-

Who We Are

- What We Do

Series: Some Macro ThoughtsATH

By Nohshad Shah

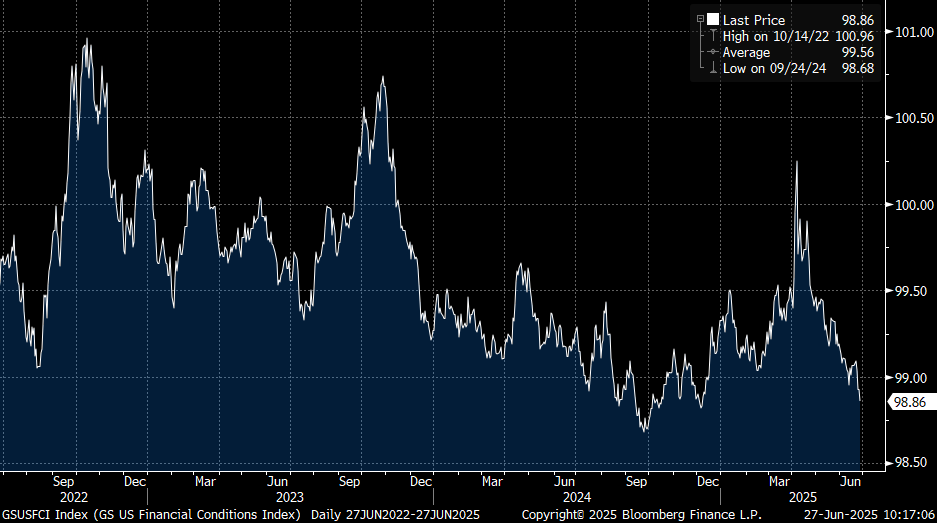

BACKDROP FOR RISK ASSETS CONTINUES TO IMPROVE FURTHER. For the last two months I have been articulating the upside case in equities driven by a mix of reduced tail risk (mostly policy-induced), solid earnings growth and an easing of financial conditions (FCI). These factors have served to substantially improve the forward US economic growth outlook, leaving open the right-tail of the distribution for risk asset performance. Indeed, this week SPX hit all-time highs in a powerful rally reflecting the dramatic change in the macro landscape since April’s liberation day. Whilst it’s natural for investors to take pause, my view is that the path of least resistance remains higher. Let me explain why. This week saw a continuation of recent positive news…geopolitical concerns tensions eased with a ceasefire agreement in the Isreal-Iran conflict…Treasury Secretary Bessent confirmed the scrapping of the ill-fated 899 provision in the fiscal bill…Nvidia stock hit all-time highs ($3.8tn market cap; world’s most valuable company) with renewed optimism from Jensen Huang on robotics…and FCI eased substantially (chart below) with sizeable contributions from equities (SPX +3.6%), bonds (10y UST -12bps) and the US dollar (DXY -1.6%). President Trump’s frustration with Fed Chair Powell’s wait-and-see approach to monetary policy has become an increasing focus for market participants with noise around a potential summer announcement of his replacement. Betting markets have Chris Waller and Kevin Warsh as joint favourites (see below), but regardless of who it is, the implications of a “shadow chair” could prove tricky for POTUS. In theory, the early nomination allows the chair-in-waiting to influence market pricing of the future policy rate path…likely with a dovish tilt, prior to taking office. But the risk is of intense prolonged scrutiny of these pronouncements for 8-9 months, bringing the issue into focus for both markets and the Senate – who have to confirm the candidate. Moreover, markets could easily lose confidence in the Fed (as observed in April’s episode) and other FOMC members (including Powell himself) would almost certainly not appreciate the criticism…potentially making it more fractious for the new Chair when they eventually start. As with so much these days, we may well be entering unchartered territory. However, it is true to say that recent Fedspeak has had a dovish tilt with both Governors Chris Waller and Michelle Bowman angling for a July rate cut – buoyed by recent benign inflation figures and some weaker data. The market has taken note of these developments, moving to price 64bps of rate cuts by the end of this year. This will only serve to ease financial conditions further…through the monetary policy channel…creating a self-re-enforcing feedback loop of lower bond yields, a weaker US dollar and higher stocks. And that’s before considering the incoming large positive fiscal impulse. The bottom line is that the US economy has shown remarkable resilience in recent months, having been hit with a barrage of uncertainty from the new Administration’s unconventional policies. Despite this, growth has held up…as has the labour market…and with tail-risks reducing with each coming week, the emphasis has shifted firmly to the forward-looking outlook: unrivalled dominance in AI (with $600bn+ of investment and counting)…the engine of both US and global economic growth for decades to come…with both monetary policy and fiscal policy priced to ease in coming months despite FCI being close to the loosest in three-years! The question is not IF you should be long equities…it is…are you long enough?

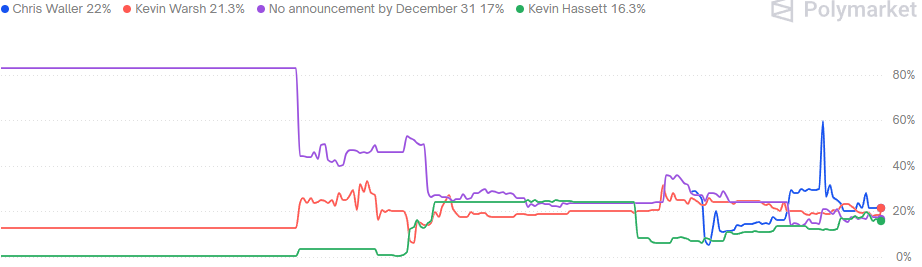

Who will Trump announce as next Fed Chair?

Source: Polymarket, 27jun25

Source: Polymarket, 27jun25US Financial Conditions Index

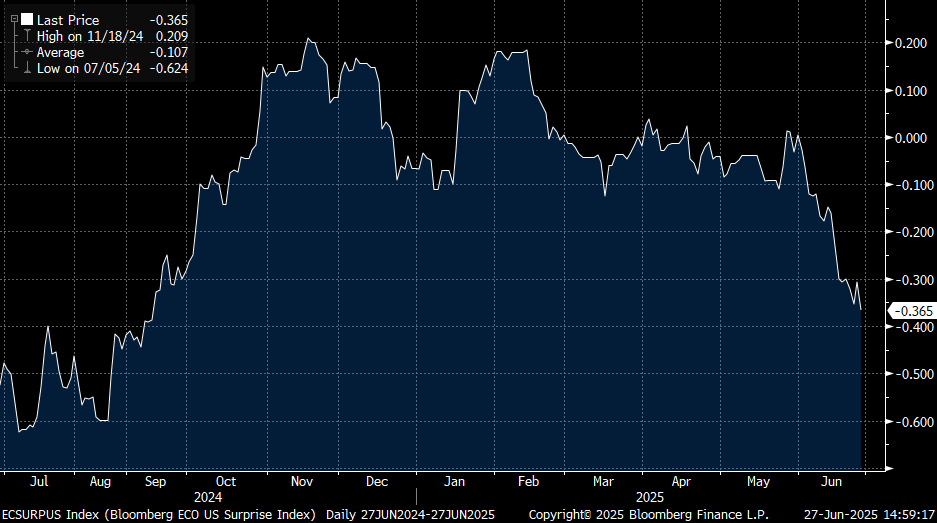

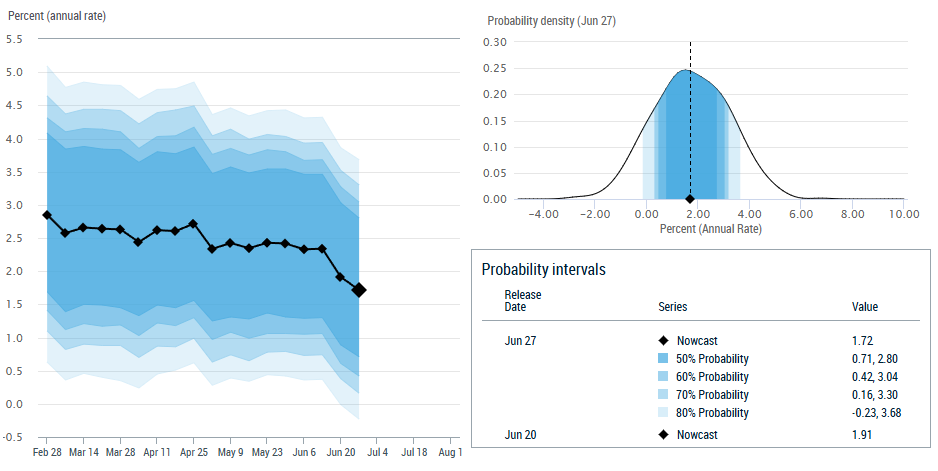

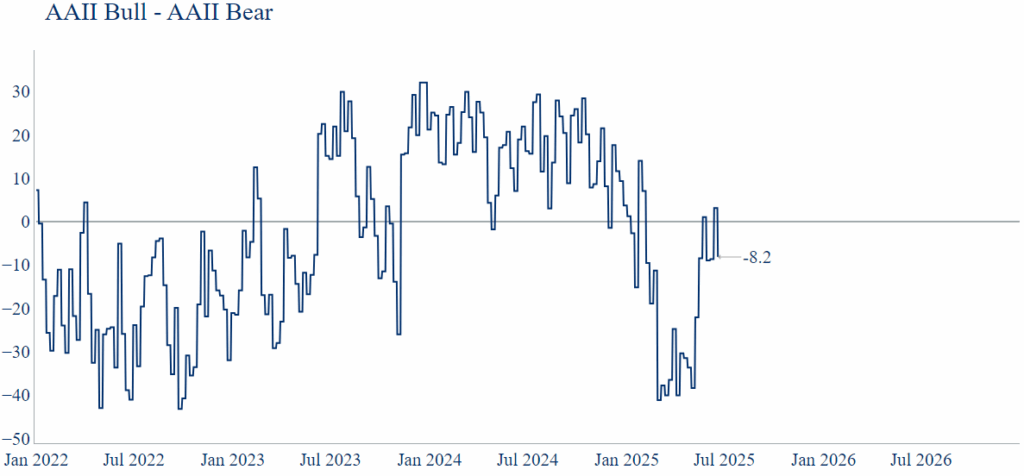

Source: Bloomberg, 27jun25SOME OF THE RECENT DATA HAS BEEN WEAK…most neatly captured in the Bloomberg Economic Surprise Index, which has been on a consistent downward path this month (chart below). The Conference Board Leading Economic Index (LEI) also continues its negative trend at 99.0 reflecting “consumers’ pessimism, persistently weak new orders in manufacturing, a second consecutive month of rising initial claims for unemployment insurance, and a decline in housing permits weighed on the Index, leading to May’s overall decline. With the substantial negatively revised drop in April and the further downtick in May, the six-month growth rate of the Index has become more negative, triggering the recession signal”. The labour market is treading water – Job Openings languish around 7391k…NFP an unspectacular 139k…and Initial Clams at 245k (4w moving avg.)…still well below levels typically associated with a recession (~350k+). The NY Fed’s Nowcast has GDP tracking at 1.72% from ~2.5% entering this year…slowing, sure…but far from recessionary. One can expect some further weakness as the hard data starts to reflect the weaker soft data from April/May and seasonal weakness in the labour market reveals itself. This is not a cause for panic – the forward outlook is rapidly improving and indeed, if we do see material signs of weakness in the labour market, it will likely perpetuate more dovish rate pricing in the front-end of the curve, thereby generating even greater stimulus for a risk rally. Speaking to my esteemed colleague Scott Rubner (you’ll hear a lot more from him soon) he notes that the month of July is seasonally very strong for equities – apart from momentum factor unwinds in 2024, NDX has traded higher in each of the prior 16 years…and with institutional sentiment only just recovering towards neutral (AAII chart below), the risk is one of a re-leveraging in stocks, especially as VaR windows normalise with the tariff tantrum fading in the rear view mirror.

Bloomberg Economic Surprise Index

Source: Bloomberg, 27jun25NY Fed Staff Nowcast

Source: NY Fed, 27jun25AAII Investor Sentiment Survey

AAII, 27jun25

ON THE FISCAL FRONT…the One Big Beautiful Act (OBBA) hit a snag as parliamentarian Elizabeth MacDonough frustrated GOP proposals for fast-track legislation by ruling that some of the provisions related to Medicaid violated the Byrd Rule, which governs what legislation can pass with a simple-majority (rather than the typical 60 votes required) and avoid a filibuster under budget reconciliation rules. In the last week, she ruled that more than two dozen provisions violated this rule, meaning that Republicans will need to devise alternative ways to find savings to fund corporate tax cuts. Whilst some lawmakers called her for her firing, cooler heads will likely prevail and they will be wary of creating a precedent for rule-breaking, which could hurt them in the future. President Trump continues to vocally assert the benefits of his fiscal bill, affirming my belief that this is the most crucial pillar of his entire domestic agenda. Unlike tariffs, which had many dissenting voices, corporate America certainly wants and expects this legislation to be passed – 86% of CFOs surveyed by CNBC expect Trump’s 2017 TCJA tax cuts to be made permanent. Whilst there are some sensible voices highlighting the risks from America’s fiscal profligacy, the political class is not (yet) of the mindset to listen.

SO…WHAT ARE THE RISKS? With the backdrop of solid (but not spectacular) economic growth and a resilient labour market, we now have very easy financial conditions driven by a weakening USD (structural hedging flows), a bond market rally (softer spot data and seasonals) and strong equity markets (buttressed by Big Tech/AI). Into this, we now add potentially a more dovish Fed outlook…should the FOMC react to spot data and/or the President appoints a structurally dovish Chair…and a substantial fiscal package, which is front-loaded in nature with a growth impact of +0.9% GDP in 2026. The natural result of such a potent cocktail of policy measures is stronger growth and higher inflation. My sense is that Chair Powell knows this…which is why he has been so reluctant to cut rates, though it remains unclear how long he’ll be able to holdout against the chorus of voices (the loudest of which is the President himself) calling for more easing. Time will tell. The asset price implications are also clear…a weaker currency…higher equities…and higher long-end yields even with lower policy rates. As mentioned in last week’s note (“Goldilocks Summer”), in the near-term I expect bond yields to move lower. But ultimately, 10y yields will need to compensate investors for higher inflation risk. Expect elevated term premium and steeper curves to prevail over the medium-term.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Some Macro Thoughts - What We Do