-

Who We Are

- What We Do

Series: Macro ThoughtsDeleveraging

By Nohshad Shah

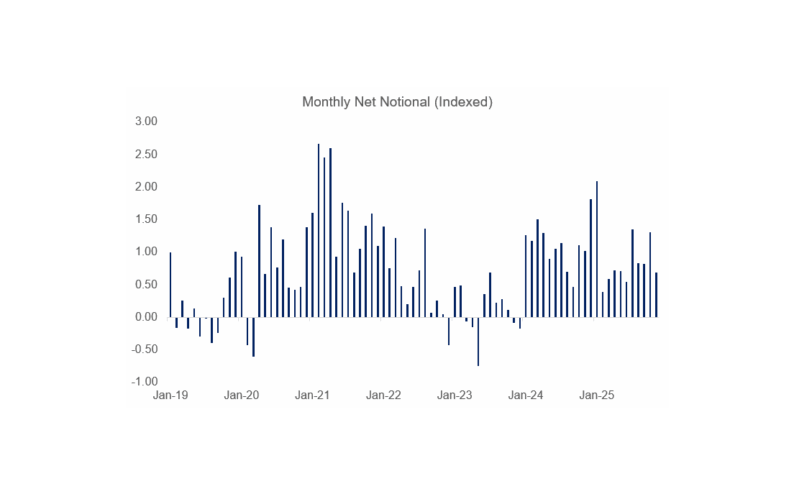

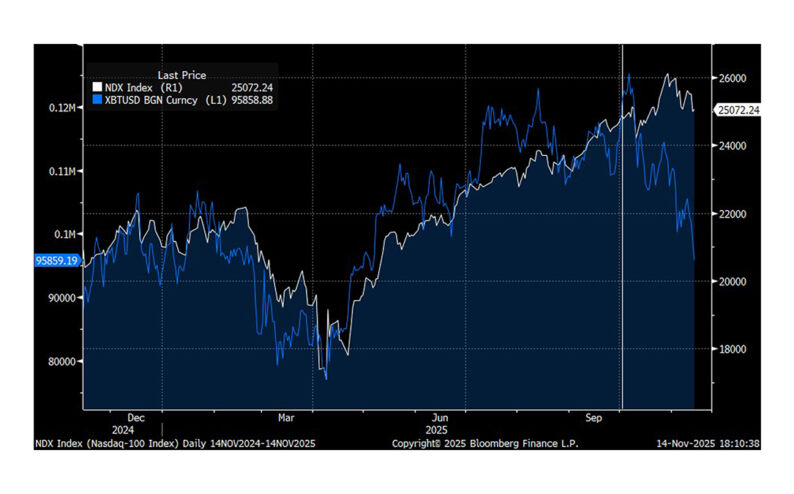

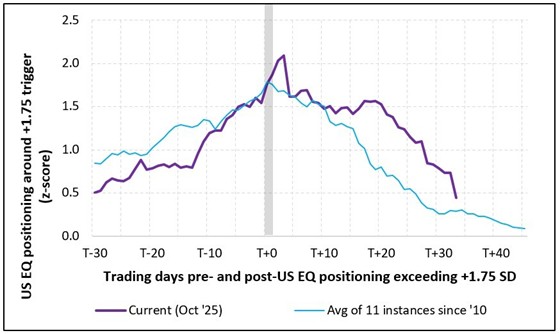

RISK ASSETS REMAINED UNDER PRESSURE THIS WEEK WITH NDX -8% FROM THE HIGHS AND INVESTORS SHEDDING RISK ACROSS EVERYTHING FROM TECH STOCKS TO BITCOIN. Whilst the sell-off has accelerated in recent days, concerns have been building since mid-October, when I highlighted in this note the emergence of downside risks. Some of this is a typical unwind of overextended positioning – most measures of aggregate positioning in US equities suggested heavy speculative longs (chart below)…and profit-taking towards the end of a year of solid stock market performance has come quickly. But there is more at play here and it’s instructive to understand the key factors driving this move. The mindset of investors towards AI-related capex has changed. The market has woken up to the magnitude of debt issuance required to fund this ongoing spend…estimated to be $600bn next year (up from ~$400bn in 2025)…and finds it objectionable. The boom felt better when it was funded out of earnings, but markets are jittery around the use of large and complicated debt deals. The return on investment remains highly uncertain…in a recent study, Bain & Co. estimated that $2tn in new revenue is required to profitably offset the infrastructure spend by 2030…much larger than the current revenues of the hyperscalers. As I’ve long said, these mega cap companies see this expenditure as existential, making them inelastic buyers of resources to achieve AI build goals and increasingly inelastic issuers of debt to fund it. Investors, however, are not inelastic…far from it…and they are becoming much more discerning on this matter, reflected in the price action in equity and credit markets (chart below).

US Equities Aggregate positioning

Source: Vanda Research

Oracle 5Y CDS; CDX IG 5Y

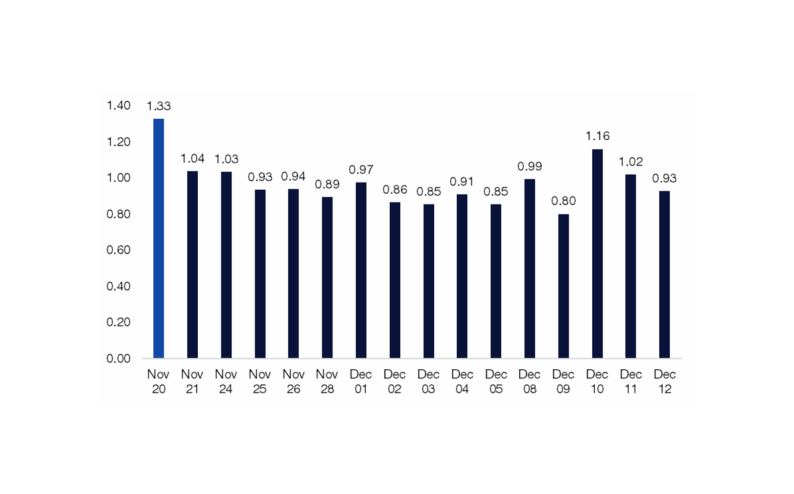

THE GENESIS OF THE RISK-OFF MOVE STARTED WITH THE CHANGE IN FED NARRATIVE…following last month’s FOMC meeting. Chair Powell’s presser introduced doubts around the glide path for their insurance rate cuts, moving the probability of a rate cut in December from 100% to a low of 40%. In my view, this was driven by the lack of clarity on the health of the US labour market in the absence of economic data during the government shutdown…a significant portion of the committee seems uncomfortable with continued cuts in the “foggy” environment, especially with inflation still ~1% above target. This signals a hawkish adjustment in the Fed’s reaction function without the related positive boost in the economic outlook – a problem for stocks. Incrementally, this week’s release of the September employment report did not provide much clarity…it wasn’t weak enough to push the Fed into a December rate cut but not strong enough to allay fears around the labour market. The +119k NFP print was robust but accompanied by a downward revision of -33k to the prior two months. This leaves the 3m average pace at 62k, essentially around most estimates of the breakeven rate…which is consistent with my view that the labour market is cooling but not collapsing. Whilst some forward-looking labour market indicators have been better (NFIB small business hiring; ISM employment subcomponents), the rise in the u/e rate to 4.44% was meaningful, though largely driven by a 470k increase in participation, particularly among the younger cohorts of the household survey (generally the most benign way that the u/e rate can rise, but a rise nonetheless). The increase in permanent (rather than temporary) layoffs was also concerning (although voluntary job leavers increased too). Like the data, commentary from FOMC members remained inconclusive with hawkish comments from voting members like Goolsbee who’s “uneasy front loading too many rate cuts”. These sentiments were echoed by Collins and Jefferson but stand in sharp contrast to NY Fed President John Williams (importantly, a confidant to Powell) who on Friday flipped the script and pricing (to 75% for a Dec cut) by saying “I still see room for a further adjustment in the near term to the target range for the federal funds rate to move the stance of policy closer to the range of neutral”. This further contrasts with the tone from another Powell ally William Barr, less than 24hrs before, who suggested “we need to be careful and cautious now about monetary policy, because we want to make sure that we’re achieving both sides of our mandate”. Both speakers came after the employment report and it’s clear that whichever way the decision for December breaks, a significant number of the committee will be unhappy. There have been five meetings since 2011 which saw three members dissent…and one needs to go back to 1992 under Alan Grenspan to find a meeting that had four dissents from the decision. It seems we are entering a new regime, and policymakers are struggling as much as market participants to decipher the outlook.

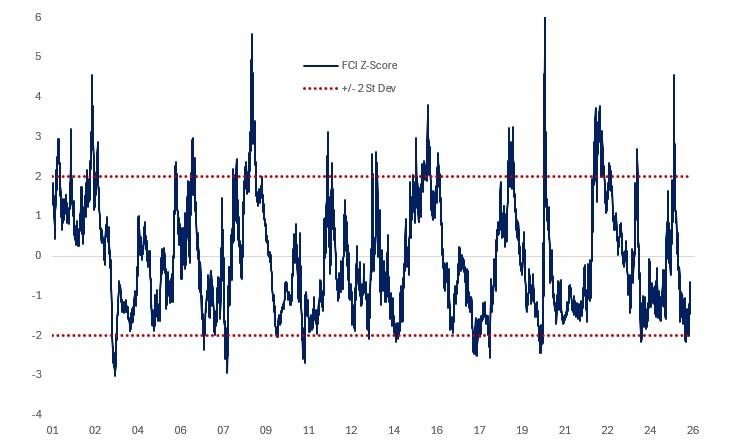

US Financial Conditions Index Z-Score

Source: Bloomberg, Citadel Securities

ALL OF THIS IS UNSETTLING FOR RISK ASSETS…which have become accustomed to loose financial conditions buttressed by easy monetary and fiscal policy. FCI has been easing consistently since April – to the tune of 100bps – reaching multi-year lows last month. As I’ve suggested before, this was not a stable equilibrium and tightening was overdue – either from the rates channel or equities. Indeed, if we look at the long-term history of the Z-score of FCI (chart above), we see that at +/-2sd it tends to signal a turning point…and this is exactly what we’ve seen over recent weeks with a tightening of ~40bps in FCI, driven by a combination of the policy factor (rates) and risk assets (equities lower, credit wider). Another important factor in the sell-off is liquidity…which has been drained in recent weeks due to a confluence of factors that are yet to be fully resolved. The Treasury General Account (TGA) build from $300bn to ~$1tn in October definitionally depletes reserves…and the build was particularly rapid recently due to the shutdown…meaning that outflows – which create private sector reserves – were curtailed, whilst bills issuance – which drains private sector reserves – was high. The relationship between liquidity and risk assets is complex and certainly non-linear, but there was some hope that once the government shutdown ended and as the end of QT approached, liquidity would improve, and funding stress would relax. However, the TGA has started to decline but still sits at $900bn, some $50bn above its target level and bills issuance remains seasonally elevated until the end of November. If liquidity remains relatively scarce and we are yet to normalise to the “ample” threshold (hard to measure in real time) then this remains a constraint on risk sentiment and market-based liquidity proxies.

Treasury General Account Balance

Source: Bloomberg, Citadel Securities

THE PATH FORWARD FOR ASSET PRICES REMAINS COMPLICATED. The current bout of deleveraging needs to run its course…though based on positioning metrics and FCI, we should be in a healthier place now. However, risk assets will remain levered to what the Fed will do – not only in December’s meeting – but into 2026. We still have ~75bps of rate cuts embedded into market pricing…should those need to come out, it will no doubt be painful for equities. We need clarity from the Fed, either way.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Market Insights - What We Do