-

Who We Are

- What We Do

Series: Some Macro Thoughts2026: Starting Strong

By Nohshad Shah

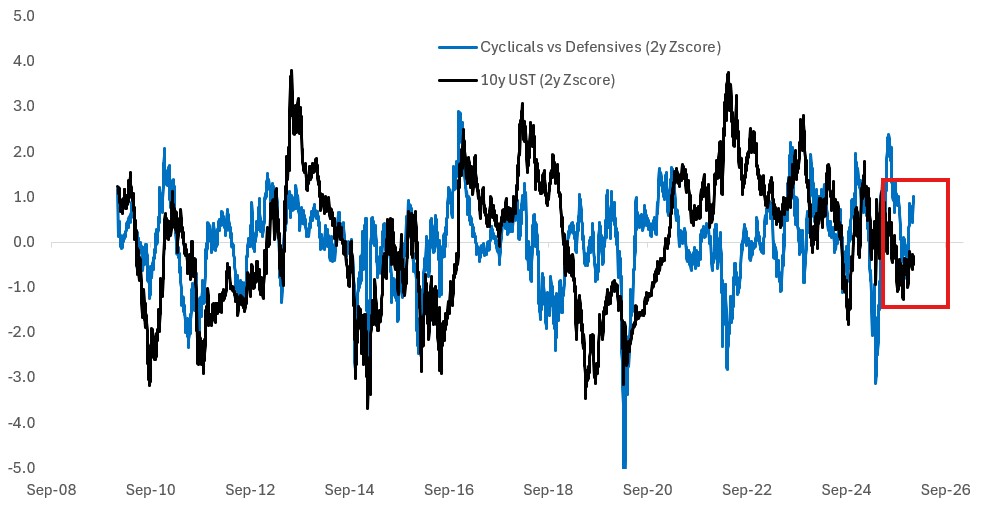

GLOBAL MARKETS HAVE STARTED THE YEAR WITH AN UPBEAT TONE WITH MAJOR EQUITY INDICES AT OR CLOSE TO ALL-TIME HIGHS…which is consistent with my long-held view that 2026 growth will be stronger than expected, driven by a combination of easy financial conditions, loose monetary and fiscal policy, healthy balance sheets supporting consumption, strong corporate profits and the continued AI investment boom. Whilst many forecasters have (finally) upgraded their growth predictions for the year (and removed recession calls), the market still continues to underprice US GDP growth…and there remains a dichotomy between bond and stock markets. Forward-looking equity market internals appear to be better reflecting the acceleration in growth prospects, with cyclicals vs defensives up 12.5% since November (chart below). It’s worth remembering that these moves “under the hood” of the index often represent narrative shifts ahead of moves in bond markets. The NY Fed Nowcast puts US GDP Growth at 2.6% which suggests a continuation of the Q3’25 strong pace (4.3%) following what was likely a dip in Q4 with government shutdowns muddying the waters. Given FCI is close to the loosest it’s been in four years, the Fed has just cut 75bps and President Trump’s OBBA will inject ~1% of GDP worth of fiscal impulse into the economy, this should not come a surprise to anyone. So, against this backdrop, why are rates markets pricing in a further 55bps of rate cuts this year? Two reasons…first, some chance of the labour market slowing down rapidly…and second, a dovish takeover at the Fed, led by a new Chair. On the labour market, my view for some time has been that the primary policy change of last year was immigration, something which will have profound implications for the long-term makeup of the US economy. Net migration moving from +3 million to zero (or negative) means that the labour force has shrunk and will continue to do so, assuming these policies remain in place (which I fully expect). Combined with aging demographics, this serves to constrain labour supply and reduces the breakeven level of job creation…which is consistent with recent labour market data…NFP at 50k (vs breakeven of ~30k)…Prime-Age EPOP near multi-decade highs….and low Initial Jobless Claims (212k 4wk avge.). This tells me that the labour market remains structurally tight with high utilization of the core workforce and real constraints on labour supply with current policies meaning that labour force growth cannot easily come from domestic workers (and that’s before we consider the substitution effect based on relative skills). In sum, this means trend growth is likely running lower than long-term estimates (~1.9%) and market observers may well be surprised at the inflation-generating capacity of the US economy as realised growth accelerates. Some of this could be offset by AI-driven productivity gains (more on this below), but I continue to believe that inflation remains a material risk this year.

Source: Citadel Securities, Bloomberg

Source: FRED

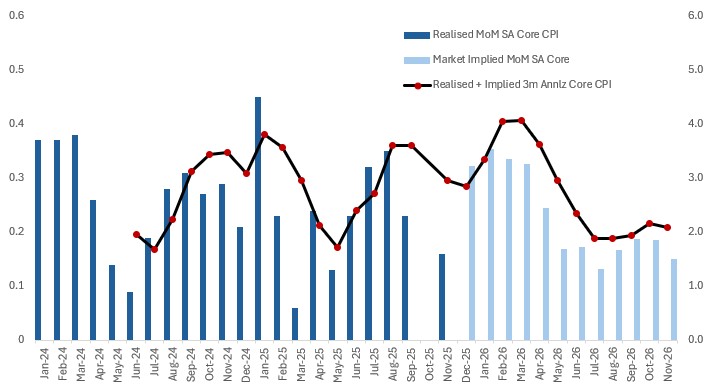

INFLATION MARKETS ALREADY REFLECT A SIGNIFICANT ACCELERATION IN THE FIRST HALF OF THIS YEAR…we can see this by backing out the market implied core inflation level from the prices of monthly inflation fixes which trade in the zero-coupon inflation swap market. These suggest that 3m annualised core inflation is likely to peak above 4% in Q2 this year with 6m annualised over 3.5%…reflecting ongoing tariff passthrough, technical factors which see payback from the low CPI readings in Q4 (related to the government shutdown) and some residual seasonality that sees inflation data print stronger in the first quarter. The concern for investors is that the market is assuming a steep disinflation after that acceleration. However, if my prevailing view of lower trend growth and a tighter labour market materialises, it will heighten the risk of continued accelerating inflation as growth rebounds – this is the key threat for the “disinflation consensus”. What can improve this risk? Productivity gains driven by AI…but in my mind, this will take much longer to play out than the popular narrative suggests…indeed history tells us that it takes time for technological change to show up in official statistics. Geopolitics could play a role…President Trump’s recent takeover of Venezuela means he now controls over 20% of global reserves (2023 measures), although improving the country’s lacklustre production of 1m bpd will take years and much investment. Nevertheless, it likely signals further downward pressure on oil prices in the context of an already oversupplied market (the IEA has forecasted a significant global oil market surplus of 3.84m bpd in 2026).

Source: Citadel Securities, Bloomberg

THE FED CHAIR SAGA IS NEARING THE END…consensus and betting markets imply roughly equal probabilities for Kevin Hassett and Kevin Warsh around 40%. Both are assumed to be effective in steering the committee towards a more dovish pathway with respect to policy rates. However, I do think that the appointment of Warsh leans materially more hawkish with respect to balance sheet policy, given his historical stance on the issue. The question for markets regarding Hassett is whether his loyalty to the President is considered too close for comfort…and if the discounting of additional policy easing because of his pick is offset by higher term premium in the long end of the yield curve (crucial for financial conditions). This is important in the context of a 10yr yield which has steadfastly refused to move much lower despite 175bps of rate cuts over the last 16 months. In terms of Trump-dominance over the Fed, my view historically has been that the power of the Chair alone to drive a meaningful shift in the policy outlook – regardless of the economic data – was limited, given the composition of the board and the assumption that regional Presidents would be reappointed, ensuring the impartially and credibility of the institution. That still remains my base case. However, there is an alternative scenario in which Powell departs from the Board and several of the established Governors follow suit alongside him, in which case the check on the Administration’s influence over monetary policy could be diminished. This is a risk worthy of consideration. All told, my expectation is that we will undershoot the current market pricing of rate cuts for this year…driven by the strength of the economic outlook, inflation (and “affordability”) concerns and perhaps even the simplistic point that if we do enter an AI-induced bubble in the stock market, fuelling it further with more stimulative policy is just not prudent.

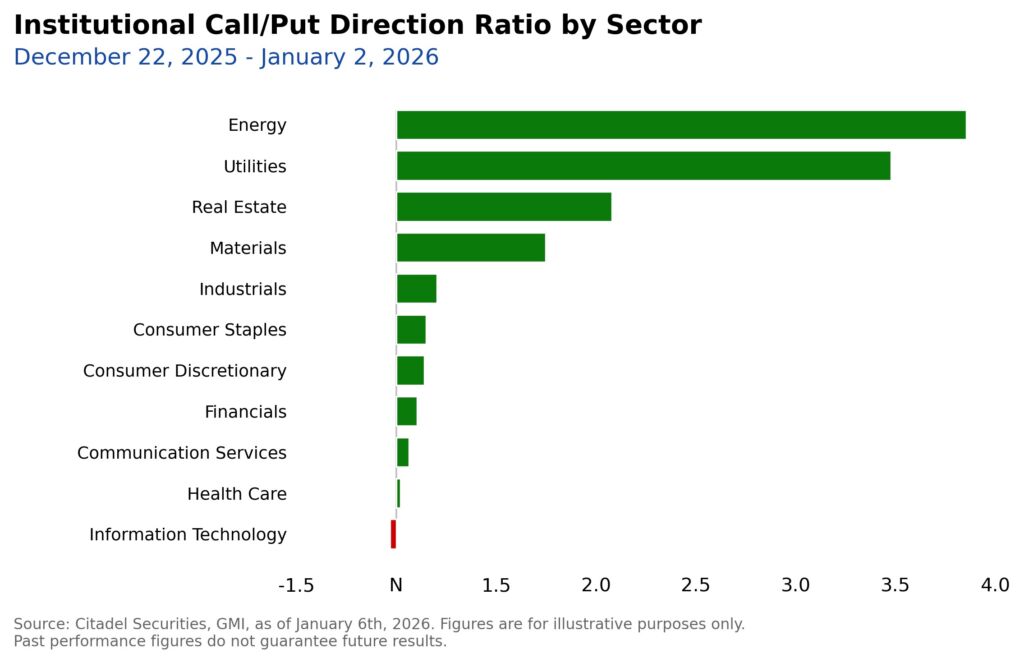

Q3 PRODUCTIVITY PRINTED AT 4.9% WHICH HAS DRAWN A LOT OF ATTENTION…particularly in the context of a market that is hyper focused on AI adoption. Indeed 90% of respondents to our recent AI client survey said they expect it to deliver a positive productivity shock. That said, I’m skeptical of this specific Q3 data…productivity is notoriously hard to measure and highly prone to revisions and subject to QECW benchmarking. Moreover, it is highly volatile across quarters and the 4.9% reading came after two weak prints which implied an annual rate of 1.9% y/y. I’d also be very surprised to see AI impact official statistics on productivity any time soon…generally, the adoption of new technologies takes time – in a Brookings survey of 1000 American adults conducted in Q4 last year, only 19% reported an increase in productivity as a result of using AI tools and there is clear uncertainty around the pace of adoption, especially in a professional context. For the avoidance of doubt, I remain optimistic that AI will deliver meaningful productivity gains, but just over a longer time horizon. Markets tend to be overly focused on near term gains and do not pay enough attention to the impact of multi-year compounded total factor productivity gains. None of this suggests that hyperscaler valuations are unsustainable – and I don’t think that dot-com bubble comparisons are necessarily that helpful – firstly because the forward P/Es of the leading companies are much lower than at the peak of the dot-com era. Secondly, we are seeing a healthy increase in breadth – Citadel Securities Equity Client Franchise flows skew towards topside buying in Energy, Utilities, Real Estate, Materials and Industrials (in keeping with the cyclicals theme noted above), whereas option flows in Tech have been much more directionally balanced. I fully anticipate that investors will continue to be increasingly discerning in how they reward/punish AI capex overspend especially as we expect hyperscaler issuance this year to (at a minimum) be flat to the ~$100B in FY25. Further, my expectation is that the market slowly realises that the greatest beneficiaries of AI will not necessarily be the ones investing in the infrastructure but those that integrate it into their workflows to deliver margin expansion (as well as firms that provide the AI software to deliver widespread productivity enhancements). Ultimately, investors will always reward most the companies that focus on systematic, long-term execution not necessarily opportunistic growth.

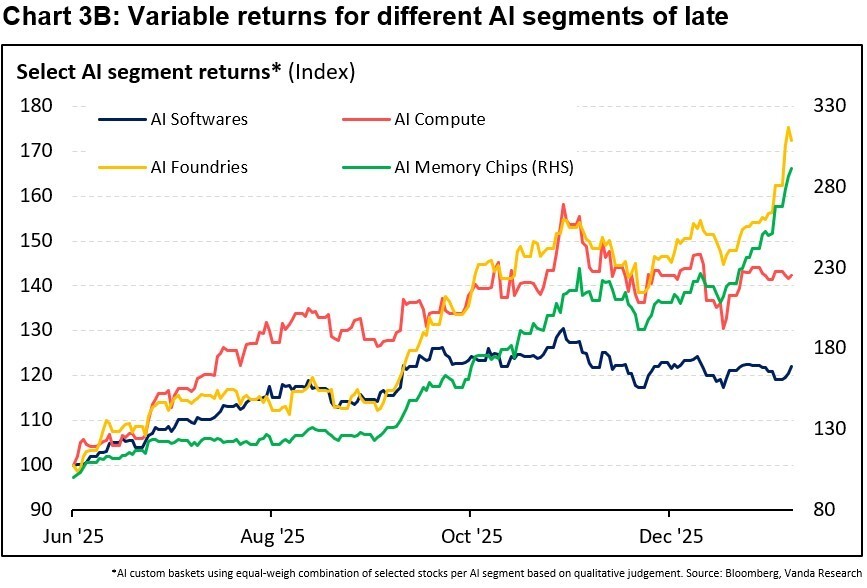

Source: Vanda

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Market Insights - What We Do