-

Who We Are

- What We Do

Series: Some Macro ThoughtsAwaiting Liberation

By Nohshad Shah

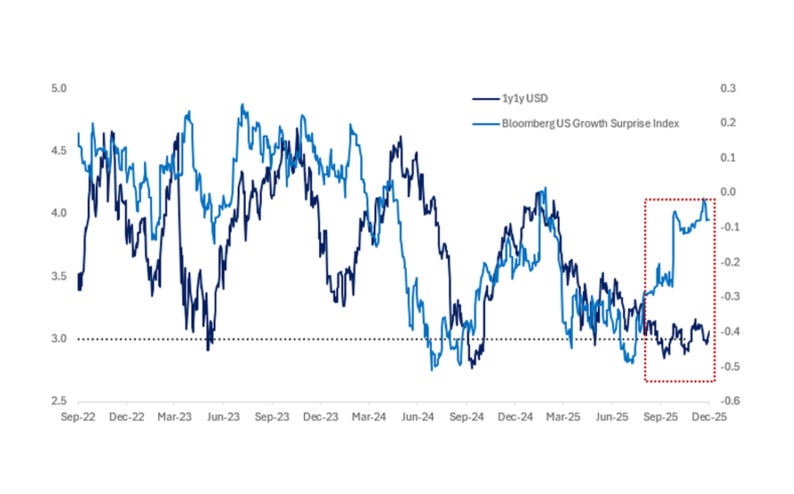

IN LAST WEEK’S NOTE I highlighted the substantive difference in tone in the dovish presser from Chair Powell…and the more hawkish movement in the dots from other FOMC members, reflected in the Summary of Economic Projections (SEP). Since then, the hawkish members have come out in force to state their case with Golsbee, Bostic, Musalem and Kugler on the tapes:

“If you start seeing market-based long-run inflation expectations start behaving the way these surveys have done in the last two months, I would view that as a major red flag area of concern,” – Goolsbee

“I moved to one mainly because I think we’re going to see inflation be very bumpy and not move dramatically and in a clear way to the 2% target,”

“Because that’s being pushed back, I think the appropriate path for policy is also going to have to be pushed back.” – Bostic

“If inflation expectations are threatening to become unanchored or becoming unanchored in the long term, then the balanced approach may not work,”

“we would have to probably lean into the inflation side of our dual mandate, to make sure inflation expectations and inflation remain anchored.” – Musalem

“Importantly, while goods inflation was negative in 2024 — as was the norm before the pandemic — it has turned positive in recent months,”

“This development is unhelpful because goods inflation has often kept a lid on total inflation and also affects inflation expectations.” – Kugler

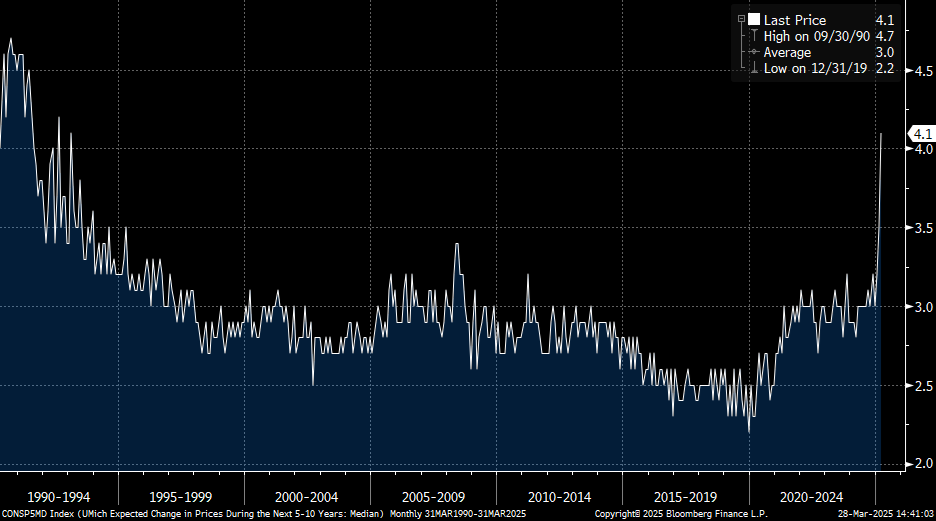

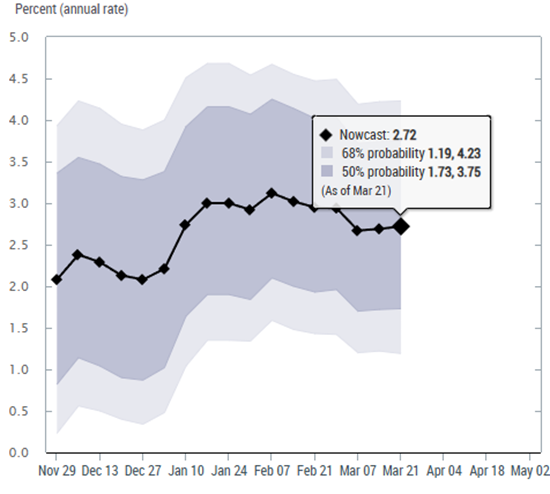

These comments reflect a real concern around inflation expectations…rightly so, given that under most estimates, upcoming tariff implementation could lead to core PCE reaching 3-3.25%, well above the Fed’s 2% target. Indeed, UMich Inflation expectations on Friday showed a further move higher with short-term at 5% and long-term 4.1%, the highest reading since 1993. In the meantime, the hard data continues to be robust – slowing, sure, but from an above-trend starting point…GDP tracking for Q1 remains at 2.7% (NY Fed Nowcast)…and the labour market is balanced with NFP 3m Avge at 200k and u/e rate 4.1%. But as we all know, the market has been squarely focused on the risks to growth driven by policy uncertainty…as reflected thus far in weaker “soft data” prints. Interestingly, even on this front we got stronger Flash PMI prints this week (composite 53.5 vs 50.9 exp.) suggesting the start of an uptick from the downtrend since December. Of course, consumer sentiment remains a key factor to watch with both The Conference Board and Michigan Sentiment data still weakening sharply. In sum, I continue to believe that what we’re seeing is a correction in growth, but not a recession. And if moves in the stock market can be stabilized with a less volatile outlook on tariffs (more on this below), then what we’re left with is mid-to-high 1% GDP growth, a stable labour market…and inflation that remains above target, with risks to the upside. In that context, Chair Powell’s dovish stance may be considered puzzling…but given heightened uncertainty and jittery markets, why tighten financial conditions at this point…and risk antagonizing President Trump in the process. There is no need…at least until we have greater clarity. Indeed, a risk management approach…perhaps of the career kind.

Source: University of Michigan Survey of Consumers, Bloomberg

Source: Federal Reserve Bank of New York

TARIFFS REMAIN A HIGHLY UNPREDICTABLE FACTOR for the global economy and there’s no edge in predicting outcomes. We have done some analysis on the high-level scenarios that might play out. The table below (h/t: Grant Wilder) highlights three scenarios (high, moderate, low) for effective tariff rates and their likely impact on growth and inflation. In the most negative scenario, we see a 0.6% hit to US GDP in 2025, whilst the inflationary impact could be as much as 0.4% on the CPI measure. Following President Trump’s announcement of 25% tariffs on foreign-made automobiles (starting 2 April), the inflation market reacted accordingly with 2y breakevens rallying ~10bps to reach a multi-year high of 3.28%…our inflation trader Durham Abric noted “75% of US vehicles are imported (5.5% CPI weight), implying 1% upside given a full pass through to CPI”, whilst appreciating that pass-through will be limited by demand destruction, margin compression and likely rotation into the used car market. This is simply a preview of what lies in wait for “liberation day”…though it’s important to note that Administration officials have signalled there will be specific details as part of the announcement with reciprocal tariffs likely to be imposed at the country level (as opposed to products) based on factors such as pre-existing tariffs, currency manipulation, VAT and non-tariff barriers…with an emphasis on ~15 countries considered to be the worst offenders (highest trade surplus’ against the US). In addition to the reciprocal tariffs, there are likely to be ones on individual sectors, potentially pharma and semiconductors. The chronology is likely to be…high level announcements on 2 April…then individual countries will have the chance to negotiate…a drawn-out process. This suggests to me a phased approach, likely to result in a material and extended impact on both spot inflation and inflation expectations. The implications for growth will depend partly on how financial conditions react to the announcement…on the one hand, the relative certainty compared to the back-and-forth of recent weeks could provide some respite for risk assets…on the other, the hit to consumers as the largest component of GDP may just be too much to ignore. For now, President Trump (like the Fed) will be buoyed by the hard data holding up – so don’t expect much let up in the tariff agenda.

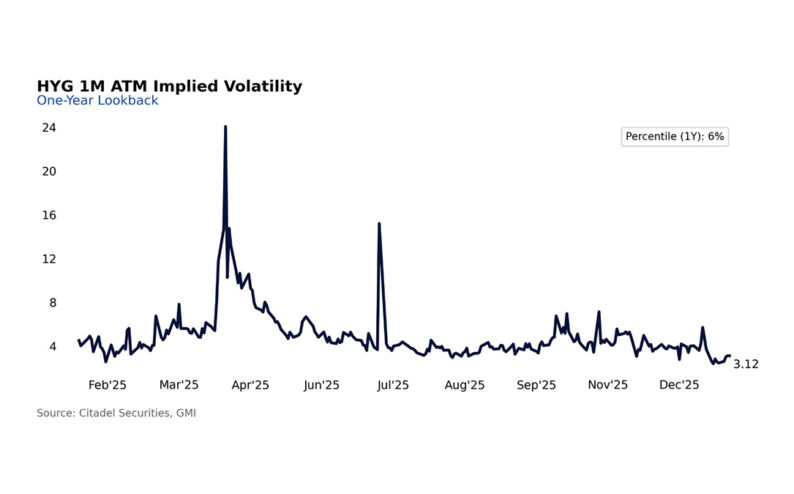

Source: Citadel Securities, 24mar25

AS I’VE MENTIONED BEFORE, THE LONG-TERM RAMIFICATIONS OF THE “AMERICA FIRST” AGENDA ARE PROFOUND. This was laid bare in a thought-provoking article from the esteemed economist Barry Eichengreen. In it he highlights the evolution of the US dollar as the world’s reserve currency and the institution-building that was essential to this – the IMF, World Bank, Bretton Woods…and most importantly an independent Federal Reserve Bank. The Marshall Plan to provide Europe with US dollars to re-invigorate their economies and return to the international payments system also played a crucial role. The dollar’s continued dominance derived not only from it’s outsize share of GDP and trade, but equally from “relationships and reciprocity”. The numbers have been trending downwards for some time…US GDP is now ~15% of global (from 25%)…with US share of global exports ~11% (from 18%). An acceleration of these trends driven by the disengagement of the US from global trade will only serve to undermine the dollar’s international status as importers and exporters seek to diversify…to quote Eichengreen: “when the weight of an economy in global trade and finance declines, the market forces making for widespread use of its currency have a corresponding tendency to weaken”. And that’s without getting into considerations around geopolitics and the weaponization of the dollar for economic sanctions. Ultimately, my view is that an America First agenda that incorporates a retrenchment of the United States from the world, both economically and geopolitically, and risking the sensitive balance of independent institutions and politics, cannot be good for the value of the US dollar. There might be short-term cross-currents, but it’s difficult to argue against a long-term decline in its value.

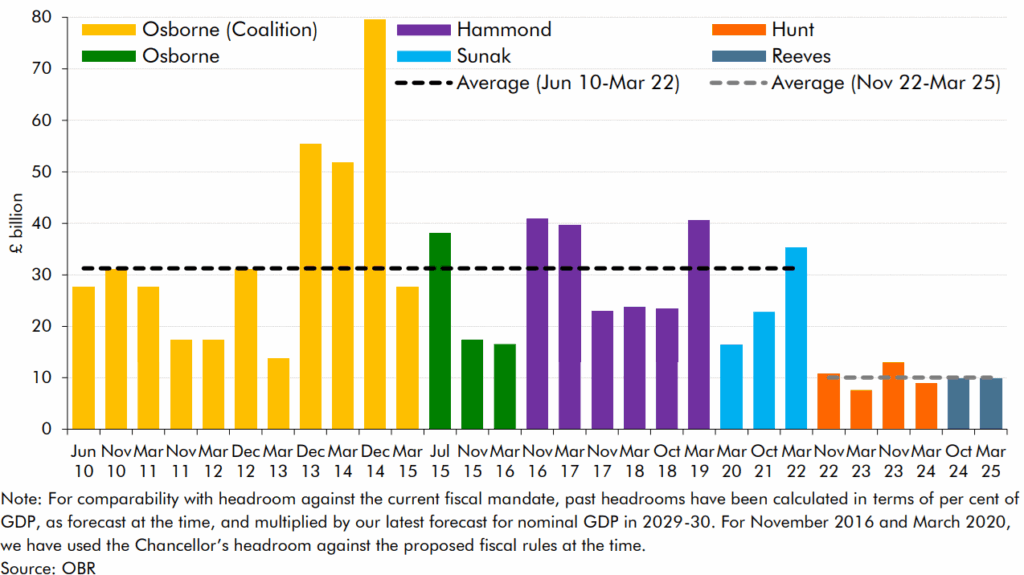

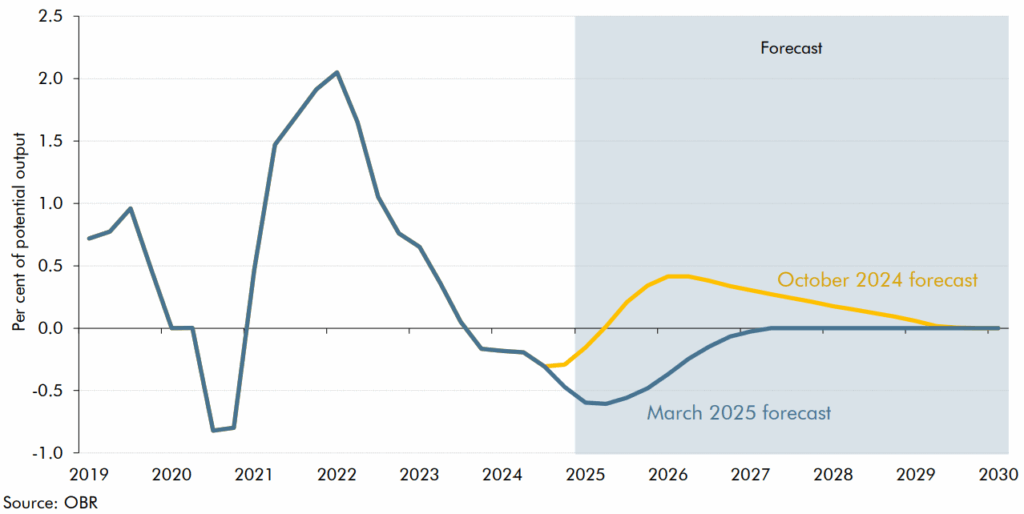

MEANWHILE IN BLIGHTY…the outlook continues to get even more challenging. UK Chancellor Reeves was forced into substantive adjustments in her Spring Budget due to her self-imposed “fiscal rules” (current spending must be balanced with tax receipts by 2029/30) revealing a £14bn plan to fix the public finances. The fiscal outlook has sharply deteriorated since the budget in October…with higher debt interest repayments and lower tax receipts contributing to a move from £9.9bn of “headroom” to a deficit of £4.1bn. Chancellor Reeves sought to restore the headroom with a number of measures including cuts to welfare benefits, broader reductions in spending, more emphasis on tax collection and boosts from other policies such as planning reforms. However, the independent Office for Budget Responsibility (OBR) poured cold water on the announcements suggesting there was only a “very small margin” of flexibility, which could easily be wiped out by an escalating trade war or similar factors. Indeed, the current headroom is amongst the lowest of any Chancellor since 2010 (see below). What’s striking is the OBR’s downward revision of 2025 GDP growth expectations from 2% in October to 1% now…owing to a mix of structural weakness in productivity and cyclical factors such as consumer confidence and higher rates…indeed the forecast path for the output gap was revised significantly with a trough of -0.5 in 2025 (chart below). By imposing such a stringent framework, Rachel Reeves has created a highly uncertain backdrop for the UK macroeconomy…with trade uncertainty and such limited fiscal space, the risk is one of constant speculation around imminent tax rises in coming months…and that’s with tax as a share of GDP already forecast to rise to 37.7%, a post-war high! Speaking to Ben Broadbent (former Deputy Governor of the BOE), a member of our Global Thought Leaders Program, he sees “risks to activity from fiscal policy are skewed to the downside, simply because the fiscal rules apply to the headline (and not the cyclically adjusted) deficit. So, if she’s constrained by those rules, and growth weakens for some other reason, depressing tax receipts relative to the OBR’s projections, fiscal policy has to be tightened.”. Whilst the market lacks confidence in growth and fiscal policy, Gilt yields in the 10y+ sector will struggle to come lower…and if indeed this all leads to a much weaker growth outcome, then the BOE will surely have to respond with an acceleration of cuts in the second half of this year (currently 50bps priced by Dec) . A further steepening of the 5s30s curve seems sensible.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Some Macro Thoughts - What We Do