Our GMI market capitulation checklist has not yet fully healed; however, as futures rebound this morning, it is clear that the reflexive squeeze and short-covering bid remains elevated. Many of these technical, flow-of-funds dynamics continue to create air pockets in both directions.

As key technical and positioning pressures begin to clear, and IF geopolitical tensions ease, April has the potential to be a strong month for US equities. Upside tail risks appear underpriced, and in this type of environment, buyers tend to live higher.

We removed our bearish February stance, shifted to neutral into March options expiration, and are now tactically bullish into April. Our positioning and sentiment indicators suggest that investor positioning has become overly extended to the downside.

GMI: April Checklist

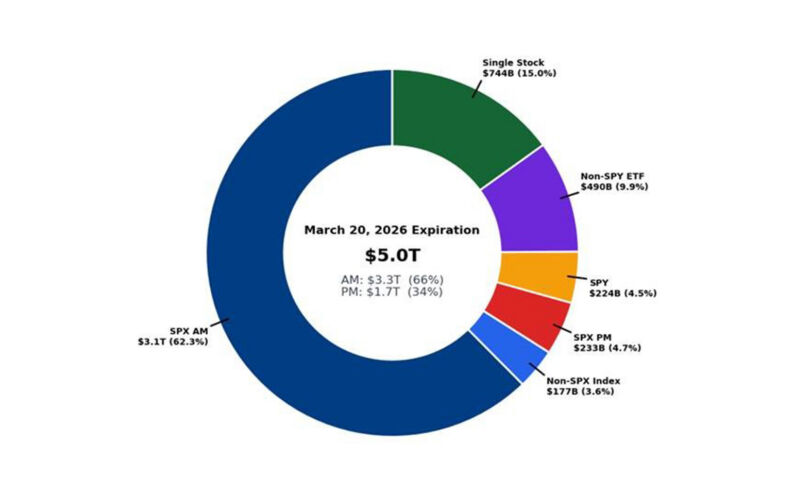

I. Quadruple Witching Option Expiration

OpEx will represent the largest technical event of the month, with ~35% of US options exposure set to roll off by March 20th – a clearing event for gamma that could meaningfully loosen the mechanical constraints currently anchoring the index.

II. Volatility Stress

S&P 500 skew reached the 98th percentile over the past five years, driven by elevated institutional hedging demand. With ~25% of options expiring, delta-hedging pressures have eased.

New overwriting strikes are now positioned higher and more dispersed, reducing the strength of the upside gamma wall in a move higher. Volatility is no longer the coach from the sidelines, it is QB1, telling when teams can re-risk.

III. Systematic De-Grossing Supply

Systematic strategies – including CTAs, Risk Parity, and Vol Control – have triggered de-risking flows below the 200-day moving average (~6622), amplifying recent downside pressure. Our 10% vol-targeting model has already reduced exposure by more than 20%.

These strategies could transition into incremental buyers if the market were to move higher.

IV. Liquidity Conditions

While trading volumes remain elevated (~20B+ shares/day), market depth is extremely thin. Last week, S&P 500 top-of-book liquidity was in the 3rd percentile over the past two years. Investors can transact ~$2.5M at the touch versus a ~$12M YTD average, which is back to Liberation Day levels. Lower top book liquidity hinders the ability to move risk quickly without impact.

V. Elevated ETF Short Base

ETFs have accounted for ~35% of trading volume over the past three weeks, peaking at 47%, and setting a record streak above 35%. This reflects active shorting via ETFs to reduce net exposure. Both net and gross exposures have declined, while levered end-of-day ETF flows remain a key driver of intraday volatility.

VI. Quarter-End Rebalancing Flows

March 31 marks the final major negative technical flow event, driven by pension rebalancing and quarterly options expiration.

Pensions are expected to continue reallocating toward fixed income while reducing equity exposure, providing potential support to rates markets. Significant options open interest will also roll off into quarter-end.

VII. Q2 Reset: New April Inflows vs. Record Outflows

We see a new technical dynamic this April: capital “repatriation” back to the USA (not rest-of-world), back into technology (Mag 7), and back into quality.

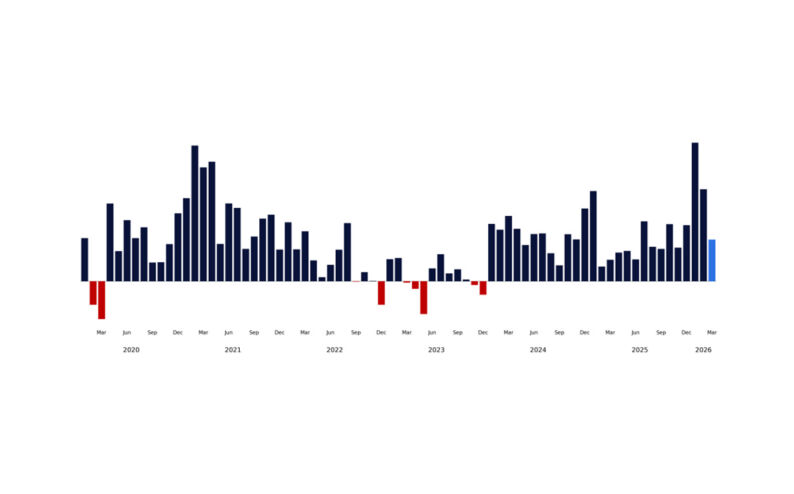

ETF inflows have already reached $518 billion year-to-date, more than 30% ahead of last year and more than 5x the average by this point in the year. In an environment where liquidity remains thin and trading is increasingly concentrated in passive vehicles, these reallocations can have an outsized impact on price action.

US ETFs have seen significant outflows. As positioning resets into Q2, this flow-driven backdrop favors large-cap, liquid equities – particularly US mega-cap technology.

VIII. Sentiment Reset

The Citadel Securities Retail RORO (Risk-On/Risk-Off) has declined sharply from February highs. In addition, the AAII Bull/Bear Spread has reset to the lowest level in 3 months, while CNN Fear & Greed stands at 15 – down ~50 points from January and its lowest level since November.

IX. Seasonal Tailwinds: April

Since 1928, April has been the second-best month for S&P 500 returns, with an average gain of +1.3%. The index has risen in 63% of Aprils, with average upside of ~4.3% in positive months. Seasonality is also front-loaded, with strength concentrated in the first half of the month (average 1H return = +0.91%; average 1H rally = +3%).

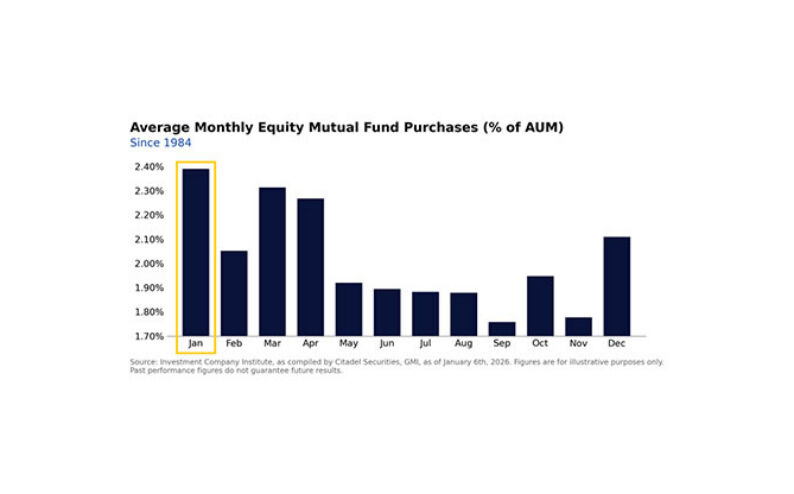

X. Tax Refunds

We are in the heart of tax refund season, with 53% of annual refunds issued by April 1st and roughly 75% by April month-end. Citadel Securities’ retail flow data shows this has historically coincided with a pickup in retail activity.

XI. Retail Re-Acceleration

Retail investors have still been net buyers of US equities each week in March (and since the end of November), despite a moderation from the record pace earlier this year. Retail selling pressure over the last two weeks has been limited to 3 trading sessions only.

Year-to-date, average net notional traded on our platform has been more than 3x higher on S&P down days versus up days. This spread has widened further in March, as retail investors began selling into strength. We are seeing this again this morning – retail flows on our platform were relatively flat ahead of the Trump announcement, now they are monetizing the pop higher after being strong net buyers last week.

Our options flows have also been net bullish over the same period. Citadel Securities retail flows show no signs of weakness from retail investors, more of a holding pattern, and willing to continue buying the dip once all clear.

XII. GMI BOTTOM LINE

The setup for April is increasingly constructive.

While risks remain and the broader capitulation checklist is not fully resolved, our data-driven assessment of sentiment and positioning is overwhelmingly bearish.

We will continue to monitor developments and update the GMI Capitulation Checklist accordingly – but for now, the balance of risks has tilted to the upside.

Copyright © Citadel Enterprise Americas LLC or one of its affiliates. All rights reserved.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CDGE”) authorized and regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch authorized and regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the Japan Financial Services Agency (“JFSA”); and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”), Financial Industry Regulatory Authority (“FINRA”), and Securities Investor Protection Corporation (“SIPC”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC, FINRA, and SIPC, or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity. Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at www.citadelsecurities.com/GlobalSalesTrading.