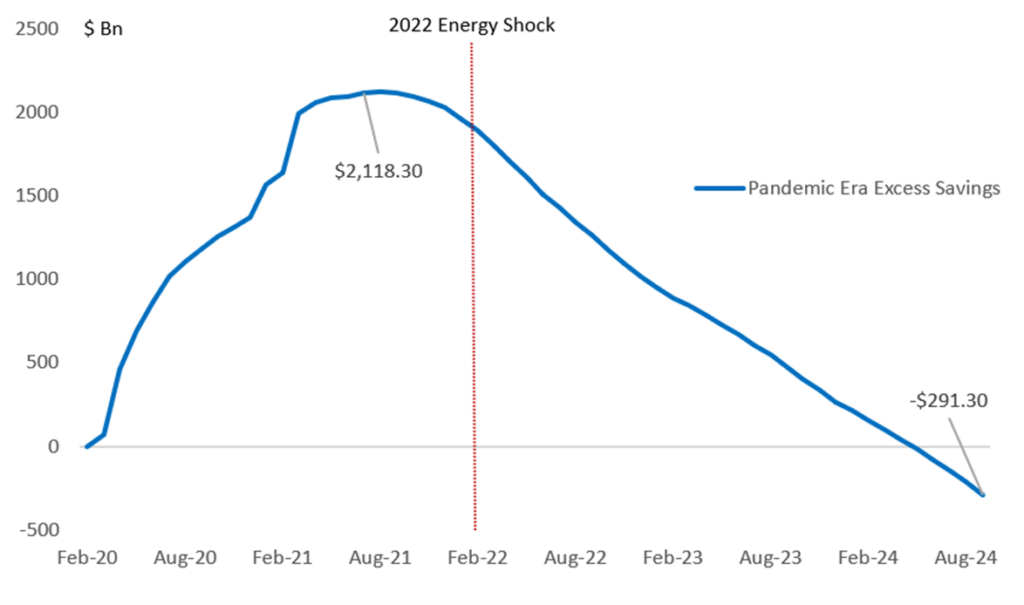

As we argued last week, the first phase of the conflict has played out largely along the lines of a hawkish policy shock, in which markets respond to the move in energy markets by aggressively rerating front end inflation forwards higher and moving policy pricing in a hawkish direction. The initial phase of the global front end move was driven by deleveraging, but the central bank communication last week implies that the energy shock is likely to elicit a policy response should energy prices remain elevated. This is broadly in line with the 2022 playbook, with both markets and central banks focused on the inflation implications of the energy shock. We think that the 2022 playbook is likely the wrong interpretation of how this plays out, as we see the global economy as likely more vulnerable today than it was in 2022. The 2022 energy shock came alongside an enormous positive demand shock in the form of global reopening, massive fiscal support and labor markets which were historically tight. Furthermore the deferred consumption of the pandemic had created a significant increase in excess savings, that made households uniquely resilient to higher energy prices.

Pandemic Era Excess Savings Were a Unique Consumption Buffer in 2022

Rolling Cumulative Pandemic Era Excess Savings as Calculated by San Francisco Federal Reserve

Source: FRBSF, Citadel Securities, Mar-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

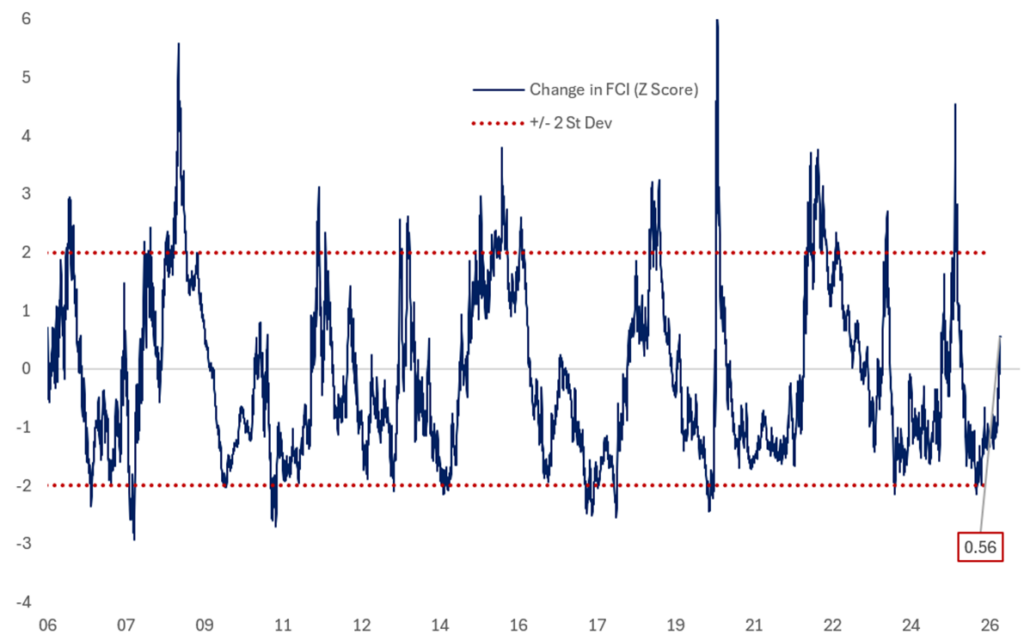

Despite the clear differences from the 2022 supply shock, central banks are likely to remain focused on the risk of a second inflation wave and the de-anchoring of expectations, even beyond the kinetic phase of the conflict. In the context of the volatility of energy prices, we think central banks will remain on high alert, but that once the second derivative of front-end pricing turns, forward real rates will price the growth implications of the significant supply chain disruption that looks somewhat unavoidable. Either the supply shock itself erodes demand in an environment that lacks the excess demand conditions of the prior cycle, or growth proves more resilient amid higher energy prices and supply chain disruption, in which case we think central banks will deliberately tighten to offset the inflation impulse. In both cases, the adjustment ultimately comes through weaker demand and lower forward growth. The mechanism through which financial conditions tighten is important as when driven by policy, tightening is typically painful but contained, as central banks retain the ability to reverse course. However, we consider that tightening can also be market-led, as deteriorating growth expectations widen credit spreads, compress equity valuations, and strengthen the dollar. In an environment where central banks remain hawkish while markets mark down growth, these forces can become mutually reinforcing. Weaker growth drives risk assets lower and the dollar higher, which in turn tightens financial conditions further and weighs again on growth. This dynamic is particularly acute in emerging markets, especially energy importers, where adverse terms-of-trade shocks pressure currencies and force central banks to tighten defensively to protect their currencies. This dynamic is more likely should the conflict persist, but its an important channel via which resulting weakness in EM assets feeds back into global growth and reinforces dollar strength, amplifying the tightening impulse at the global level.

Financial Conditions Are Not Close to the Reversal Threshold

Z-Score of US Financial Conditions

Source: Bloomberg, Citadel Securities, Mar-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

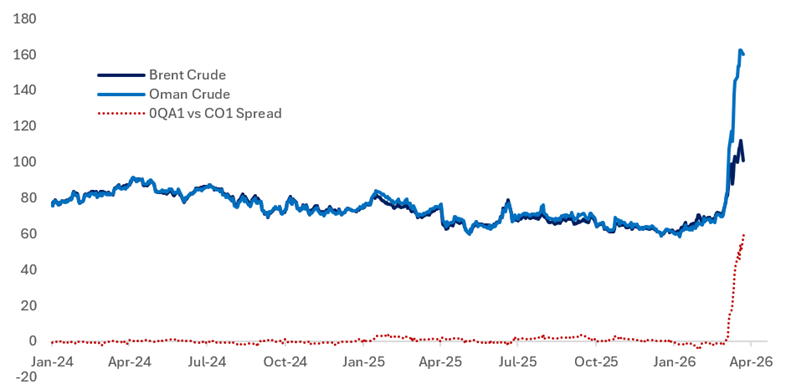

Furthermore, markets remain largely focused on crude futures, which appear to be materially understating the severity of ongoing physical shortages and the scale of supply chain disruption. Even in a scenario where the Strait reopens, we think that these dislocations may be unlikely to normalize quickly; instead, they are likely to persist for weeks, if not months, as inventories are rebuilt and logistical bottlenecks clear. Crude futures continue to trade at a meaningful discount to physical barrels being delivered into Asia. For instance, Oman crude is trading at $160/bbl, reflecting acute shortages and elevated physical premiums.

Crude Futures Appear to Understate Physical Shortages

Brent Crude + Oman Crude Active Contract Futures Prices

Source: Bloomberg, Citadel Securities, Mar-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

Importantly, the disruption is not limited to crude. Physical shortages across oil products, LNG, helium, fertilizers, and other critical inputs are likely to ripple through global supply chains well beyond the formal end of the conflict. This should not be viewed narrowly as an energy price shock but rather a broader supply shock with both price and quantity effects. We note that the quantity constraint is likely to prove at least as important as the price channel. As inventories are drawn down and the final cargoes that were already in transit prior to the Strait closure reach their destinations, the market will increasingly be forced to operate on reduced physical availability rather than buffered stockpiles. At that point, price discovery may shift decisively toward the marginal unit of scarce supply. We do not think that markets have fully internalized the second-order and “butterfly” effects that arise when upstream inputs become physically constrained. Disruptions in energy and industrial inputs can propagate nonlinearly across manufacturing, agriculture, and transportation networks, amplifying the initial shock. For example – physical shortages of helium could eventually represent a material headwind for the manufacture of chips and hence the data center build out, and given the energy intensity of the AI complex, we do not think this theme is immune from the butterfly effects of global supply disruption and concerns over future energy security. Nor do we think it is without doubt that the pace of AI capex will proceed unabated if global financial conditions tighten in a disorderly manner and growth expectations and risk appetite decline coincidentally. These risks recede somewhat if the kinetic phase of the conflict is shorter but are impossible to rule out given the more fragile nature of the global economy following this shock.

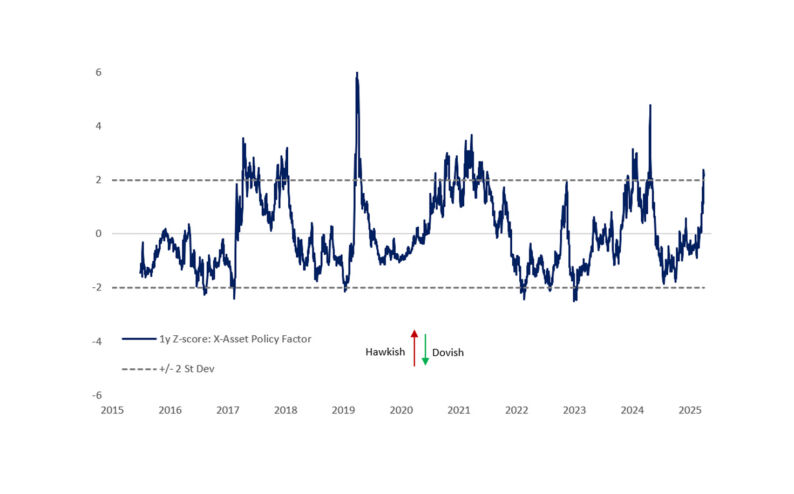

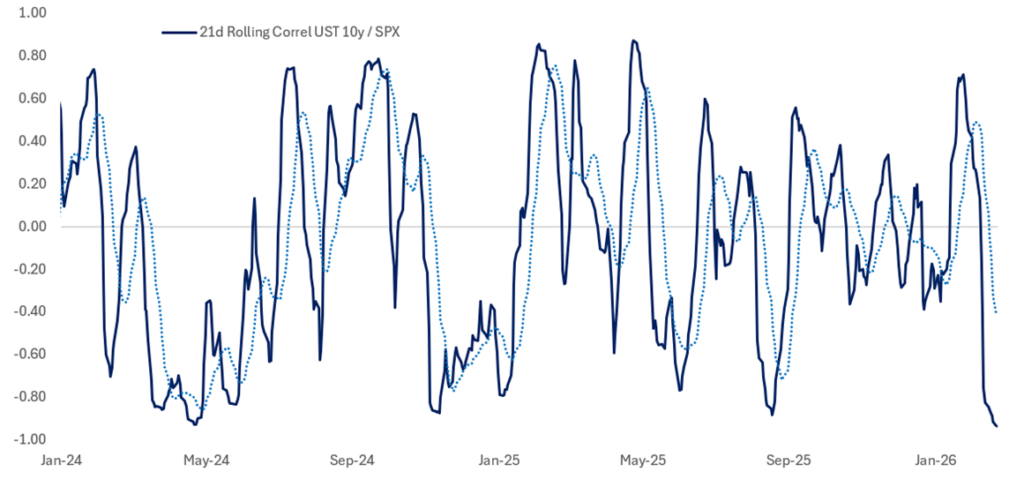

Stock Bond Correlations Imply A Hawkish Policy Shock is Currently Dominating Growth Concerns

21d Rolling Correlation: 10y UST Yield vs SPX

Source: Bloomberg, Citadel Securities, Mar-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

Markets were caught off guard by the initial phase of the conflict, as reflected in the sharp deleveraging in global front ends. The next phase is likely to be defined less by escalation dynamics and more by the extent of the growth shock. As the focus shifts away from a hawkish policy impulse toward weaker growth, the level and pace of tightening in financial conditions will be the key metric for spillovers. Once front-end rates reach a clearing level, we expect real rate forwards to flatten as attention turns to the growth outlook. In FX, dollar calls offer attractive asymmetric protection to a re-escalation scenario given the still-muted move in the dollar, while implied volatility remains low on a cross-asset basis.

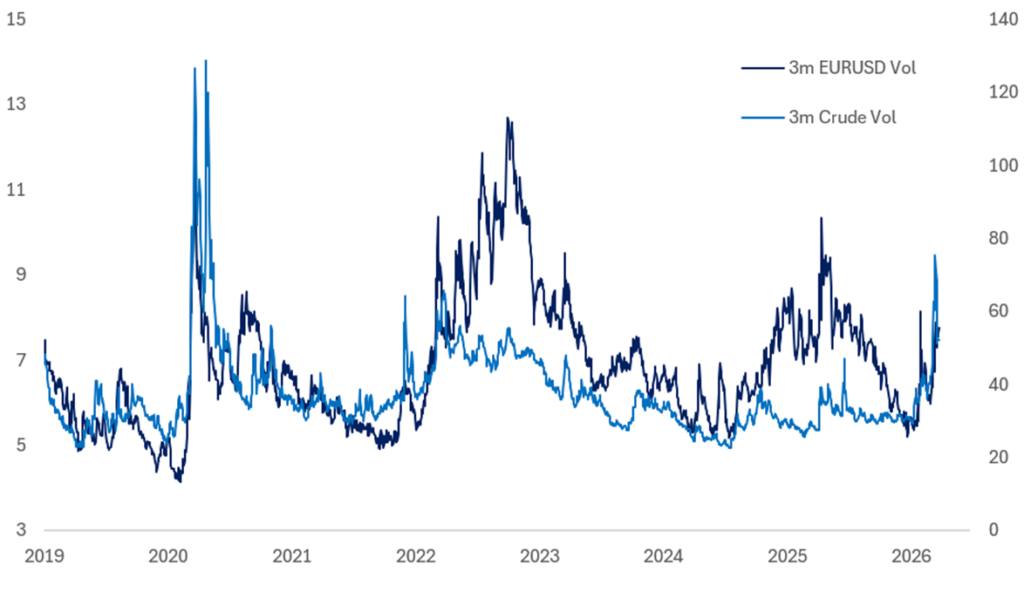

FX Vol Has Failed to Keep Pace With the Increase in Oil Vol

3m Crude + FX Implied Vol

Source: Bloomberg, Citadel Securities, Mar-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

Copyright © Citadel Enterprise Americas LLC or one of its affiliates. All rights reserved.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CDGE”) authorized and regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch authorized and regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the Japan Financial Services Agency (“JFSA”); and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”), Financial Industry Regulatory Authority (“FINRA”), and Securities Investor Protection Corporation (“SIPC”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC, FINRA, and SIPC, or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity. Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at www.citadelsecurities.com/GlobalSalesTrading.