-

Who We Are

- What We Do

Series: Some Macro ThoughtsDovish Powell / Hawkish Commitee

By Nohshad Shah

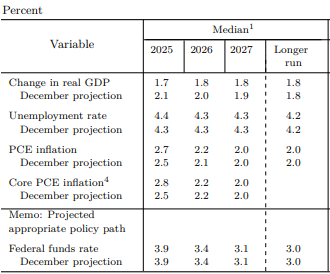

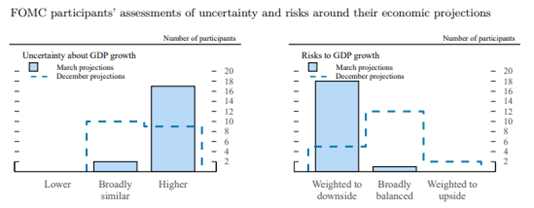

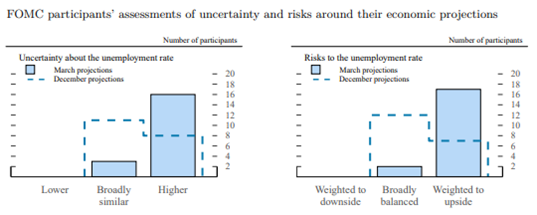

THIS WEEK’S FED MEETING REVEALED A DOVISH TONE FOR MARKETS. In the SEP, the 2025 median expectation for growth was revised down (1.7% from 2.1%), the unemployment rate was revised up (4.4% from 4.3%)…yet core PCE moved higher (2.8% from 2.5%)…typically not a set of outcomes that would sit well with any central bank. The median dot for the policy rate remained the same at 3.9, still implying two cuts…but looking under the hood, we have gone from one outlier not forecasting any cuts in 2025 to now a quarter of the FOMC…indeed the 2025 median dot would have been one cut if two more committee members had shifted. Nevertheless, Chair Powell struck a more balanced tone, seeming to dismiss the forecast changes in a highly uncertain and volatile backdrop. This was reflected in the FOMC participants’ assessments of uncertainty and risks around their economic projections…with weightings to the downside on growth and upside to inflation (see below). Essentially, the Fed is anticipating a challenge to both sides of their mandate – higher inflation, but lower growth…and with an employment picture that remains stable so far. In my mind, Chair Powell is taking a pragmatic approach, something we’ve seen often from the Fed in years past…he is biding his time in a volatile environment and will adapt rapidly to changing conditions on the ground without getting attached to dogma around prior assertions (c.f. inflation expectations). At the moment, there is no need to signal cuts – the hard data is not weak enough. Moreover, my sense is that amidst a jittery market with heightened policy uncertainty he didn’t want to sound more hawkish than needed either…nor indeed did he want to antagonize the Trump administration. For markets, this reveals a dovish preference…with a heightened sensitivity to any weakness in the labour market and concerns around growth…with much less emphasis on inflation prints. This is a green light for front-end rates to rally…even more so should we get a weak NFP or deterioration in activity data. Terminally, I continue to believe that given core PCE inflation remains above target (with risk of it rising w/tariffs to 3% and above), the Fed will still need to see a significant deterioration in the employment picture to cut rates deeply. But this week we learnt that should that indeed materialize, there is no doubt which side of the dual mandate that the Fed would emphasize. However, it’s certainly worth remembering that the hard data has repeatedly confounded US recession expectations throughout this cycle…

Source: US Federal Reserve, Summary of Economic Projections 19mar25

THE FED ALSO ANNOUNCED A MEANINGFUL SLOWDOWN IN THE PACE OF QT…moving the cap on monthly redemptions of Treasuries to $5bn from $25bn. Chair Powell insisted that this move did not reflect concerns around the debt ceiling nor was it linked to monetary policy. As a reminder, the debt ceiling – the limit to borrowing to fund ongoing deficits – was re-implemented this year….which means that until it’s raised or suspended, the Treasury cannot issue net new debt. This will likely come to the foreground sometime this summer, when the coffers will run dry and Congress will have to raise the ceiling (with some of the usual back and forth). With that context, the slowdown of QT will be a positive development as elevated QT + increased net issuance may well have led to a heightened focus on constrained liquidity in the system. Again, this signals Chair Powell was keen to ease liquidity pressures in the broader ecosystem. Along those lines, it’s been interesting to see the shift in Secretary Bessent’s stance on Treasury issuance. Having criticized Janet Yellen’s focus on bills against longer-dated bonds as akin to quantitative easing, it seems Bessent is likely to continue doing exactly this, stating that issuing more long-end USTs was “a long way off”. Why the change of tune? As mentioned in previous notes, this Administration is more focused on controlling long-end yields than anything else…given its importance in determining financial conditions. Moreover, as I’ve mentioned before, my suspicion is that there is a chronology in mind for President Trump’s economic policies…first, get the tariff agenda done (a consistent theme for Trump since the 1980s), with some related pain around the uncertainty of its implementation…then move onto the growth side of the equation…in other words, deregulation, lower energy prices and most importantly, tax cuts. I continue to believe that there will be a material fiscal boost from this President’s agenda that will be more than just an extension of TCJA…but all in good time. A recession doesn’t have to be part of this plan…but if one materalises…are we still in the window where President Biden can be blamed? Either way, lower long-end yields are absolutely fundamental to this chronology…however they are achieved.

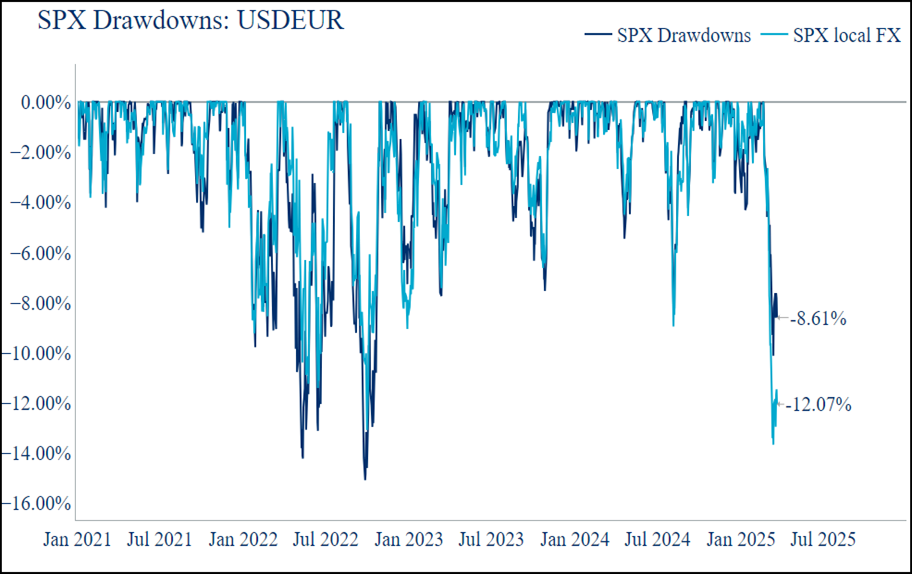

THE BIGGEST CONCERN FOR RISK MARKETS continues to be the uncertainty around tariffs. The expectation is that 2nd April will bring the announcement of a “reciprocal approach” framework under the guidance of US Trade Representative Jamieson Greer. Reports suggest he has brought discipline and rigour to the process and reinstated aspects that were missing from prior tariffs implemented on Canada-Mexico and China such as a formal process of receiving feedback from corporates. In addition, there are reports of a simplification of new tariff rates by sorting nations into a tiering system incorporating three levels, thereby avoiding some of the complexities…and Secretary Bessent noted that there was a focus on a “dirty 15” group of countries with the largest trade surpluses against the US. It seems to me that the Administration is trying to get more of a handle on the narrative and tighten up the process…time will tell if this will be enough to stall the slide in equities. As mentioned last week, the broader implications of a strategy to eliminate the US trade deficit will have profound implications for global asset prices in the medium term – something that markets have not fully appreciated. Following 2nd April, if the trade war escalates, it’s easy to see global investors drive the de-coupling of their historical overexposure to US assets, with a dramatic impact on both stock prices and bond yields. In the first instance, this would involve non-US investors fx-hedging their unhedged exposure to US assets. Traditionally, in a typical “risk-off” scenario USD strengthening provides a buffer against equity market drawdowns. However, what we’re now seeing is risk-off with a weaker USD, which amplifies losses (chart below; h/t Grant Wilder). Beyond this, investors will look to diversify their investments into non-US assets…we are already starting to see this with ETF flows into Europe, where equity valuations remain cheap on a relative basis to US, and with the boost from fiscal policy, the growth outlook has materially improved (as have the attractiveness of bund yields). Not quite the end of US exceptionalism…but watch this space.

Source: Citadel Securities, Bloomberg 21mar25

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Market Insights - What We Do