By Nohshad Shah

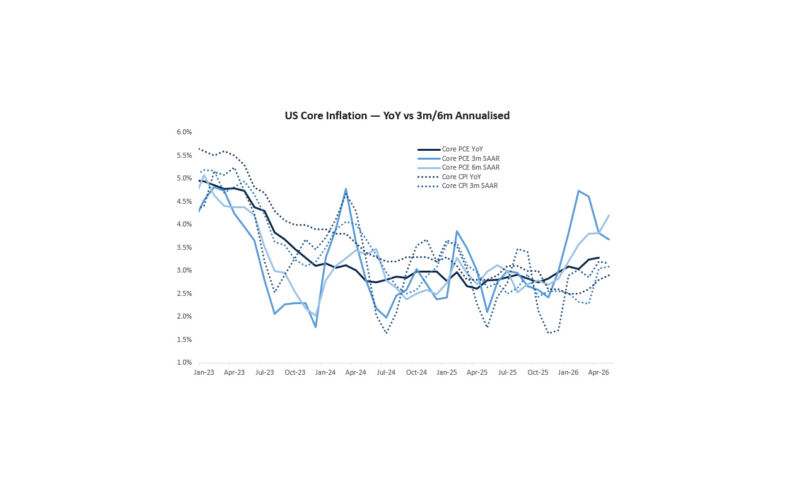

WHAT DID WE LEARN ABOUT THE US ECONOMY THIS WEEK?…The CPI and PPI data confirmed that inflation remains at uncomfortably high levels – with a number of components surprising to the upside, expectations for the translation into Core PCE (the Fed’s preferred measure) are now running at 0.33% MoM; 2.75% YoY…leaving the 3m and 6m annualized rates at 2.9% and 2.6% YoY, respectively. Bearing in mind this reading is for February, so before the impact of tariffs that are starting to be implemented (thus far 20% on Chinese imports and 25% on steel and aluminium)…these are not comforting numbers for the Fed. Indeed, one can reasonably expect that as the new Administration’s policy developments take their course, the tracking for core PCE can exceed 3.0% in the coming months…a full 1% above target. Moreover, the Fed has made it abundantly clear that inflation expectations are crucially important…and we got more bad news on this front with UMich Inflation expectations again coming in very high (1yr: 4.9%; L-T: 3.9%). For the Fed to materially cut rates with this inflation backdrop, recession risks will need to come to the fore – something which would typically be revealed in the labour market data. On that front, following on from last week’s NFP (151k; 4.1% u/e rate) we had initial claims come in below expectations at 220k, confirming that we are not seeing a material deterioration in the employment picture – typically, we would need to see an 80K+ spike in claims over a couple months to signal a recession. Within the context of DOGE layoffs, it is important to remember that government employees do not show up in claims data as they have a separate unemployment insurance program…but the picture here is very murky regardless with legal proceedings underway challenging the cuts and calling for reinstatement of some federal employees. As mentioned in my previous notes, there are risks to both sides for the labour market…immigration controls driving the u/e rate lower…or negative sentiment causing a recession and a sharp fall in employment. My sense is that the FOMC will view these risks as balanced…and what’s certainly clear is that the hard data is yet to reveal material weakness. But on inflation, the backdrop looks much more worrying…here, it’s less about the spot data…and more about the risks of an acceleration as President Trump implements his trade agenda. Chair Powell will not want inflation expectations to get out of control – which is a very real risk here. I would even posit the argument that the Fed would be ok with getting behind the curve a little, knowing that it’s easy for them to cut rates deeply, but more decisively, once we have a clearer picture of how much the economy is slowing. Next week’s retail sales will be a useful guide…consensus expects +0.3% (control) following the -0.8% last month…anything substantially more positive will call into question the recession narrative and front-end rate cut pricing will calibrate further.

Source: US Dept of Labor

PRESIDENT TRUMP AND SECRETARY BESSENT…have made it clear this week that the focus is squarely on getting their trade agenda implemented and not on the stock market. Risk assets have taken this at face value in recent weeks, continuing to sell-off with NDX -11% and SPX -8% from the peak. The technical picture has indeed been challenging with momentum and factor unwinds, as well as CTA selling all playing a role. Though difficult to say, it feels like we are in the latter innings of this move and on Friday the market started to stabilize for the first time in a while. However, for a substantive move higher in risk assets, we likely need a positive tier 1 macro catalyst…assuming the back-and-forth on tariffs continues. It’s fashionable these days to say there’s no “Trump Put” on equities…but make no mistake, this is real wealth destruction for US citizens (including for many of the folks surrounding the President)…and with a sizeable ongoing impact on American companies. My expectation would be that CEOs are voicing their concerns privately…so perhaps there may well be a ”Trump Put”…just further out-of-the-money than most expected. More concerningly, the implications of a strategy to eliminate the US trade deficit, including with allies, has profound implications for global asset prices over the medium-term. Most of the trade surplus from large foreign countries goes into US equities and bonds…THE global benchmark assets…a profitable relationship for both sides. If the trade war escalates, it’s easy to see a de-coupling of this multi-decade relationship…with a dramatic impact on stock prices and bond yields as countries reduce their exposure to US assets. It is tough to predict where we will land on the spectrum of outcomes for tariffs with so much uncertainty on the table…but we will find out more around the 2nd April deadline. All of this is the true price of “America First”…and why I continue to favour USD fx weakening.

source: Bloomberg

IN EUROPE…the good news continued with an agreement for a large fiscal package in Germany. Chancellor Merz has agreed a loosening of the country’s “debt brake” for defence spending with discussions of spending now exceeding 3% of GDP. In addition, there will be a 500bn infrastructure fund, with 20% earmarked for green transition in a comprise with the Greens…and individual states can now issue debt up to 0.35% of GDP. The package will go to a vote in the Bundestag on 18th March and then The Bundserat on 21st March but is expected to pass with no further hurdles. As mentioned last week, this is a very material boost to the EU economy…and with further measures to come from other EU countries, it creates a backdrop of growth momentum in the region. This is already starting to be reflected in the outperformance of European stocks (Estoxx +10% YTD), EURUSD (+5% YTD) and the sell-off in 10y bund yields (+50bps YTD). As this theme continues to proliferate, I would expect more of this price action with global investors increasing their allocations to European assets. I doubt the ECB will be cutting rates much beyond once more…so if you embed more term premium into the yield curve and inflation persisting above 2%…with greater issuance in the future, it’s reasonable to see EUR 5y5y yields 50bps higher from here over the medium term.

source: Bloomberg

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/