-

Who We Are

- What We Do

Series: Macro ThoughtsInflation, Remember?

By Nohshad Shah

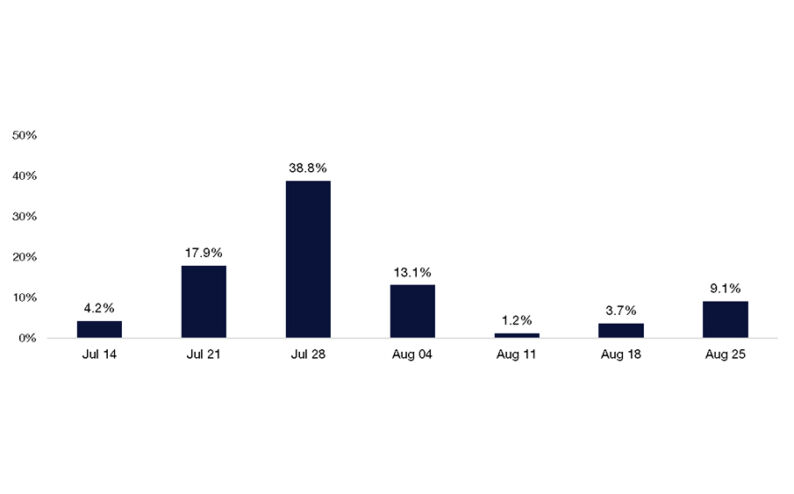

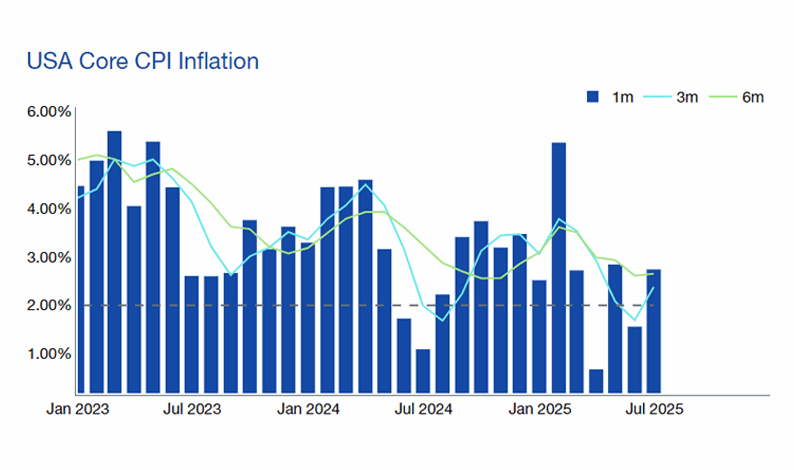

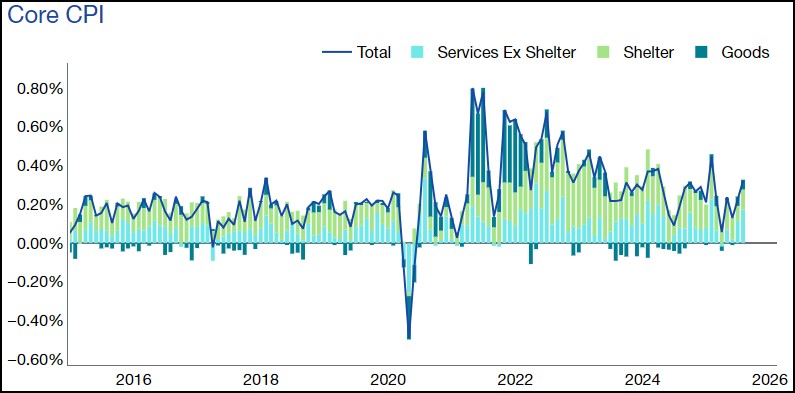

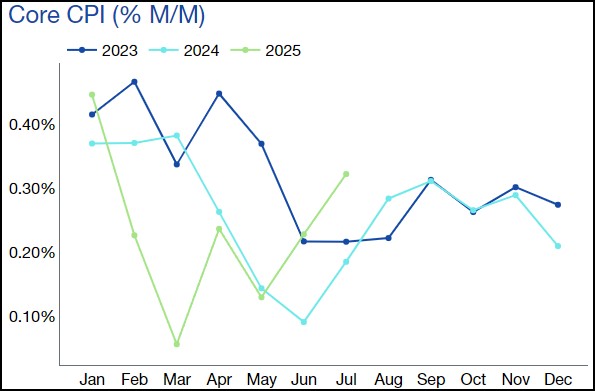

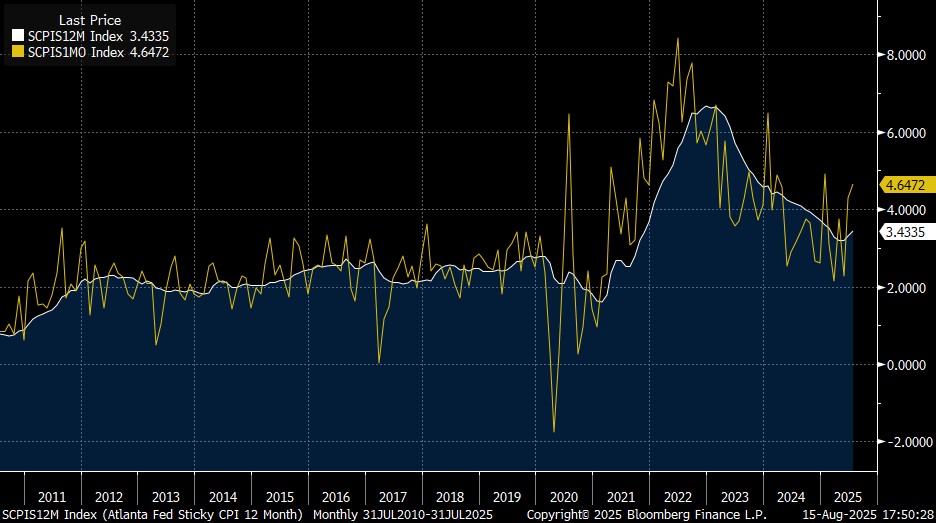

THIS WEEK’S DATA WAS A TIMELY REMINDER THAT INFLATION REMAINS A PROBLEM FOR THE FED. Core CPI came in 0.32% MoM (3.1% YoY), which the market interpreted as dovish due to the core goods component at 0.21% MoM…but more concerningly, core services was materially stronger than expected at 0.36% MoM. This paints a worrying picture – tariff-induced inflation has yet to show up in a meaningful fashion…likely due to some mix of inventory accumulation, which allowed retailers to be patient in adjusting prices…and simply more benign assumptions about tariff outcomes in the aftermath of liberation day. But there are worrying signs in the PPI data, which does not include import prices, but via supply chains showed significant price pressures are building with intermediate production inputs rising and core goods +0.38%. More broadly, the post-COVID seasonal pattern in CPI has been one of muted inflation during summer…so when looking at the number through this lens, it was actually quite elevated (chart below). The on/off nature of tariff deals and implementation lags has meant that the pass-through from tariffs is yet to appear in a significant way…but that does not mean it won’t…as we’ve heard from retailers during Q2 earnings statements, price rises are coming soon. Now…if inflation was close to target and we had a clear tariff shock, then it would be plausible for the Fed to look through this as a one-off price level shift. Instead, in essence what we have is accelerating sequential inflation in services, just ahead of a likely sustained move higher in core goods inflation…which means a much greater risk of second round effects and potential for stoking inflation expectations…especially if we start to see higher wages due to reduced labour supply stemming from immigration controls. Another concerning sign can be observed in the Atlanta Fed’s “Sticky-Price CPI”, which displays a weighted basket of items that change price relatively slowly (based on the frequency of their price adjustment)…which rose 4.7% annualised for the month of July and stands at 3.4% on a 12-month basis (chart below)…suggesting underlying price pressures are creeping up from an elevated baseline. All said and done, most expect Core PCE (the Fed’s preferred measure) to come in at 0.30% MoM, leaving the YoY rate at 3%, a full 1% above target prior to tariff effects. In sum, when I survey the landscape for the US economy I see the Unemployment rate at 4.2%…Initial Claims at ~220k…Composite PMI at 55…the easiest financial conditions (FCI) in 3 years…an ~11% devaluation of the broad-based dollar index (DXY)…forward fiscal stimulus of ~1% of GDP….and perhaps some “tariff dividend” cheques coming in the post worth some part of $300bn (the estimated tariff revenue for 2025). Do these conditions warrant the 130bps of rate cuts priced by the market through next year?? I would argue No. But, investors have taken their cue from i) the recent weak payrolls report, and ii) dovish rhetoric from Treasury Secretary Bessent, who this week suggested “there’s a very good chance of a 50 basis-point rate cut” in September and “we should probably be 150 to 175 basis points lower”…in what seems like the beginning of the “shadow chair” phase of monetary policy. The rates market is convinced that the Fed will be able to deliver rate cuts regardless of the economic backdrop. Whilst the spot incentive for FOMC members to highlight their dovish credentials is clear (especially if auditioning for the Chair), once President Trump makes his choice, that incentive expires. This will leave the committee in a position to think critically about the legitimacy of a protracted rate cutting cycle…and should the prevailing conditions not warrant it, the front-end of the rates market may well be forced to course-correct. Market participants playing for the 50bp cut in September beware.

Source: BLS

Source: BLS

Atlanta Fed Sticky CPI (12m & 1m annualised)

Source: Bloomberg, Federal Reserve Bank of Atlanta

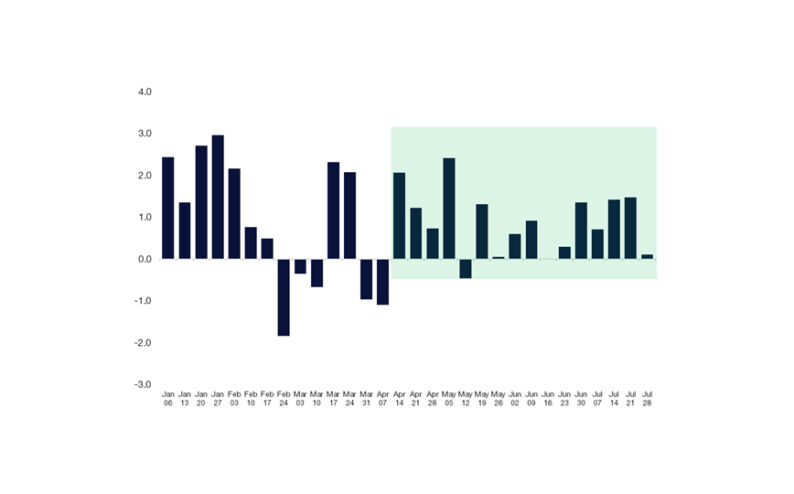

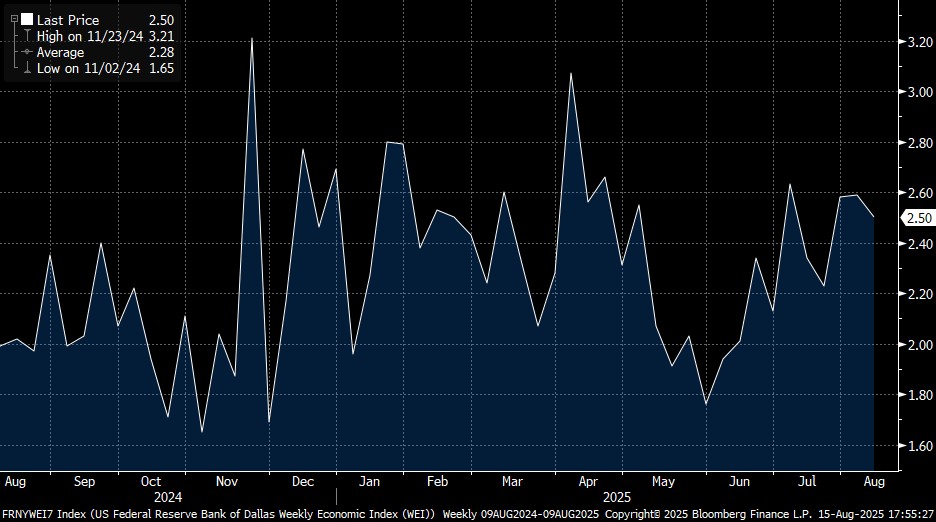

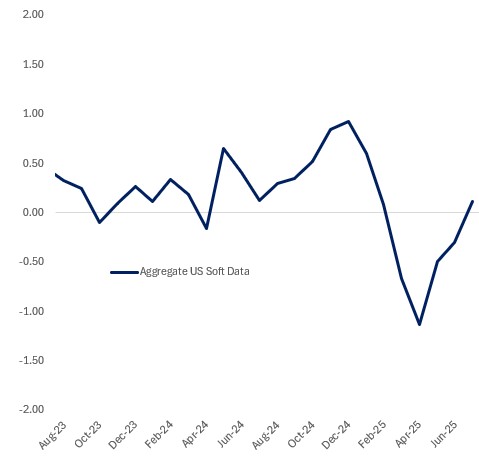

WHAT ABOUT GROWTH? Regular readers will know that my core view has been that growth and the labour market have been moderating from strong levels, but we are not going to see a recession anytime soon…and more importantly, the forward outlook for growth has been on a positive trajectory since May. This continues to be the case with the Dallas Fed’s WEI running at a healthy 2.50% (13-wk moving avg. 2.23%) and similarly, the Atlanta Fed’s GDP Now is at 2.55%, driven by upgrades to consumer spending (Real PCE est. 2.2% vs 1.4% in Q2) …far from recessionary and well-above what most would consider trend growth ~1.5%. Retail Sales (control group) exceeded expectations this week at +0.5% including a meaningful upward revision in the prior month to +0.8%, revealing a solid 3-month trajectory with positive implications for the next round of GDP numbers. Indeed, looking at the soft data in aggregate can sometimes be informative for the trajectory of the economy…here, we can see a very substantial positive trend since the lows of April (chart below). Consumer spending, which represents 70% of US GDP, continues to remain strong – in a recent paper from the Boston Fed the authors find that since 2022 real aggregate spending has been supported by high-income consumers and the amount of credit card debt held by this cohort has yet to catch-up to pre-pandemic levels (although that is not true of low-income consumers). Factors such as this and the boost from high stock and housing prices have supported household wealth and therefore consumption and will continue to do so. Going back to policy, should the Fed deliver the 5-6 rate cuts that are now priced into the market, then the economy will be running hot…especially when you take into account the 2026 GDP contributions from the rolling impact of FCI easing (+0.5%), President Trump’s fiscal package (+1%) and tariff dividends (+0.5% assuming half is paid out). And this is exactly what this Administration wants, especially heading into the mid-term elections next year.

Dallas Fed Weekly Economic Index

Source: Bloomberg, Federal Reserve Bank of Dallas

Aggregated US Soft Economic Data

Source: Haver

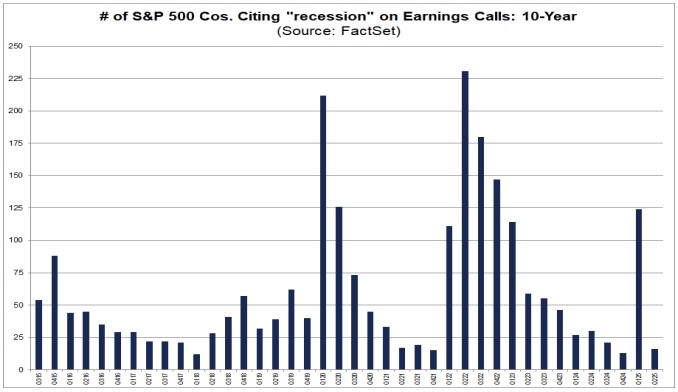

THE IMPLICATIONS FOR ASSET MARKETS: the always-prescient equity markets have started to upgrade the growth outlook with cyclicals v defensives having a sharp +4% move on the week (chart below), the best performance in some time. This represents a signal that this market is becoming more optimistic about the growth outlook with a heady mix of easy monetary and fiscal policy at a time when growth is likely picking up and the labour market (as represented by the unemployment rate) remains solid. An upgrade to nominal growth will continue to support the equity market and institutional sentiment remains subdued, relative to the backdrop, so I expect this bullish run to continue. A full 81% of S&P 500 companies have reported a positive EPS surprise and YoY earnings growth sits at 11.8%, which will be the third consecutive quarter of double-digit earnings at the index level…all during what most expected to be a subdued quarter amidst tariff-driven uncertainty! Indeed, according to Factset document search, the term “recession” was cited 87% less during this quarter compared to Q1 and well below the 10-year average. So…Corporate America is doing what it does best – adapting to conditions and finding a way to win. Meanwhile, 10y rates remain in the 4.0-4.60% range that I’ve talked about for some time – whilst there’s no immediate catalyst for a breakout, the medium-term dynamics will partly depend on the Fed’s actions…the more credible it’s moves, the more stable the rate. But, if the opposite starts to materialise, don’t expect the bond market to play ball forever.

US Cyclicals vs Defensives

Source: Bloomberg

Source: Factset

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Market Insights - What We Do