By Nohshad Shah

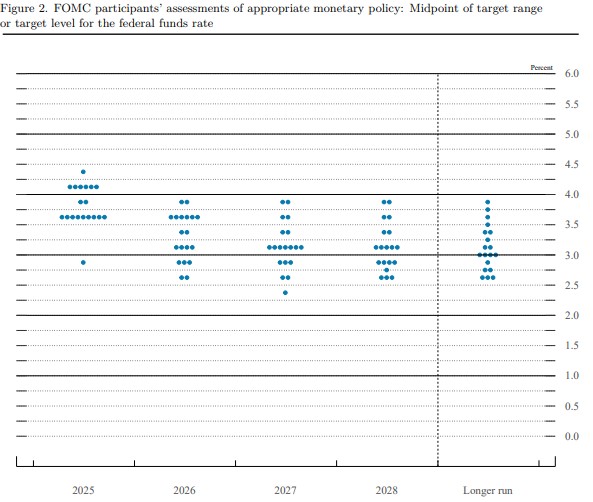

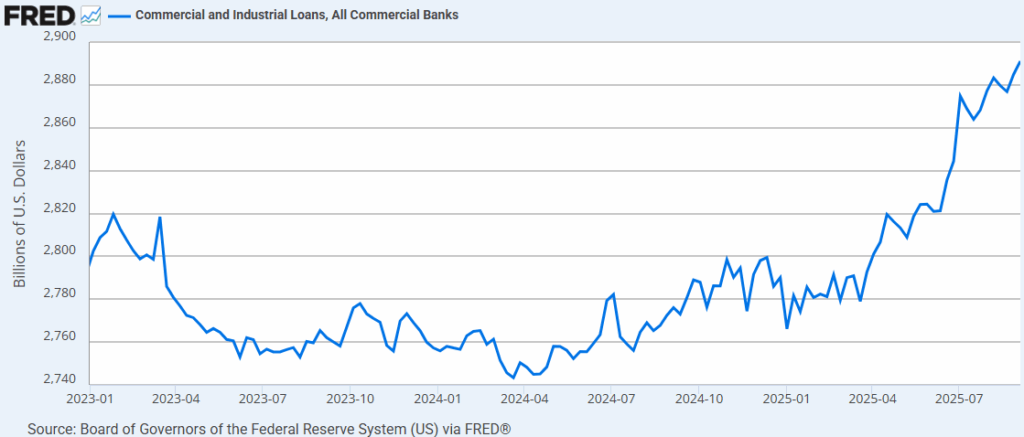

THE FED’S INSURANCE CUTS BEGAN THIS WEEK WITH A 25BP CUT AND CONFIRMATION OF A DOVISH BIAS TO POLICY, LIKELY FOR THE REMAINDER OF THE YEAR. The Summary of Economic Projections (SEP) revealed a three-cut median for policy rates in 2025 (from two in June), meaning we should expect further 25bp adjustments in the October and December meetings as the base case. Both the statement and Chair Powell’s presser confirmed that “downside risks to employment have risen” and whilst he did pay heed to “two-sided risk” and that there is “no risk-free path” given the challenges to both sides of the mandate, let’s be very clear about what has happened – Powell has changed his own emphasis to labour market weakness, and with it, the core of the committee. The balance of risks have shifted in his mind, and he is not going to tolerate a heightened risk of runaway unemployment for inflation that is above target (forecast 3% for 2025) but not considered to be at risk of accelerating. This confirms, in my view, a level of inflation tolerance (3% is the new 2%?) that is increasingly becoming the norm amongst central bankers and leaves no doubt as to which is the favoured child in the Fed’s dual mandate. Interestingly, the 2026 forecasts were revised in a more hawkish manner – more inflation (2.6% from 2.4%), stronger growth (1.8% from 1.6%) and a lower unemployment rate (4.4% from 4.5%)…at the same time as reflecting only one further cut in 2026. This implies that front-loading insurance rate cuts this year will protect the labour market and prevent the economy from slowing…then allowing a more gradual path for both policy and inflation back to target (not predicted until 2028). This seems sensible to me…if the spot concern is the labour market, then heading off this weakness with rate cuts now makes sense…and by December you will have more information to judge the balance of risks to the labour market, as well as the full impact of tariff-induced inflation passthrough. The SEP also revealed potential future fractures within the Fed…nine members put two or fewer rates cuts for 2025 and one maintained a no cut forecast (likely Beth Hammack of the Cleveland Fed)…on the other side, Governor Miran dissented at the meeting (in favour of a 50bp rate cut) and penned 150bp of rates cuts for 2025 in his dots, in line with what both President Trump and Treasury Secretary Bessent have been calling for, again raising the spectre of politicization of the Fed. Market participants should anticipate more dissents in the future. Still, Chair Powell maintains a firm grip for now and the group with the three-cuts median dots likely represents the core of the FOMC…including Governors Waller and Bowman, who notably did not dissent despite aspirations for the next Chair. Challenging Fed independence may not be all that straightforward. In sum, the Fed has committed to a series of rate cuts into the end of this year, driven by the spot labour market weakness – Powell is simply not going to risk a further deterioration for the sake of bringing inflation back to target. This means that financial conditions are going to get even easier…even though they have been on a consistently easier path since April’s tariff shock (chart below). As regular readers will know, my view is that the forward outlook for US growth is strong – corporate earnings remain solid (est. 7.7% YoY for Q3), household balance sheets are healthy (chart below), consumption remains stable (retail sales control group +0.7% this week), commercial loan growth is accelerating (chart below), we have a once-in-a-generation AI capex investment boom underway ($400bn and counting), and government policies designed to boost the supply side of the economy (deregulation, energy infrastructure, tax cuts). Throw in policy easing…both monetary and fiscal…and this is a heady mix. The forward-looking soft data are inflecting upwards. I do not see a recession anytime soon.

Federal Reserve Dot Plot

Source: Federal Reserve

US Financial Conditions Index

Source: Bloomberg

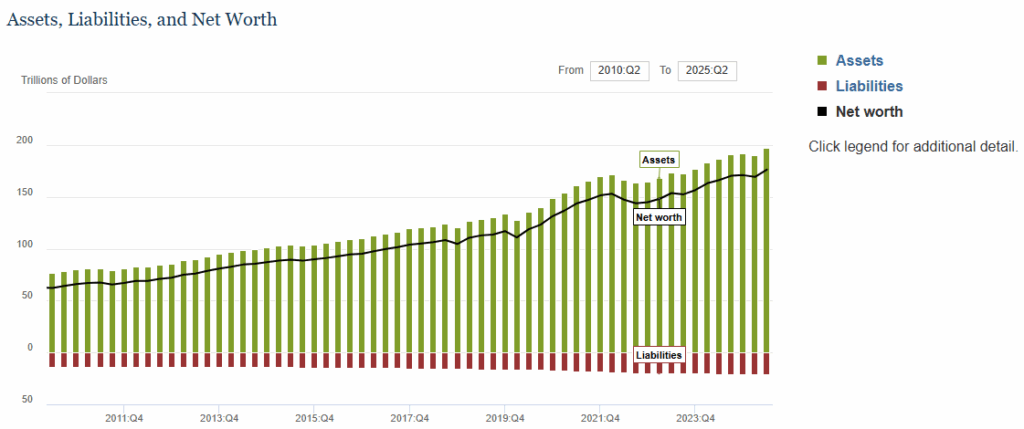

Balance Sheet of Households and Nonprofits

Source: Federal Reserve

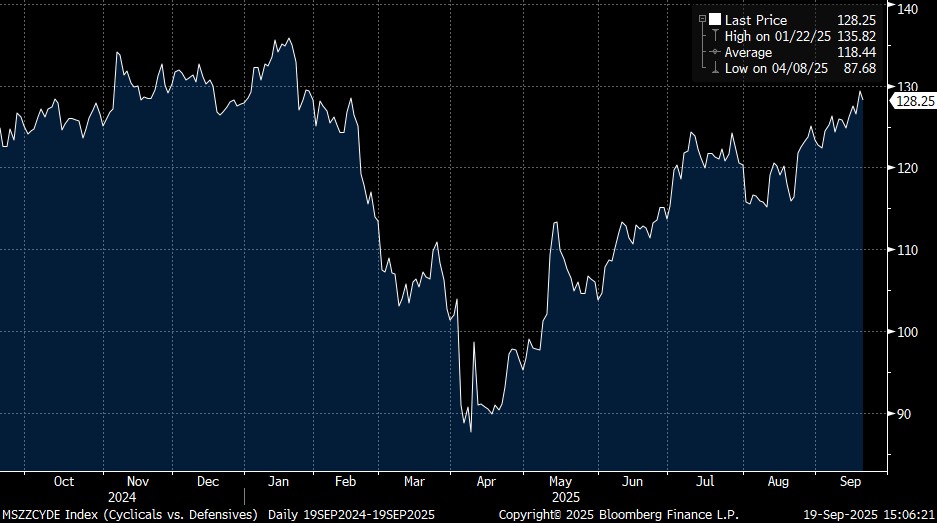

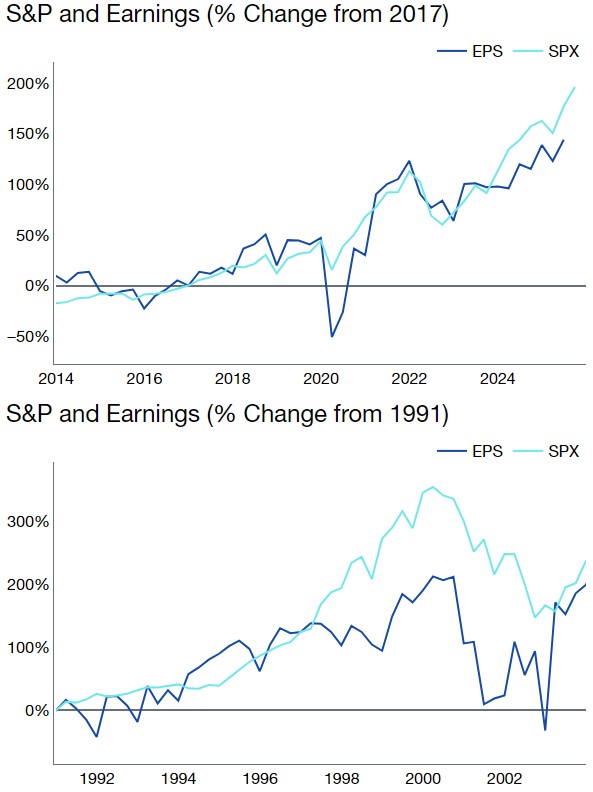

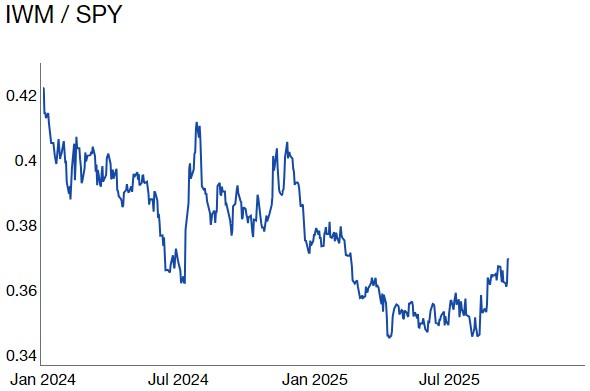

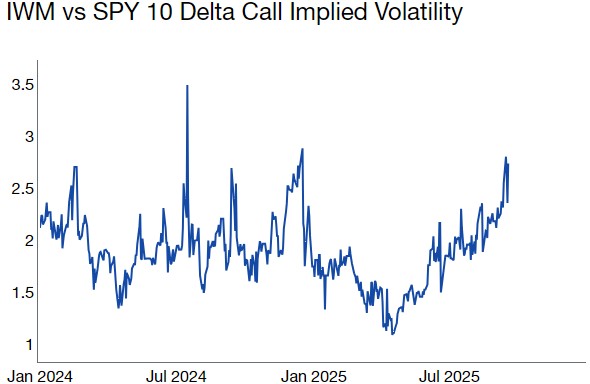

WHERE DOES THIS LEAVE MARKETS? RISK-ON…is the only conclusion when FCI is easing this much (most since May’22). This is a green light for risk assets to outperform – in equities, cyclicals v defensives (chart below) should continue to rally as the market upgrades the forward growth outlook. In addition, the Fed’s emphasis on easing rates regardless of inflation should support interest-rate sensitive sectors of the market – namely small caps and unprofitable tech. IWM has room to catch up to SPY and the pick-up in implied vols for calls suggest a focus in this direction (charts below). What could derail the rally in risk assets? First – a collapse in activity and the labour market leading to a sharp recession – the data does not support this…Dallas Fed WEI tracking at 2.26% (amongst many similar trackers) and Initial Claims dropping back down to 231k this week, after rising for two weeks. Second – valuations becoming too rich – S&P EPS has kept pace with index performance, unlike past peaks in p/e ratios (chart below). Third – accelerating inflation – if I’m right about forward growth, this will become a concern…but it seems to be taking a backseat for now. Fourth – a sharp rise in long-end bond yields – with a dovish monetary policy impulse and bond vigilantes MIA, it seems we need a trigger of some sort for this to happen. Indeed, the risk is that asset managers extend duration, given the front-end is now priced dovishly (1y1y swap ~3%) for a non-recessionary environment (which may well pose a risk to long held steepener positions). And finally – unknown risk factors – which could transpire at any point. ULTIMATELY, THE FED’S DOVISH STANCE ONLY MAKES ME MORE BULLISH ON THE US ECONOMY. RISKS MAY MATERIALISE, BUT FOR NOW FOCUS ON THE RIGHT TAIL.

US Cyclicals v Defensives Stocks

Source: Haver

Source: Bloomberg

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/