-

Who We Are

- What We Do

Series: Some Macro ThoughtsRisks…But Not On the Cyclical Outlook

By Nohshad Shah

MARKETS ARE JITTERY…AND FOR GOOD REASON. The combination of rising US–Iran conflict risk, ongoing pressure on software stocks from AI disruption, and early stress signals in credit is an uncomfortable mix. Diplomacy has stalled, and with it the probability of kinetic conflict in the Middle East has risen materially. The US has now assembled its largest regional air power presence since the 2003 Iraq invasion: multiple destroyers, advanced F-35 and F-22 jets, an aircraft carrier strike group – and notably, the USS Gerald Ford, the most advanced carrier in the US fleet, reportedly en route. This is unlikely to be symbolic positioning…sustaining such a deployment costs billions, which makes it difficult to interpret it as a bluff. In my view, the timeline is being set by military logistics, not presidential statements…we learned last year that publicly stated deadlines can be truncated abruptly. Accordingly, the relevant signal is force accumulation…once assets are in place, the optionality narrows. Washington argues Iran failed to recognise several “red lines”. Tehran’s calculus seems different…after last year’s strikes during negotiations, trust is effectively zero. From the regime’s perspective, conceding to US demands – full disarmament – risks certain internal collapse. Instead, they are placing an alternative bet…that regime change is extremely difficult without boots on the ground…and that US air strikes may even consolidate domestic support and improve legitimacy for the leadership; survival itself constitutes victory. It is a dangerous wager…especially given US military supremacy…but high-stakes actors often take asymmetric risks when survival is in question. The IRGC appears to believe it can withstand strikes and suppress internal unrest. For markets, the central risk is energy infrastructure…roughly 20% of global oil consumption transits the Strait of Hormuz. Even a temporary disruption would have an outsized impact on crude prices that already embed a modest geopolitical premium. Kharg Island – the terminal for over 90% of Iran’s crude exports, much of which goes to China – remains a strategic choke point and escalation lever, particularly if Gulf oil infrastructure is a target of Iranian retaliation. Whilst this remains a risk-scenario, rather than the central case (retaliatory strikes against US bases), investors should be alert to the possibility that in conflicts where both sides are testing resolve, timelines compress, miscalculation risk rises, and market pricing can adjust far faster than most expect. This risk is important in the context of a global oil market which remains tight despite a headline surplus – largely fictional from a pricing perspective. A substantial amount of sanctioned crude (Iran, Russia, Venezuela) is moving through shadow channels, with tens of millions of barrels sitting in floating storage…barrels that don’t clear into OECD hubs that actually set Brent. In other words, the market isn’t mispricing a glut; it’s correctly pricing tight, deliverable supply plus geopolitical fragility.

Source: Bloomberg, Citadel Securities

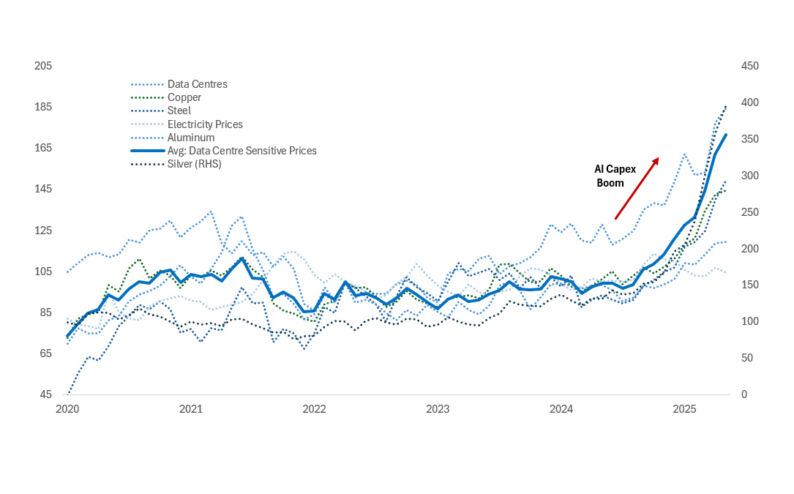

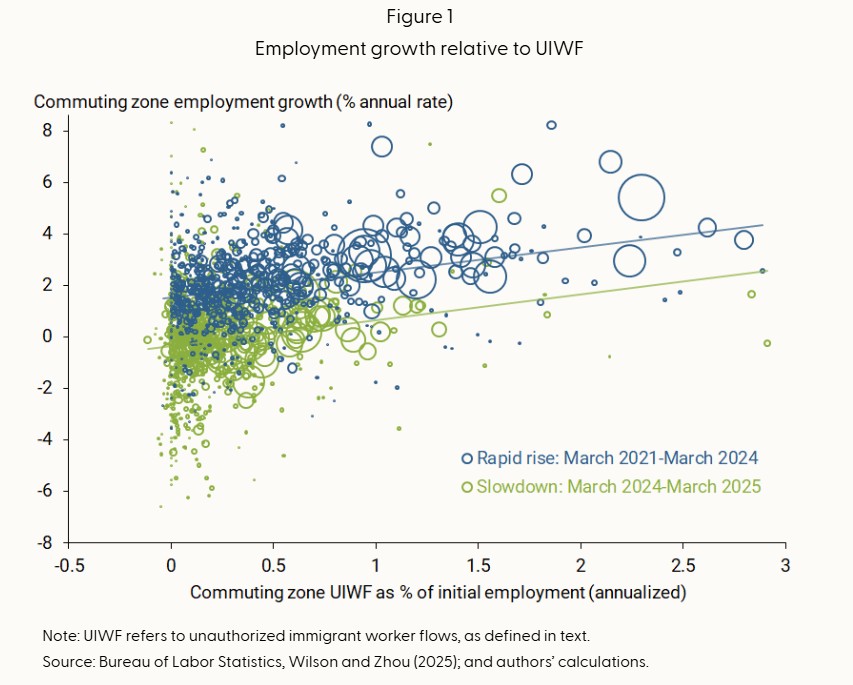

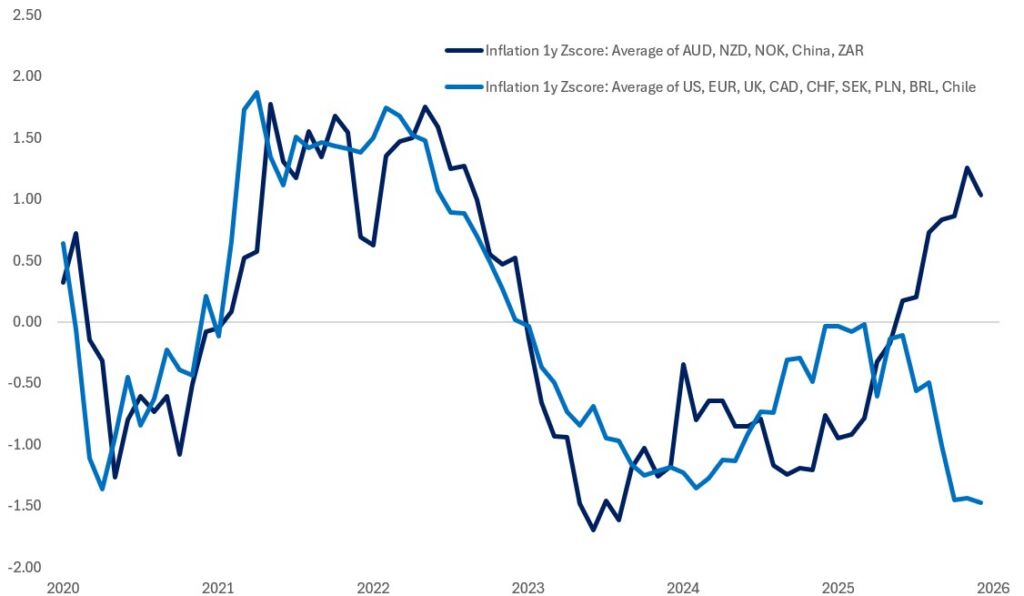

DESPITE THE MARKET’S FOCUS ON AI-DRIVEN DISINFLATION AND LABOUR DISINTERMEDIATION, THE INCOMING DATA CONTINUE TO REINFORCE MY CORE VIEW: WE ARE IN A CYCLICAL RE-ACCELERATION THAT SUPPORTS THE LABOUR MARKET AND SKEWS INFLATION RISKS TO THE UPSIDE. Friday’s US Supreme Court ruling against President Trump’s IEEPA tariffs was not a significant surprise for markets, but still a positive tailwind. In reaction, POTUS said he would impose a 10% global tariff and pursue section 122 of the Trade Act of 1974, an untested legal provision under which the President can impose up to 15% tariffs with a 150-day limit. He also mentioned section 301 and 232, which have previously been used for certain sectors. It remains uncertain whether refunds will now need to be processed in coming months – something lower courts will opine on. On net, this should be seen as a continued reduction of 2025’s trade-related uncertainty for the US economy…and in fact, may add further stimulus in 2026, a boost for corporate profits. With respect to economic data, Initial Jobless claims falling back to 206k adds to the signal from January’s jobs report that the labour market has stabilised. The high-frequency evidence is even clearer…the San Francisco Fed’s weekly labour market stress indicator – which tracks how many states are seeing claims-based unemployment accelerate – now sits at 3.0…the lowest level since Jan’23. That is not a labour market rolling over. If anything, conditions may be tightening…the decline in the unemployment rate through December and January was welcome, but U3 now sits at 4.28%. A move toward or below 4% would materially raise upside inflation risk. At the same time, the AI capex boom is not purely disinflationary, but carries near-term price pressures. As Frank Flight highlighted, the data centre buildout is pushing commodity inflation higher (our AI-linked commodity basket is up 65% since Jan ’24), while construction hiring is colliding with supply constraints in a sector where roughly 30% of the workforce is foreign-born. That is fertile ground for wage pressure. Recent San Francisco Fed research strengthens a point I have been making since last summer: immigration flows have been the key adjustment in the US labour market. Using newly constructed data on unauthorised worker inflows matched to local employment outcomes, the authors find an almost one-for-one relationship between immigration flows and job growth – both during the surge and the slowdown. If labour supply has been doing most of the work, then a deceleration in immigration implies a smaller effective labour force than headline data suggest. The policy implication is straightforward…if the labour market is tighter than conventional metrics imply, slack is lower, and wage risks are greater. The Fed has already delivered 175bps of cuts to cushion perceived labour weakness. If that weakness was largely a supply dynamic rather than demand deterioration, the forward reaction function is likely to prove materially less dovish than markets currently assume.

WHAT DOES THIS MEAN FOR MARKETS? There are two competing forces. First, the market continues to underprice the strength of the US growth backdrop. The cyclical impulse is firmer than consensus assumes. That is supportive for equities and credit, and clearly negative for duration…bonds are misaligned with the growth data. The counterpoint is policy…the case for delivering the full slate of rate cuts currently priced is thinning by the day. If inflation risks reassert – and tighter labour dynamics suggest they might later this year – that may become the equity market’s Achilles heel. Strong growth is supportive; a less dovish Fed is not. Taken together, this creates room for repricing…equities can move higher on cyclical momentum, but yields can rise alongside them. Credit, however, looks stretched…valuations are exceptionally tight and offer little compensation for policy or inflation risk. In sum, positioning for this environment argues for long growth via equities, short duration to capture tighter financial conditions, and selectively short credit where spreads fail to reflect appropriate risk.

Source: Bloomberg, Citadel Securities

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Market Insights - What We Do