By Nohshad Shah

PRESIDENT TRUMP’S MISSIVES ON FRIDAY ROILED MARKETS…as he threatened the imposition of additional 100% tariffs on China and suggested he would cancel a planned summit with President Xi. The measures are to be introduced on 1st November or sooner, depending on China’s reaction and seem to be driven by what POTUS views as an “extraordinarily aggressive position on trade”. China announced large-scale export controls on rare earth minerals on Wednesday, which are critical components in the manufacture of everything from semiconductors, EVs to smartphones and fighter jets. The move was widely seen as a ploy to exert leverage ahead of summit negotiations, especially given the strong hand that the country has…as a reminder, China controls 70% of rare earth mining, 90% of separation and processing, and 93% of magnet manufacturing according to FT analysis. Make no mistake, this is a big deal…US manufacturers have warned that they might even have to cease production without rare earth magnets with foreign companies needing China’s permission to export magnets that contain even tiny amounts of rare earth materials (or produced using the country’s extraction mechanisms, refining or magnet-manufacturing technology). Time will tell what this dramatic escalation leads to, but for markets that had very little “tariff escalation” priced, it was a salient reminder that trade impacts are not over…if implemented, this would lift the effective tariff rate for the US economy from ~18% to ~30%. There are other signs of concern for investors…most notably the recent widening in HY and IG credit spreads (chart below) driven by lower quality consumer credit and parts of private credit (triggered by concerns about Tricolor/First Brands contagion)…the continued rally in Gold, which suggests a mix of both dollar diversification and a desire to move away from fiat currency (as well as now a momentum play)…and the US government shutdown, which presents meaningful risks should it extend for many weeks (more on this below). Downside risks remain present (and underpriced). Friday’s news illustrates the vulnerability of equity markets to shocks at these valuations.

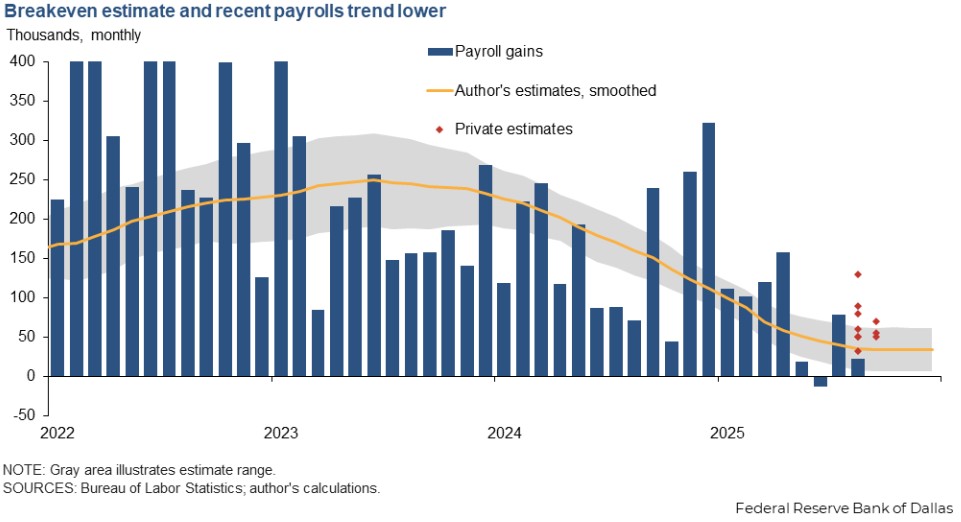

ANOTHER OVERLOOKED RISK IS INFLATION…which follows naturally from the rare earth restrictions that are essential to US supply chains and come on top of existing tariff-driven goods inflation pressure (as well as elevated services). Bond markets have been sanguine because of weakness in labour markets, allowing the Fed room to ease on the assumption that supply driven inflation will be transitory. But…new research from the Dallas Fed paints a picture of breakeven payroll growth that is alarmingly low. The paper confirms that the most important factor in recent volatility of the labour force has been net migration. The analysis shows a significantly higher peak in population growth in 2023 and a much steeper fall in 2025 compared to prior estimates. Taking this into account and incorporating other factors such as labour force participation and the structural ratio, the article concludes that the breakeven level of monthly payroll growth has dropped from a peak of 250k in mid-2023 to an estimated 30k in mid-2025 (chart below). This should concern Fed officials because it implies that labour market slack is much less than estimated and therefore the bar for overheating the economy and generating more unhealthy inflation is low. If there is genuinely less slack in the labour market than most estimates, then inflation could pick up fast in the current backdrop…from levels which are already ~1% above target. Bond markets are unlikely to ignore this.

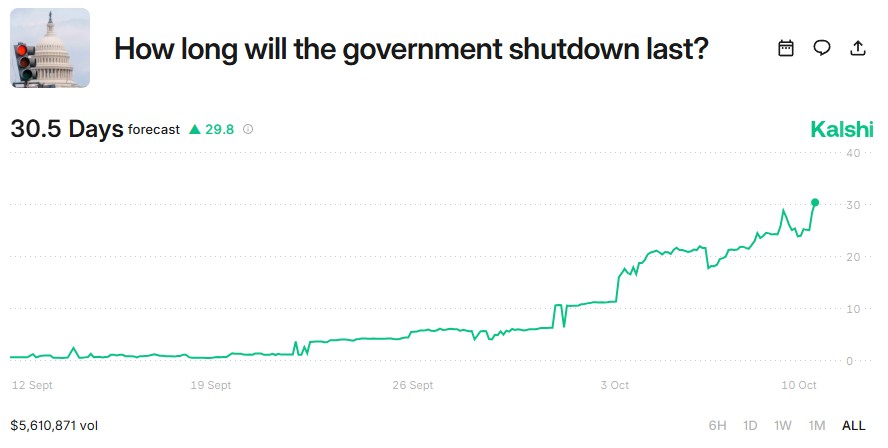

THE US GOVERNMENT SHUTDOWN CONTINUES WITH LITTLE SIGN OF IMMINENT PROGRESS. The market remains relaxed about the ongoing deadlock…likely because historical shutdowns have been relatively short-lived and the economic cost has been limited. FOMC staff estimate the impact of a government shutdown to be 0.2% of quarterly annualized GDP per week that the shutdown lasts, though this estimate does not include impact from financial conditions or market disruptions…although the payback is generally assumed to be symmetrical in the subsequent quarter following the reopening. The market’s calm reflects historical precedent…but I see scope for this shutdown to pose greater risks than prior ones. First – polling tends to show that the party holding out for concessions on unrelated spending topics tends to get the blame for the shutdown…but recent polls from The Washington Post found that 47% blamed President Trump and Republicans in Congress for the shutdown while only 30% blamed Democrats. This substantially reduces Senator Schumer’s incentive to agree to re-open the government without concessions on healthcare subsidies and risks drawing out this saga, thereby avoiding the “normal pathway”. Kalshi odds forecast the shutdown to last 30 days, with a 50% probability of it lasting more than 30 days (chart below). Second – previous shutdowns have seen federal workers furloughed rather than permanently laid off…but President Trump and other GOP leaders have indicated a desire to use the shutdown to shrink the size of the government workforce further. There have been some signs of willingness to negotiate a deal on healthcare by POTUS – his personal involvement is a positive sign – but no tangible progress yet. In my mind, the shutdown represents a more pervasive issue in US politics…a focus on short-term political point scoring – which inevitably leads to profligate spending – rather than strategic decision making to ensure long-term economic prosperity and debt sustainability. Both sides of the aisle have been guilty of focusing too much on the one-year-forward fiscal impulse, largely ignoring the fact that the US debt trajectory is on an unsustainable path. The OBBA is a near-dated pro-cyclical tax cut that will deliver a sugar rush late in the economic cycle…offset by a back-loaded fiscal tightening well into the next presidential term. On current form, can anyone reasonably expect the next Administration – Republican or Democrat – to not kick the can further down the road and push fiscal consolidation beyond even the subsequent election? The longer the fiscal issue festers unaddressed, the more severe the long-term consequences will be as the inevitable sizeable taxes increases and large spending cuts kill growth, animal spirits and the entrepreneurial essence that is the lifeblood of the US economy. At a time of dramatic change within societies, politicians across the democratic world are faced with the challenge of short-term political cycles against the need for long-term strategic decision making on a myriad range of topics including deregulation, technology, demographics, and fiscal sustainability. Strong leadership is essential to make decisions that will deliver meaningful progress that often outlasts the governments that implement them.

Source: Kalshi

AI IS REAL AND WILL BRING SUBSTANTIAL – POTENTIALLY EVEN INDUSTRIAL REVOLUTION LEVEL – CHANGE TO INDIVIDUALS, BUSINESSES, AND THE MACRO ECONOMY. This was one of the learnings from our flagship “Future of Global Markets” conference in NY this week, where we convened some of the world’s foremost thought leaders to opine on how innovation will alter the landscape of markets, business, and society. The long-term benefits from AI will come not only from the rising value of a few hyperscaler companies, but the diffusion of their innovations to a broad range of businesses and households, thereby delivering gains to productivity at the macro level and higher trend growth. This will ultimately define the fiscal space that indebted governments will have. I believe this diffusion will happen…but the timescale could be much longer than some expect. At current valuations, the AI sector will need to deliver trillions in value over coming years to justify the ongoing capex investments that have been made. At the same time, these companies see AI not simply as a source of revenue, but as a matter of survival – they must invest or risk going to zero in a world where innovation is moving at lightning speed and quantum computing ensures an even greater acceleration. And this is a crucial point – the “AI factories” that need to be built to drive this innovation will mean that the annual capex spend could rise from even the current staggering numbers of ~$400bn/year. But ultimately, like with any investment, it will have to deliver a significant return, and investors will punish companies that are unable to deliver. Some firms will fail, others will have dramatic success. This is how innovation happens…indeed we have seen this before in prior market run-ups, so market participants should take note – corrections can be quick, deep and without forewarning. Short-term shocks like Friday’s tariff news will have a greater impact on market pricing than earnings from AI that will deliver over a much longer horizon.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/