-

Who We Are

- What We Do

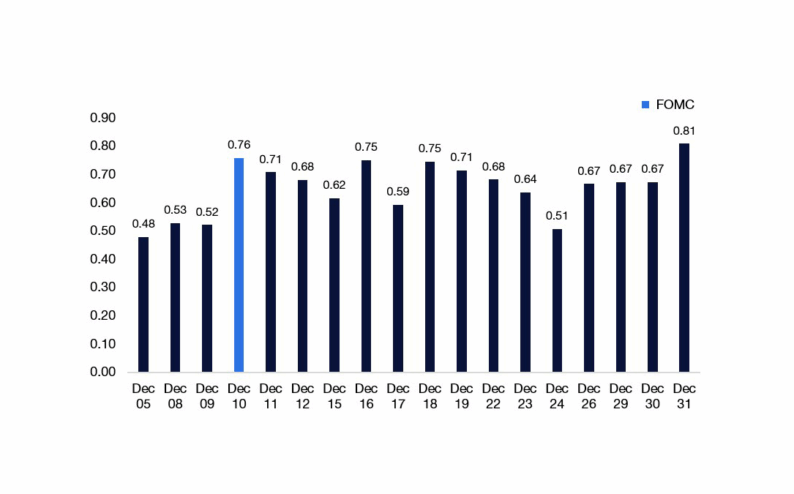

Series: Global Macro StrategyDoubling Down on Dec FOMC

By Frank Flight

Data sequencing and Fed speak make a cut hard to see.

- We continue to think Dec FOMC will be an on-hold rate decision

- Carefully mapping the sequence of economic data could hold edge regarding the Dec pricing and skews in a mildly hawkish direction

- Fed speak has been uniformly hawkish, we think the market is under indexing to the comments from Jefferson and Barr as a signal for the views of Chair Powell

- Our tracking of Fed “votes” suggest that there is a consensus to hold rates steady should the Sep Employment report come in line with expectations.

- We also think there is signal in the fact that the Fed is communicating ahead in this way AHEAD of the data deluge

84 of 105 surveyed economists expect a cut at the Dec meeting, here is why we disagree:

1) Data Release Sequence: Source of Edge for Dec FOMC Probability

We think there’s some edge in the data sequence:

- BLS will likely start by releasing the Sep Employment Report early next week, as it has been collected + analyzed.

- Reference week for the Oct employment report was 12th Oct (during shutdown) so BLS would need to collect the data asking respondents to retroactively identify hiring/employment from over a month prior. This potentially introduces material data quality concerns for the Oct and Nov reports. The household survey is most exposed to this.

- The White House had indicated that both Oct CPI and Employment reports will not be released but Kevin Hasset clarified that the Oct jobs figure would likely be released, with the U rate not released.

- The backlog of delayed data may also spill into the processing of the November employment report, which would be due to be collected next week. The key question here is if it is possible to collect and process the data on time given the backlog.

- Our base case is that it will be difficult to collect the November data on time if the Oct report is processed and released ahead of the Nov report, meaning the BLS may need to delay the report from the 5th Dec until after the Dec FOMC meeting (10th Dec). For reference – the FOMC blackout starts on the 29th Nov.

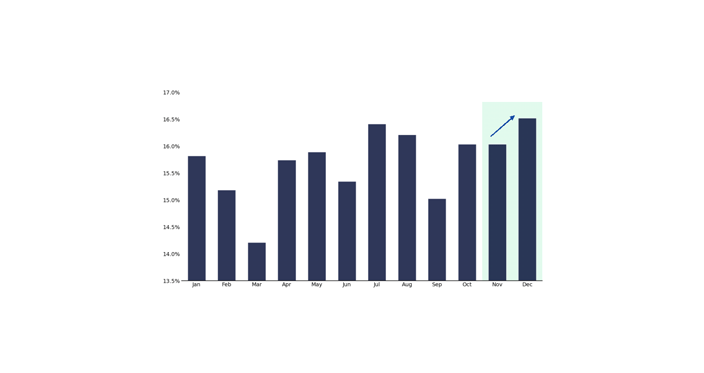

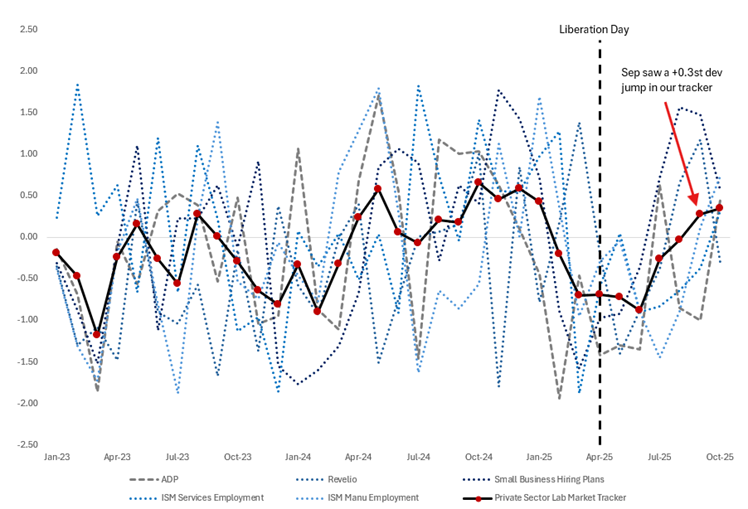

2) Sep Data Looks OK..Oct Data More Likely Delayed/Lower Quality

- Our tracking suggests the Sept Employment Report looks broadly solid (chart below).

- And we see risks that the Sep report beats consensus estimate (preview to follow).

- The October data was expected to be the weak spot in which the U-rate was expected to jump 0.3-0.5% due to the furloughing of gov workers.

- The shutdown driven U-rate rise will no longer show up given lack of Oct household survey.

- The Oct NFP report is likely to be weak but we think the expectation of a negative headline number is well flagged to the market and the Fed due to -125k DOGE layoffs being back dated from earlier in the year. Data quality concerns will be in focus also.

- The lack of an Oct CPI combined with benign initial claims as implied by aggregating the state level data means the data release sequence leans mildly hawkish in terms of its implications for the Dec meeting (less data = less likely to cut)

Source: Bloomberg, FOMC, Citadel Securities, Nov-25,

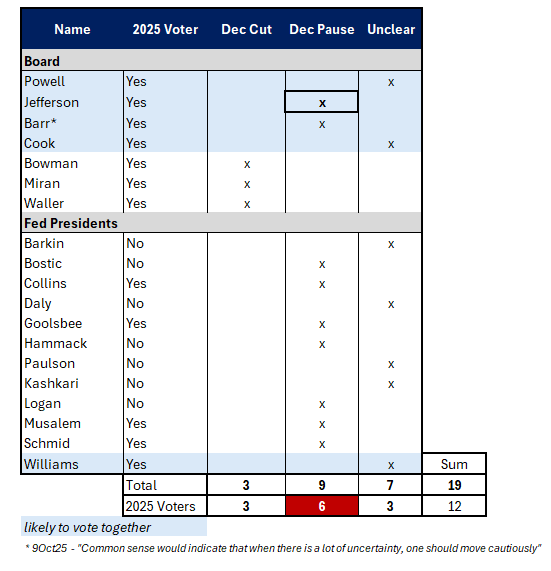

Figures are for illustrative purposes only. Past performance figures do not guarantee future results3) FOMC Vote Split Analysis

- Of the 12 voters: only 3 have stated they are likely to vote for a cut: Miran, Bowman, Waller

- Based on their public comments we think that the following 6 (/12) voters prefer to hold rates steady: Jefferson, Barr, Collins, Goolsbee, Musalem, Schmid.

- Based on their public comments we think 3x of the remaining non voters favor a hold: Bostic, Hammack, Logan.

- So far this suggests 6/12 voters prefer a hold and 9/19 FOMC members prefer a hold

- We think that Powell, Jefferson, Williams and Barr will vote together and therefore attribute a lot of weight to comments from Jefferson who last week said: “The current policy stance is still somewhat restrictive, but we have moved it closer to its neutral level that neither restricts nor stimulates the economy. Given this, it makes sense to proceed slowly as we approach the neutral rate.” and Barr who on 9 Oct said: “Common sense would indicate that when there is a lot of uncertainty, one should move cautiously.”

- We find it unlikely that Vice Chair Jefferson and Chair Powell are not aligned here, especially given it was Powell himself that injected uncertainty into the Dec meeting in the Oct presser and Jefferson followed that message up last week

- If the above is correct then this swings the committee to 8/12 voters for a hold and 11/19 of the FOMC in favour of holding rates steady, accounting for Powell and Williams

Source: Bloomberg, FOMC, Citadel Securities, Nov-25.

Figures are for illustrative purposes only. Past performance figures do not guarantee future resultsThe above table is Citadel Securities subjective assessment of how FOMC voters may lean at the December meeting

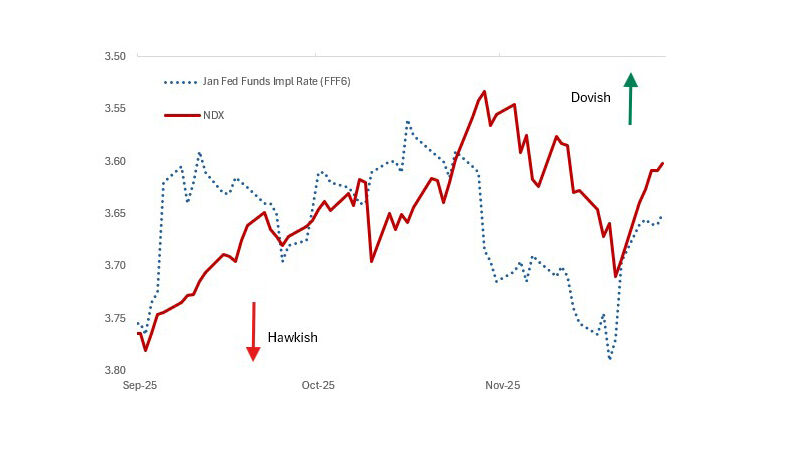

4) Timiraos WSJ Article

- WSJ Timiraos (“The Fed Is Increasingly Torn Over a December Rate Cut“) continues the theme of co-ordinated messaging from the Fed speakers.

- Timiraos piece emphasizes that: “Whether officials will cut rates again at their Dec. 9-10 meeting is a tossup.”

- There is no Fed speaker sourced for the “Toss up comment”

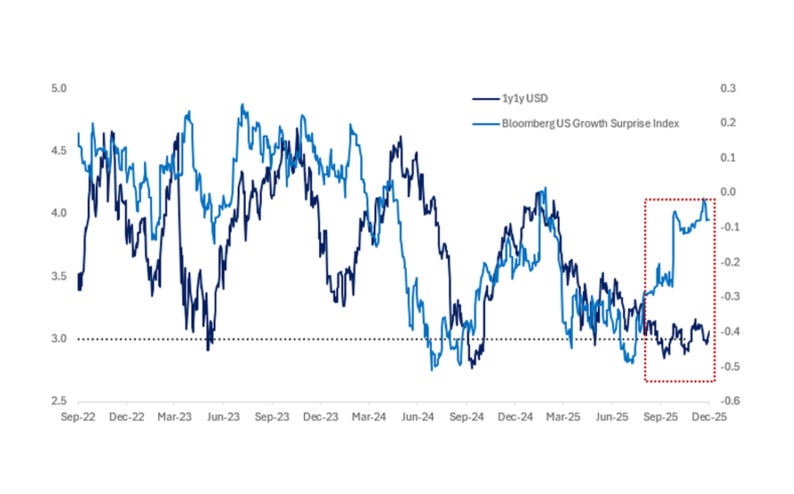

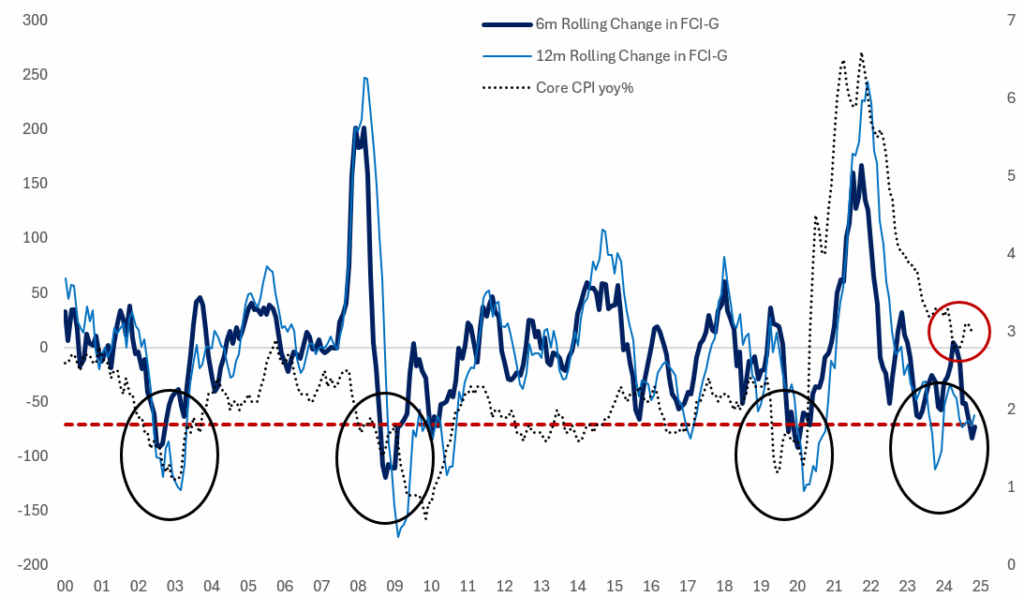

5) The Easing in Financial Conditions is Historically Large

- The six-month easing in the Fed’s own measure of financial conditions is historically large — comparable to post-recession recovery periods, representing a tailwind equivalent to 50–75 bps of one-year forward annualized growth.

- The easing in FCI coincides with the front loaded the fiscal impulse from the OBBBA, which is compounded by retroactive personal tax refunds from 2025 likely to be paid in H1 2026.

Source: Bloomberg, FOMC, Citadel Securities, Nov-25

Figures are for illustrative purposes only. Past performance figures do not guarantee future resultsLegal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Market Insights - What We Do