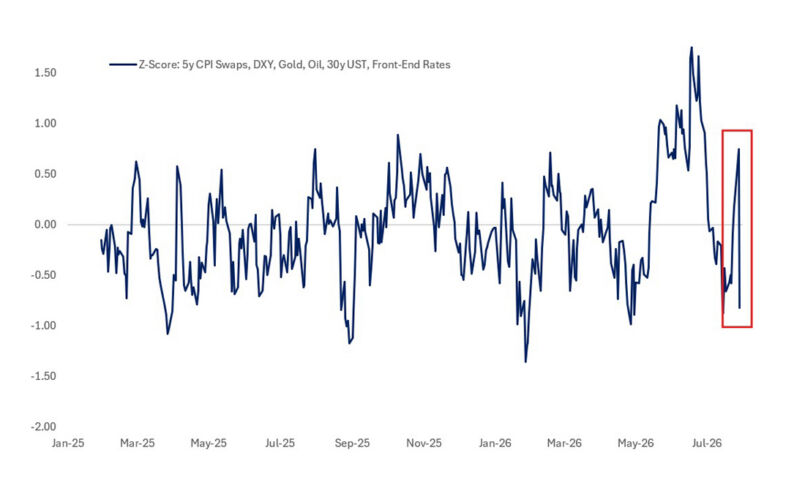

MUCH DIGITAL INK HAS BEEN SPILLED ON AI DISINTERMEDIATION AND THE RISKS TO SOFTWARE COMPANIES AND THE LABOUR MARKET. Frank Flight’s take on this is a must-read. I’ve long held the view that artificial intelligence will be a net positive for society and the economy…but like every transformational technology, it brings transition risk and uneven outcomes. There will be winners and losers. Ultimately, I see AI as a growth magnifier – at the corporate level and for countries that adopt it early and aggressively. That’s why I find the “SaaSpocalypse” narrative overblown. As Sequoia’s Konstantine Buhler argues, lower barriers to building software don’t destroy value, they expand the market and concentrate it. We’ve seen this movie before…the internet consolidated into a handful of trillion-dollar giants. The SaaS transition didn’t kill legacy leaders like Oracle…it made the market bigger. If anything, AI accelerates the same dynamic: a much larger enterprise software market, increasingly controlled by a small number of scaled, founder-led platforms. The real bet isn’t on SaaS collapsing, it’s on identifying which incumbents consolidate and which new AI entrants break through. The underappreciated risk to AI isn’t competition or model commoditisation – it’s energy. Data centres already consume roughly 460 TWh of electricity globally, and the IEA expects that figure to move toward 1,000+ TWh in the coming years (more than the annual consumption of a large, industrialised country like Japan) largely driven by AI workloads. In the US, over 2,300–2,600 GW of generation and storage projects sit in interconnection queues – more than double current installed capacity, highlighting severe transmission bottlenecks. Meanwhile, China has added roughly 1,500 GW of capacity in recent years and plans to add hundreds more annually (400 GW in 2026 alone), dwarfing US additions (86 GW). Execution risk is already visible…Sightline Climate, which tracks 190 GW across 777 large data centres announced since 2024, notes that of the 16 GW slated for 2026 across ~140 projects, only about 5 GW is under construction. The remaining 11 GW is still in the “announced” stage, despite typical build timelines of 12–18 months. Their estimate: 30–50% of planned 2026 capacity could be delayed. That’s a problem. Compute scales with power. Full stop. If generation and transmission don’t keep pace, electrons – not algorithms – become the binding constraint on AI growth. Jensen Huang, Sam Altman and others have flagged this repeatedly…yet it remains unclear whether the US government will meaningfully accelerate grid expansion with recent political rhetoric suggesting tech companies may largely be on their own. There are broader macro implications from all this. Surging AI-driven electricity demand is tightening energy markets at the margin…visible in natural gas dynamics and power pricing…hardly helpful amidst the current geopolitical instability in the Middle East. At the same time, memory constraints tied to AI infrastructure are reportedly weighing on other hardware markets, with analysts pointing to double-digit declines in smartphone shipments and rising device prices. Which brings me back to one of my core themes: inflation. I struggle to identify a major structural force in this cycle – technological, fiscal, or geopolitical – that doesn’t exert upward pressure on prices in the near term.

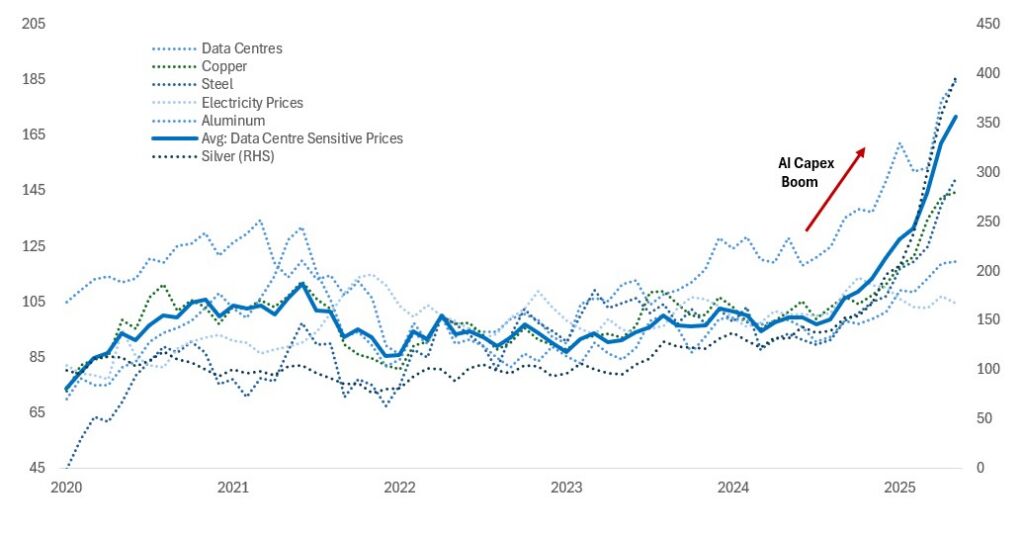

Index of prices for AI related commodities

Source: Bloomberg, Citadel Securities

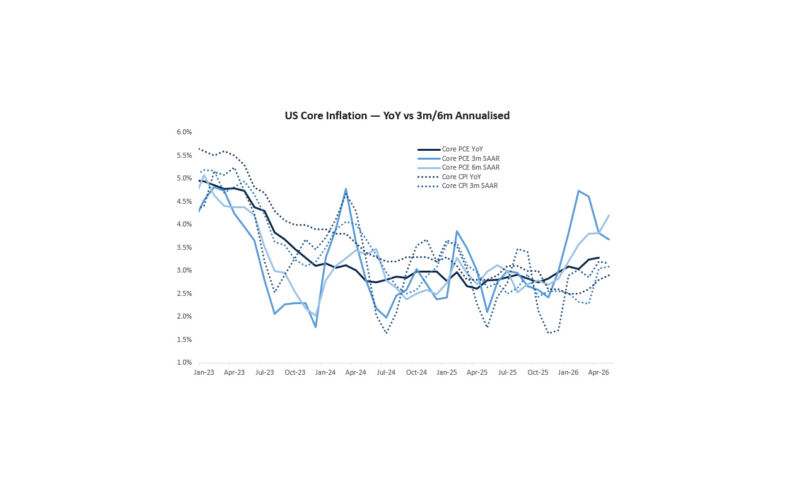

REGULAR READERS WILL KNOW MY CORE US MACRO THESIS: TIGHTER IMMIGRATION SLOWS TREND GROWTH INTO 2026, WHILE FISCAL STIMULUS, MASSIVE AI CAPEX AND EASY FINANCIAL CONDITIONS PUSH ACTUAL GROWTH ABOVE THE ECONOMY’S SPEED LIMIT…A RECIPE FOR RENEWED INFLATION PRESSURE. The monetary policy debate shouldn’t just focus on the dual mandate in a static sense; it needs to grapple with r*, the real neutral rate. If immigration slows population and labour force growth, that should, all else equal, push r* lower. Weaker trend growth reduces the marginal product of capital and softens investment demand relative to savings…the textbook dovish offset. But all else is not equal. AI capex – roughly $650bn this year and potentially ~$2tn over three years – materially alters the equilibrium. A surge in investment demand shifts the demand for funds outward, which in plain English means the price of money needs to be higher to clear the market. That pushes r* up. Markets are notoriously poor at pricing neutral in real time, so we look to the Fed’s own models…Williams’ HLW estimate sits around 1.1%, Lubik-Matthes closer to 2.1%. Averaging across broader models gets you roughly 1.4% for real neutral. Add a 2% inflation target and you get a nominal neutral around 3.4%…superficially close to today’s effective fed funds rate of 3.64%. But core PCE has been running closer to 2.75–3% since late 2023, and the FOMC’s own 2026 median forecast is 2.5%. Using 2.5% leaves nominal neutral closer to 3.9%. On that basis, policy is already below neutral. Yet OIS market pricing implies the policy rate at 3.075% by end-2026 – roughly 80bps below. With growth re-accelerating and inflation progress stalling…not to mention upside risks from AI-driven commodity and energy demand…the only way to justify that easing path is the Kevin Warsh productivity narrative: that AI will be so disinflationary that the Fed can cut as inflation falls faster than expected. I’m sceptical that those productivity gains show up cleanly in the near term, especially alongside the inflationary impulse from the capex build-out itself. And even if AI does boost productivity meaningfully, economic theory cuts against the dovish conclusion…stronger productivity raises expected returns on capital and lifts trend growth, which tends to push r* higher, not lower. A productivity boom doesn’t mechanically justify easier policy; it can simply imply a higher neutral rate. If that’s right, current forward rates pricing may be underestimating the risk that r* is drifting up – with distinctly hawkish implications.

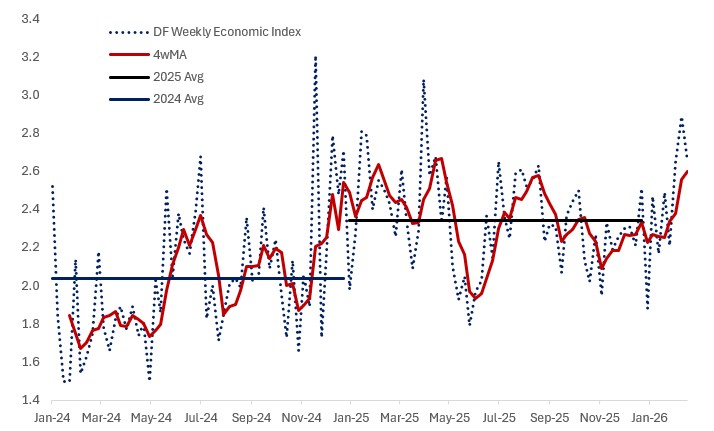

Dallas Fed Weekly Economic Index

Source: Dallas Fed

THE FUNDAMENTAL OUTLOOK CONTINUES TO EVOLVE BROADLY IN LINE WITH MY EXPECTATIONS. However, equity markets – particularly software – remain unable to shake the weakness. I’ve said repeatedly that credit is the most convex hedge to the AI disruption theme. Tech firms are deploying hundreds of billions annually into infrastructure spend…and yet IG spreads at ~80–85bps (LUACOAS) offer little compensation for risks in a world of rising uncertainty. Jeff Eason, our Head Credit Analyst, notes that a basket of topical software equities have seen roughly 35% forward P/E compression over the past 12 months. Credit in these names, by contrast, has widened only 25–50bps in absolute, a modest reaction relative to the equity reset. Beyond reassessment of business profiles and terminal value, investors will need to assess risks of companies utilising credit to support equity via M&A or buybacks at lower equity valuations. At the same time, stories of asset liquidations in private credit, occurring as the aforementioned equity multiple contraction impacts HY asset coverage, are a reminder of the structural fragility embedded in parts of this market. Funds are lending long against less liquid assets, as correlations in AI disrupted sectors increase, while offering liquidity to investors conditioned to daily dealing. When conditions tighten, that mismatch can become reflexive. I’ve long been wary of structures where the liquidity promised exceeds the liquidity of the underlying assets – that dynamic rarely ends well. The benign macro backdrop may well save the day…but pairing long equity exposure with credit shorts makes sense precisely for the reasons we’re seeing play out this week. In sum, credit concerns, AI disintermediation fears, and geopolitical risk have driven a 30bp straight line rally in 10-year Treasuries. Sentiment feels unusually fragile relative to an underlying economy that looks increasingly stable. In my view, the market is too quick to drag downside tail risks into the base case, pricing rate cuts that would require a far sharper disinflation impulse than current data justify. Long-end rates appear to be embedding a growth-risk premium tied to AI and macro uncertainty, even as activity data stabilises – and in places, reaccelerates. If and when the anxiety around AI and SaaS subsides, I would expect focus to rotate back toward the firmer macro backdrop…with higher equities and higher yields the consistent expression of that shift.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/