By Nohshad Shah

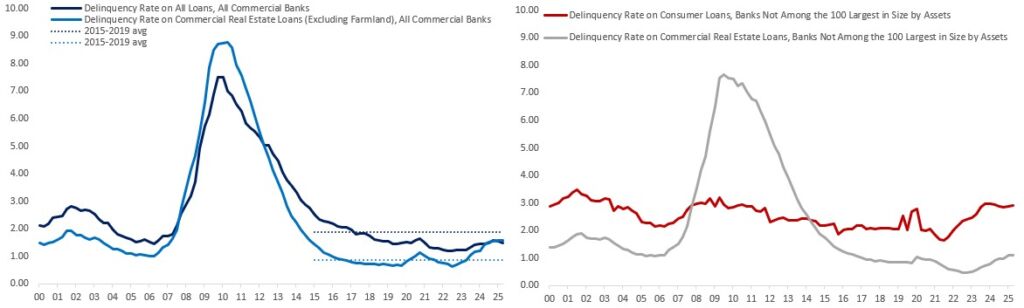

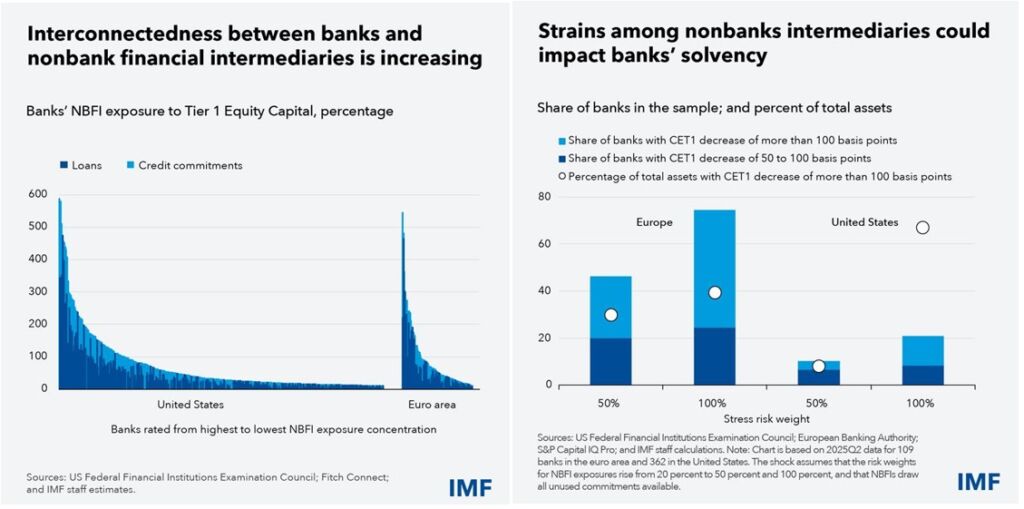

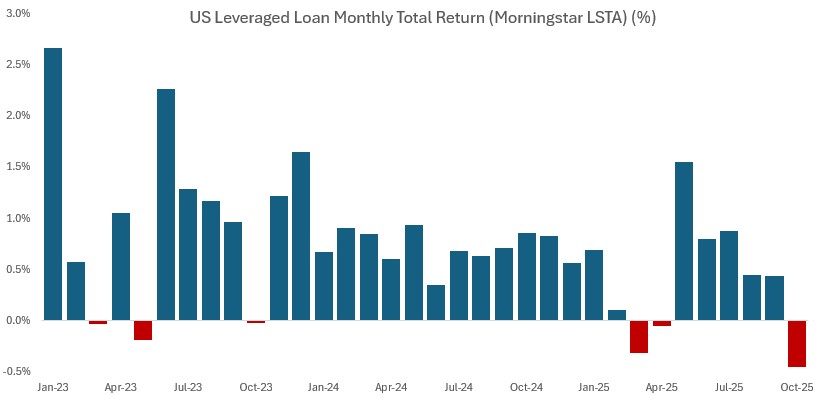

MARKETS REMAIN JITTERY…with this week’s news that two US regional banks (Zions and Western Alliance) disclosed loan losses and potential fraud by borrowers. Tensions were already high following the collapse of First Brands and Tricolor, the latter of which prompted JP Morgan to take a $170mio charge and CEO Jamie Dimon to warn of potential further “cockroaches” in the lending system. The KRE Regional Banks ETF moved sharply lower (-8%) and both HY and IG credit indices widened in response. The key question for investors is whether this is an early sign of systemic risks in markets or just part of a typical credit cycle. Whilst the environment for credit risks has been benign for a long time, there are some signs of concern. Looking at delinquency rates on all loans across all commercial banks, we see that losses are well within the 2015-19 pre-pandemic range. However, when we look at the same delinquency rates on commercial real estate (CRE) loans, they are substantially above 2015-19 levels and still rising (chart below). Though problems in the CRE space have been well telegraphed, it remains a source of concern for lenders should losses continue to proliferate as debt matures in the face of elevated interest rates and anaemic real estate demand. The other important factor is the lender…when observing default rates, it’s concerning to note that the rise in delinquencies amongst consumer and CRE loans has been most prevalent amongst smaller banks (outside the top 100 by assets – chart below). As this economic cycle has elongated, it doesn’t surprise me that smaller lenders have likely weakened their lending standards in the face of stiff competition. I am not worried about JP Morgan and their ‘fortress’ balance sheet…but we should keep an eye on the regional segment of the banking system for further losses. Of course, these days banks are only one piece of the puzzle…non-bank financial institutions (NBFIs) have significantly increased their lending share, especially leveraged loans, where they dominate with more than 80% of the market. CLOs have become increasingly popular with large institutional investors due to the breadth of the structures, thereby reducing concentration risk for investors. But as the First Brands experience shows (a large issuer for CLOs; $5bn of loans), the impact can be far and wide – losses will be felt not only by CLO equity holders, but also the managers of the structured products themselves. Morningstar LSTA data shows that the US leveraged loan market is set for its worst monthly loss in 3 years (chart below). Leveraged loan issuance has hit record levels this year due to insatiable demand for high-yielding assets from investors…and I would not be surprised if deals have been rushed through and lending standards diminished in such an environment. What concerns me is the opaque nature of this segment of the market…and the similarly opaque interconnectedness of it…some banks are large lenders to non-bank financial institutions. A recent IMF report highlights how vulnerabilities in non-bank intermediaries can quickly transmit to the core banking system, magnifying shocks…these firms (including private equity, insurance, pension funds and other investment vehicles) now hold approx. half of the world’s financial assets. In the US, many banks have non-bank exposures that exceed their Tier 1 capital…and the report finds that in a stress scenario in which NBFIs face greater risks and fully draw their credit lines from banks, the spillover effects can be significant – 10% of US banks (by assets) would see their regulatory capital fall by more than 100bps – displaying the lock-step nature of bank losses with capital declines in private markets (chart below). Does this mean we are facing systemic financial stability risks? At this moment, it doesn’t look like it – absent an escalation in losses and a sharp economic downturn this should be manageable…especially given most exposures are amongst smaller non-systemically important banks… and both Fed and Treasury have recent experience in managing macro-prudential risks (although the growth of private markets complicates crisis management). Though investors should be prudent.

Source: FRED, Citadel Securities

Source: Bloomberg, Citadel Securities

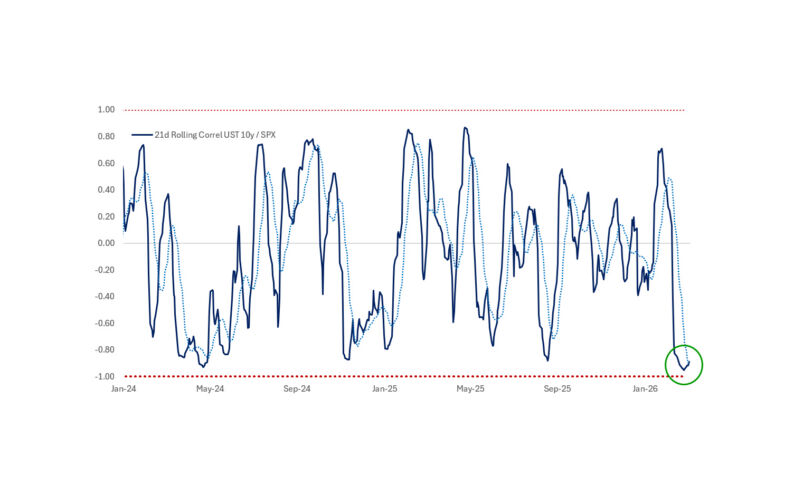

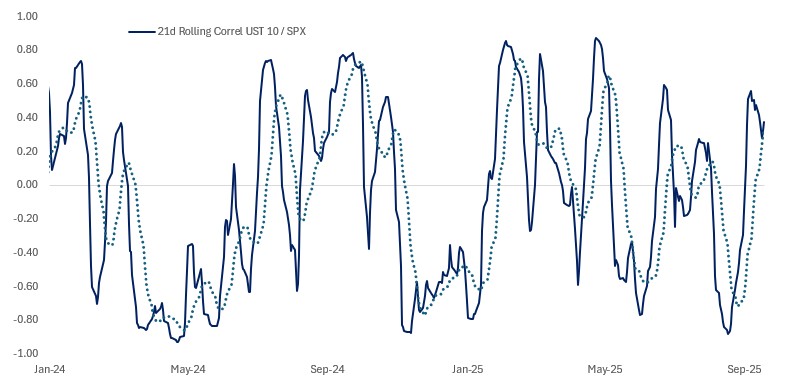

AS I’VE BEEN HIGHLIGHTING FOR THE LAST COUPLE OF WEEKS…stocks have travelled a long way towards pricing a more optimistic growth outcome (my view since early May)…and risks have felt much more balanced ahead of US-China tariffs escalation, the extended US government shutdown, and now, concerns over credit risks. The nervous price action in risk assets is more a function of valuations leaving little room for error than a prophecy of a more concerning turn in the macro narrative. For sure, the absence of economic data has not helped…creating something of a vacuum in which bad news has been amplified, without the reassuring signal of a steady stream of data supporting the “holding up” economic narrative. Equity-bond correlations have picked up rapidly (chart below), likely amplified by the lack of inflation data to interrupt the price action. Whilst it’s natural for bonds to rally in periods of risk asset weakness, it does highlight the additional vulnerability of fixed income valuations here relative to stocks…which could be challenged by both a better risk outlook and the inflation channel, which I continue to believe markets are far too relaxed about.

Source: Bloomberg, Citadel Securities

GIVEN THE ONGOING GOVERNMENT SHUTDOWN AND LACK OF OFFICIAL DATA, THE FED WILL HAVE TO RELY MORE HEAVILY ON IT’S FORECASTS…so the path of least resistance is to deliver two additional rate cuts this year – in line with the dots and market pricing. But…the path beyond that is less clear to me. Futures pricing shows three further rate cuts in 2026, which I think is a lot, absent a recession. Some of this premium is clearly a function of the market’s confidence that President Trump’s pick for Fed Chair will deliver dovish outcomes regardless of the outlook (even though 40bps of those cuts are still priced during Chair Powell’s tenure)…and the idea that extended labour market weakness will overwhelm the Fed’s second order mandate on inflation. I’m less confident than markets on both counts. In my mind, at least some of the weakness in the labour market is driven by structural forces (reduced net immigration; AI-driven hiring choices) rather than cyclical weakness. Indeed, as labour force supply is constrained by lower migration – reducing trend growth over the medium-term – the NAIRU is likely to be higher than previously estimated…implying that the labour market equilibrium consistent with non-accelerating inflation is directionally weaker than it has been in recent years…so the Fed may have less room to cut without creating inflation. In other words, the level of slack in employment may be less for a given level of the unemployment rate. This means inflation risks are greater should the economy heat up in coming months, as I expect. In sum, I remain optimistic on the 2026 forward growth outlook – relative to the pricing in rates – because of the potent mix of fiscal stimulus, monetary easing, loose financial conditions, and deregulation that should all kick into gear around the turn of the year to support the labour market. However, recent wobbles in macro markets are a salient reminder that the significant run-up in risk sentiment since April’s confidence shock has left valuations exposed to shocks. Valuations matter as much as the outlook.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/