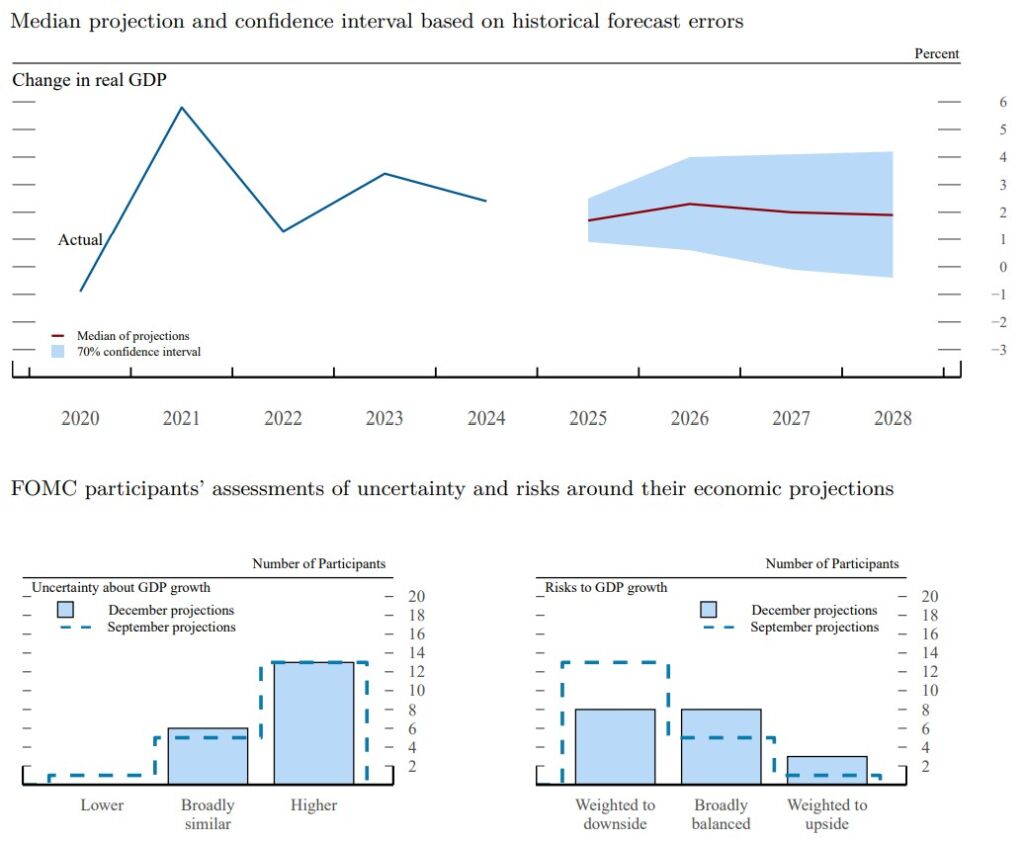

THE FOMC DELIVERED ON MY EXPECTATIONS OF A HAWKISH CUT…with the inclusion of “extent and timing” language in the statement to “additional adjustments to the target range for the federal funds rate”. The dots in the Summary of Economic Projections (SEP) also leaned hawkish, indicating only one additional cut. While this is technically unchanged – since the 2026 dots roll into the front year – the divergence from market pricing makes it meaningful. They also upgraded their growth forecast for 2026 from 1.8% to 2.3% – more in line with my expectations – though interestingly, they see a lower trajectory for core PCE at 2.5% from 2.6%…and an unchanged unemployment rate at 4.4%. This intriguing set of forecasts imply that the FOMC does not see slack in the US economy tightening in the context of 2.3% real GDP growth, despite it being ~55bps above what is likely current trend growth. Chair Powell implied this was a function of better productivity growth, but I find that hard to square with the reality of the immigration trajectory, which incorporating lags in labour supply, will be constrained for the foreseeable future. Negative net migration (for the first time in decades) will have a significant effect on trend growth (other things being equal) via the population channel (trend growth = labour force growth x hours worked x productivity). Now, it’s possible that this could be overwhelmed by an increase in AI-driven productivity in 2026…but in my mind, this will take much longer to play out than the popular narrative suggests…indeed history tells us that it takes time for technological change to show up in productivity statistics. Accordingly, I see more downside risk to trend growth than upside, meaning that the Fed may well be surprised at the inflation-generating capacity of the US economy next year in the backdrop of a growth prediction which already sits above even the long-run estimate of trend ~1.9-2.0%. Moreover, expectations for growth itself look slightly too low – given the combined policy impulse from FCI and OBBA is likely >1% GDP in 2026. I tend to think about policy impulses relative to trend…so if the FOMC agree we have 100bps of stimulus in 2026, then their 2.3% growth estimate would imply a 1.3% trend estimate, which seems inconsistent with their inflation and unemployment rate forecasts. What’s more likely is that they see a far smaller impulse, or they’re assuming some residual tariff / uncertainty drag. I think financial markets are telling us that’s wrong…for example looking at equity cyclicals vs defensives, which is at YTD highs. Hence, I see a relatively low bar to outperform the Fed’s growth forecast. In terms of the dots, six participants registered a soft dissent in the form of unchanged dots for 2025 and three wrote down a rate hike for 2026; four participants see unchanged rates, four see one further cut, four see two cuts and three see a materially lower policy path. All of this speaks to the challenge I highlighted last week that the next Fed chair will face an uphill battle cutting rates in a landscape that sees economic growth improving and inflation remaining above target (and potentially rising).

Source: Federal Reserve

LOOKING BACK AT THIS YEAR, MARKETS AND THE ECONOMY WERE VIOLENTLY JOLTED BY APRIL’S ‘TARIFF TANTRUM’…leading to heightened uncertainty for corporates and a stock market correction. As I explained at the time, once it became clear that President Trump’s policies would be more measured than originally advertised, the underlying fundamentals of the economy remained sound and easy financial conditions would provide a rich backdrop for equity market gains…especially in the context of a once-in-a-generation AI capex boom driven by hyperscalers divinely committed to winning the arms race for generative AI and beyond. This proved to be correct, with a trough-to-peak rally of 53% in NDX…the likes of which we haven’t seen since the COVID pandemic. The more underappreciated policy shift from this Administration was immigration – in a dramatic change to the Biden-era surge in net migration to over +2 million annually, President Trump’s restrictions have taken that number into negative territory, a trend I fully expect to continue. The implications for the labour market, growth and inflation will be profound…but are largely yet to be felt. This is what has made the job of policymakers so difficult in recent months…with a government shutdown muddying the waters through a lack of reliable economic data. As we look forward to next year, the outlook is less conducive to FCI easing. With regards to the Fed Chair and policy, last week I made the following argument: “this is less about dismissing the possibility of rate cuts in a weakening macroeconomic outlook and more about highlighting that it will not be trivial for the new Fed Chair to simply adopt a dovish stance in the face of an improving growth, labour market and elevated inflationary landscape”. Interestingly, leading contender Kevin Hassett started to sound somewhat more balanced on policy this week, acknowledging that “You just do the right thing…Suppose that inflation has gotten from, say, 2.5% to 4%. You can’t cut”. Though it seems Kevin Warsh’s stock is rising. It’s also my view that the primary issue for next year’s midterm elections will be ‘affordability’…something which the politically astute POTUS has realised is a concern for voters. If the reality for ordinary Americans at the grocery store does not change for the better, I fear there may well be a political earthquake in Capitol Hill. Pushing for easier monetary policy at the risk of stoking inflation further will be a risky endeavour…even for President Trump. So ultimately, the new Fed Chair will likely still see some scope for policy rates to adjust down further to neutral…but should the labour market picture improve, it’s unclear he will have the votes to cut rates much more…and if my view of the cyclical outlook prevails, then the policy impulse is unlikely to continue to be a tailwind for risk assets next year – a big shift from the 175bps of rate cuts in the last two years.

Source: Bloomberg, Citadel Securities

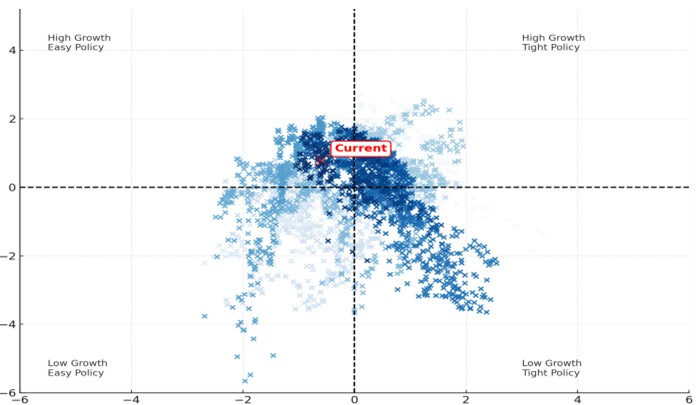

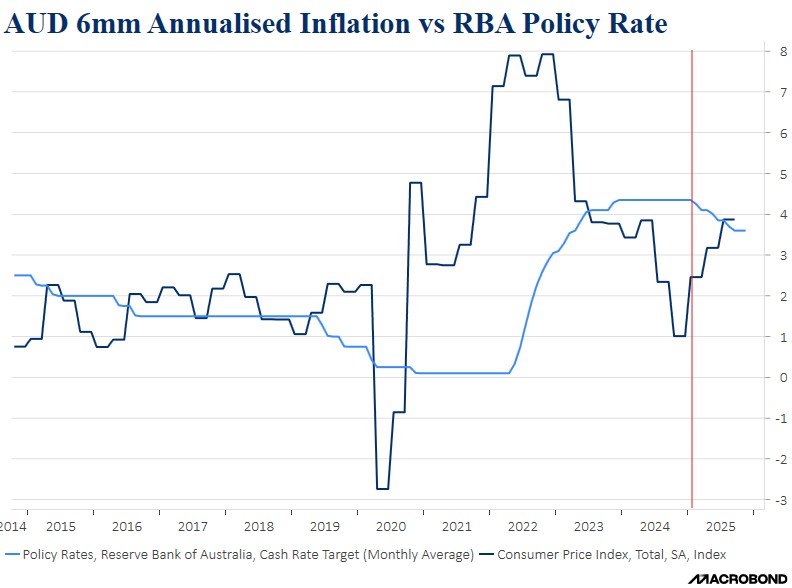

THE PRICE ACTION IN GLOBAL FIXED INCOME OUTSIDE THE US IS TELLING. We have seen a meaningful sell off in front end rates across Europe, Canada, Sweden, and most notably in Australia, as central banks have concluded cutting cycles and markets are now starting to price hikes in some regions. The RBA’s experience is a warning shot across the bow to central banks (most clearly the Fed) to not extend policy rate cuts too much in the face of high fiscal deficits, elevated neutral rates and before inflation has durably returned to target. Since the RBA cut rates 75bps from 4.35% to 3.60%, inflation has accelerated meaningfully and is likely to print between 0.9-1.1% QoQ (trimmed mean) in Q4, which annualizes to 3.6%-4.4%, a substantive acceleration…at a time when the unemployment rate (which had risen gradually following the hiking cycle) is declining…loan growth is accelerating…and household spending is picking up alongside house prices. As a result, Australian interest rate forwards now price nearly two hikes by the end of 2026. If the market decides rates hikes are appropriate for the US economy late next year, and a captive Fed is unable to deliver them, then the risk is that long-end yields will do the work for the Fed in delivering the required financial conditions tightening. My colleague Frank Flight’s framework for macro regime classification (decomposing FCI into growth and policy factors) shows we are currently priced for a high-growth / easy-policy regime (chart above). This is the best environment for stocks…and the 2026 growth outlook can absolutely support these valuations…but I see the policy lever as less likely to continue to deliver a tailwind next year. A transition from high-growth / easy-policy to high-growth / tight-policy (via FCI, not policy rates) could be challenging for markets. The tails are getting fatter.

Thank you for the readership and support this year – this will be my last note of 2025. It’s been a remarkable year for markets and Citadel Securities. Thanks to your partnership we have made considerable strides broadening and deepening our client franchise. Together we can shape the future of markets – we are here for the challenge. As always, I am a taker of any and all feedback – please don’t hesitate to reach out.

Best wishes for the holidays, NS.

Source: Macrobond

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/