-

Who We Are

- What We Do

Series: Some Macro ThoughtsA.I. Versus the Real Economy Narrative

By Nohshad Shah

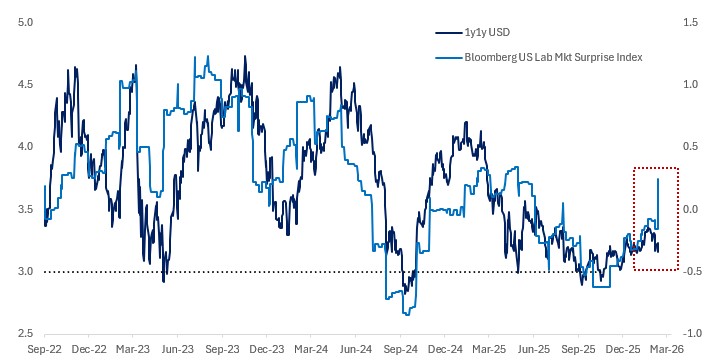

THE US LABOUR MARKET IS BEGINNING TO CATCH UP WITH THE GROWTH OUTLOOK…that was the clear signal from this week’s jobs report. Nonfarm payrolls rose +130k, well above expectations (+68k), while the unemployment rate fell below 4.3% (4.28% unrounded). Private payrolls increased a healthy +172k and average hourly earnings rose +0.4%, both meaningfully above consensus. Regular readers will know I have been decidedly bullish on the US growth outlook for some time. The rebound from tariff-related uncertainty, an unprecedented late-cycle mix of easing monetary policy alongside incoming fiscal stimulus, and still-loose financial conditions, have combined to create a constructive macro backdrop. The one lingering concern had been labour market softness, particularly after annual revisions lowered 2025 job creation to ~181k following a -403k adjustment. The negative revisions were centred on the earlier part of the year and markets are more likely to focus on the recent prints which imply risks are skewed toward reacceleration rather than deterioration. Recall that the breakeven pace for payroll growth is now only +30–50k given the sharp slowdown in net migration. Against that benchmark, current job gains remain comfortably expansionary. While healthcare (+82k) and social assistance (+42k) were the largest contributors, the breadth of gains was encouraging with more than half of sectors seeing net job gains, suggesting a broader recovery in labour demand. Prime-age labour force participation also rose to new highs, indicating that improved job prospects are drawing workers back in. Under the hood, labour force flows look even healthier: more unemployed workers are finding jobs, and fewer employed workers are losing them. That combination lowers unemployment for the “right” reasons – stronger hiring and reduced layoffs – rather than labour force exits. This aligns with broader activity data…both manufacturing and services PMIs remain in expansion territory, with forward-looking components such as new orders and business expectations picking up and employment subindices stabilising. Earnings data tell a similar story…Q4 reporting season has delivered solid results…with three quarters of companies having reported, 74% have beaten earnings estimates and 73% have exceeded revenue expectations. Blended YoY earnings growth stands at ~13%, and if sustained, would mark a fifth consecutive quarter of double-digit growth. Taken together, the data suggest the US economy has rebounded strongly from last year’s uncertainty…nominal growth in the 5–6% range for 2026 looks highly achievable, supported by a uniquely accommodative policy mix and a once-in-a-generation AI-driven capex boom exceeding $600bn.

1y1y USD Swaps; Bloomberg US Labour Markets Surprise Index

Source: Bloomberg, Citadel Securities

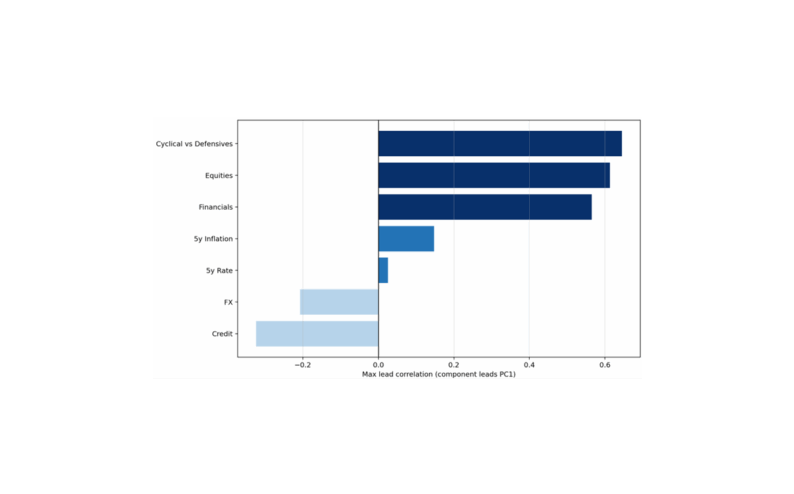

THE CURRENT POLICY MIX IS HISTORICALLY LOOSE. Fiscal policy remains highly stimulative: CBO data show the deficit as a share of GDP sits in the 16th percentile of its 64-year history and the 35th percentile of its 20-year history (where a lower percentile implies a larger deficit and therefore greater stimulus). Monetary conditions are similarly accommodative. The Fed has delivered 175bp of rate cuts, and financial conditions now sit at their easiest level since April 2022. The 12-month impulse in the Fed’s FCI-G (rolling 12m change) is in the 12th percentile of its 25-year history, underscoring how significant the easing shift has been. This combination of very loose fiscal and very loose monetary policy is unusual outside of crisis periods. The Fed began cutting in September 2024 to safeguard the labour market…since then, the unemployment rate has risen just 0.2% from the start of the easing cycle and remains only 0.9% above the 3.4% cycle low reached in April 2023. Labour market concerns are fading fast, consensus growth expectations have been revised higher (from 1.8% for end-2025 to ~2.3% today), and AI-related capex continues to exceed expectations. Despite this improving macro backdrop, markets still price a terminal Fed rate just above 3%…essentially the same endpoint priced during peak labour market concerns in September 2025. The result is financial conditions that are easier relative to the growth trajectory than would typically be expected. Ordinarily, improving growth would prompt markets to price a more hawkish policy path, tightening conditions in a countercyclical fashion. That offset has so far been absent – likely reflecting some combination of a “Fed chair premium” and expectations of a powerful AI-driven productivity boom. We can see this empirically by decomposing the move in financial conditions using my colleague Frank Flight’s cross-asset framework, which isolates the drivers in stocks, yields, credit and FX into growth and policy vectors using principal components analysis. The decomposition shows a significant decline in the policy factor (PC2, chart below) – effectively a sharp repricing toward easier conditions. That move appears inconsistent with the policy-relevant data over the past week, which has included stronger jobs data and firmer PCE expectations. In other words, markets have pushed yields lower and eased financial conditions further even as the growth backdrop has strengthened and the case for additional policy easing has diminished.

Policy factor from FCI

Source: Bloomberg, Citadel Securities

THE FIRST-ORDER TAKEAWAY FOR MARKETS IS THAT WEAKNESS IN SOFTWARE AND BROADER AI-RELATED FEARS HAVE OVERWHELMED THE “REAL ECONOMY” NARRATIVE. If that rotational pressure begins to fade, it would clear the way for performance at the index level to better reflect the improving cyclical and earnings backdrop. A firmer footing for equities should, in turn, put upward pressure on bond yields. However, absent a move higher in yields, stronger equity performance would continue to ease financial conditions via the policy factor – assuming the dollar remains anchored. In other words, if equities rally and bond yields fail to adjust, the overall policy mix becomes even looser relative to the growth trajectory – an imbalance that is unlikely to persist. Simply being long equities at current fixed income valuations leaves the position exposed to a snap-back toward a more hawkish policy regime. Instead, pairing equity exposure with a short duration position hedges the risk that stronger growth ultimately forces bond yields higher, tightening financial conditions.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Market Insights - What We Do