-

Who We Are

- What We Do

Series: Macro ThoughtsBack to Fiscal

By Nohshad Shah

LONG-END YIELDS CAME BACK INTO FOCUS THIS WEEK with the combination of last Friday’s US sovereign downgrade and the passage of President Trump’s “Big, beautiful” bill through the US House of Representatives. Independent estimates suggest the bill would increase public debt by at least $3tn over the next decade and the debt-to-GDP ratio to 125% (from 98%) with annual deficits rising to around ~7%. Sobering stuff. As I’ve said in this note before, whilst markets in the post-GFC (2009-19) period were defined by monetary policy…since 2020, fiscal policy has been the dominant policy lever (including causing the surge in global inflation). This week served as a timely reminder that it continues to be in the driving seat. 30y Treasury yields hit 5.15% in response to the news and the broad-based dollar index (DXY) continues to weaken with another ~2% correction in the last week. Investors may be inclined to think that this is a repeat of the “sell US assets” theme seen in April following “liberation day”. I would beg to differ. For the past four weeks I have made the case in favour of the market’s re-rating of US economic growth higher, following a (market-enforced) de-escalation of the Trump Administration’s tariff agenda. In my mind, the risks are skewed towards more positive growth sentiment in markets. If the dollar continues to depreciate on US fiscal expansion, then this becomes a meaningful forward tailwind for growth as it offsets the “typical” drag you’d expect from higher bond yields…which in turn, increases the fiscal multiplier relative to previous episodes. Watch the right tail.

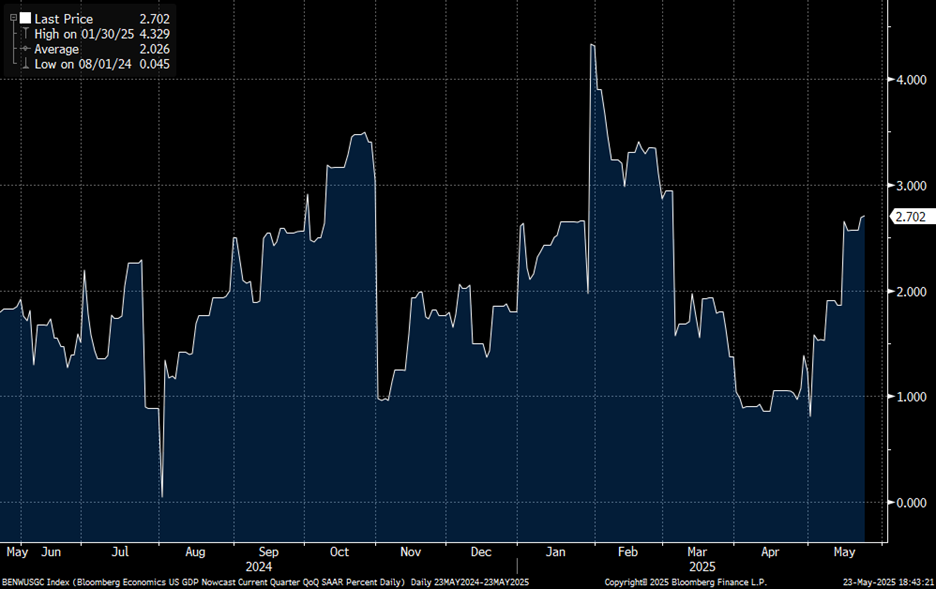

LET’S START BY LOOKING AT OUR FAVOURED BAROMETER, FCI (Financial Conditions Index). One might expect that, given the sell-off in bonds back towards the highs in yield, FCI would have tightened substantially…but if we look at the index (chart below), we observe that we remain at easy levels and certainly nowhere near the tights seen in early April. This is largely because of the performance of equity markets (SPX +17% from the lows), a weaker US dollar (DXY -3.7%) and tighter credit spreads (CDX IG 5Y -23bps). Tariffs of the magnitude originally planned were a big headwind for business investment and consumption…and the market (rightly) priced-in greater recession risk. But now those risks are broadly in the rear-view mirror (EU headlines notwithstanding – feels like a classic “Art of the deal” head fake), the forward-looking outlook for nominal growth looks solid. And this will only be further enhanced by the positive fiscal impulse from the tax bill. The riposte will be…what about bond yields? A high growth / high inflationary world driven by expansionary fiscal policy is not one where you want to own long-dated bonds. But what’s become clear in recent years is that the US economy can handle structurally higher yield levels…10y yields have been in the 4-5% range for much of the past two and half years, whilst real GDP has been 2-3.2% YoY over the same horizon. So…whilst I would still argue that a disorderly sell-off in rates can be harmful, investors should realise that higher yields are here to stay and are a natural consequence of the policy backdrop. Following on from last week’s data, this week saw PMIs coming in stronger than expected with the US composite at 52.1 (exp: 50.3)…reflecting the fact that the soft data is continuing to turn more positive moving on from the tariff-induced shock. Ultimately, these diffusion indices represent the sentiment of consumers and businesses, and one would expect them to continue to move in a positive direction as the forward-looking outlook improves further. For the Fed, this means that they are even less likely to cut policy rates anytime soon: above-target inflation with risks to the upside from moderate tariffs…GDP growth that is tracking towards 3% (chart below)… a labour market that remains close to full employment…and impending fiscal expansion…does not reflect an economy that warrants rate cuts. Indeed, if the tide turns further, then an economy running too hot may quickly become more of an issue than a recession.

US Financial Conditions Index

Source: Bloomberg, 23may25

Bloomberg US GDP Nowcast

Source: Bloomberg, 23may25

DIGGING DEEPER INTO FISCAL…House Republicans passed the multi-trillion-dollar tax bill with a 215-214 vote. The “Big, beautiful” bill now heads to the Senate, which will have the chance to make its own provisions. The Committee for a Responsible Federal Budget noted that the bill would add $3tn to the debt over the next decade, but that if certain provisions were made permanent, this could rise to $5tn. Interestingly, having passed in the House by a whisker, my sense is that the Senate, where the GOP has a stronger majority, is likely to add further to spending, if anything – so in effect, the current spending becomes the floor, not the ceiling. This week we hosted a client call with Patrick McHenry, former Chairman of the House Financial Services Committee, which clarified a few things…namely that President Trump’s influence over Congressional Republicans remains extremely firm…and that his electability is ultimately derived from economic prosperity. In summary: do not underestimate the importance of these tax cuts to President Trump – it is the cornerstone of his domestic policy agenda…bond market vigilantes be damned, don’t expect any compromise. This is an important point, because unlike tariffs, I cannot see POTUS course-correcting on tax cuts, which some in the market have come to expect. Chairman McHenry relayed that the focus in the Administration remains squarely on landing tariff deals by early Fall…the tax deal in the summer…and a crypto bill around the same time…thereby releasing pent up economic growth, just in time for delivering some of the more contentious parts of the agenda ahead of the mid-terms. We shall see. As Mike Tyson says, “everyone’s got a plan…”

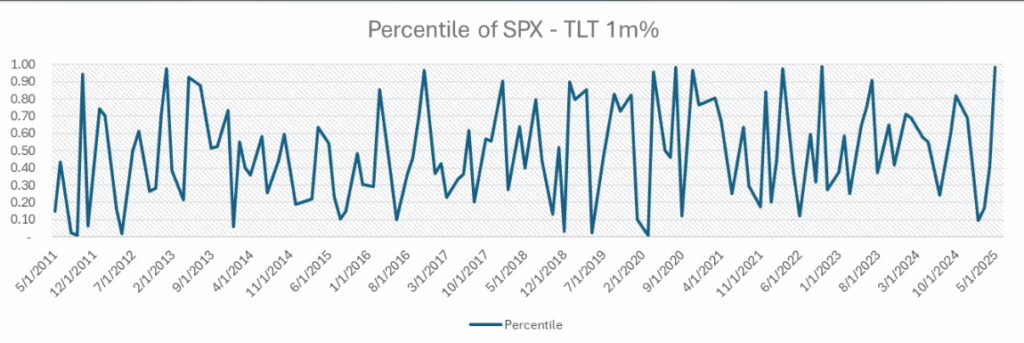

Relative index performance of equities versus rates (1m horizon)

Source: Bloomberg, 23may25

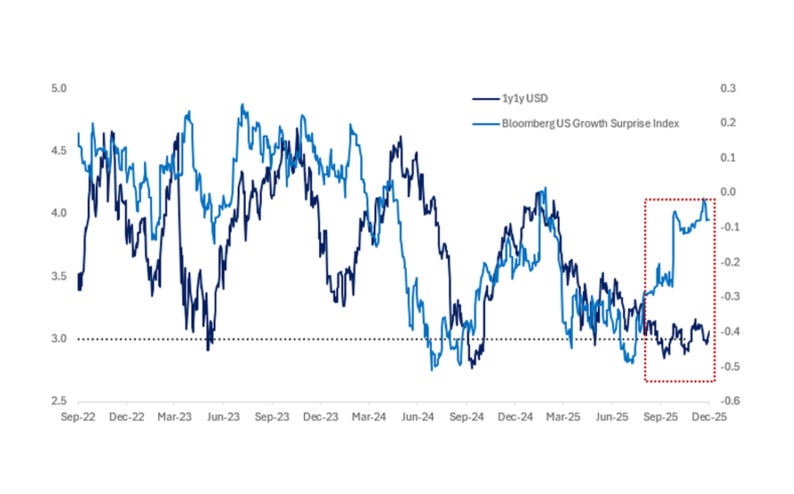

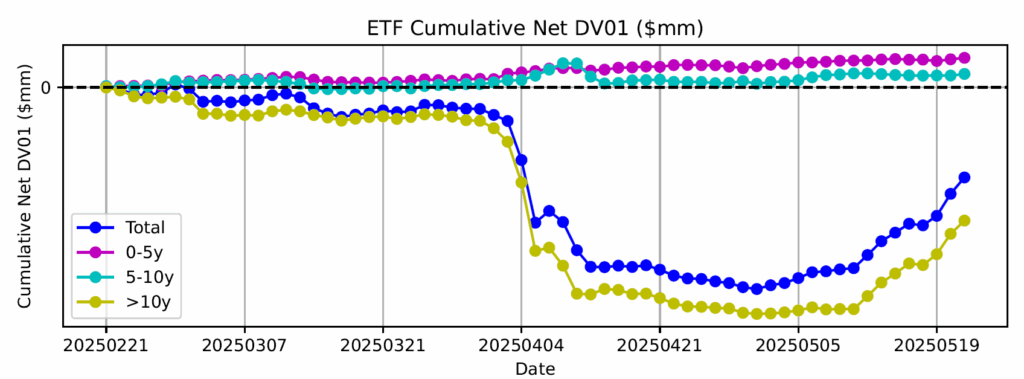

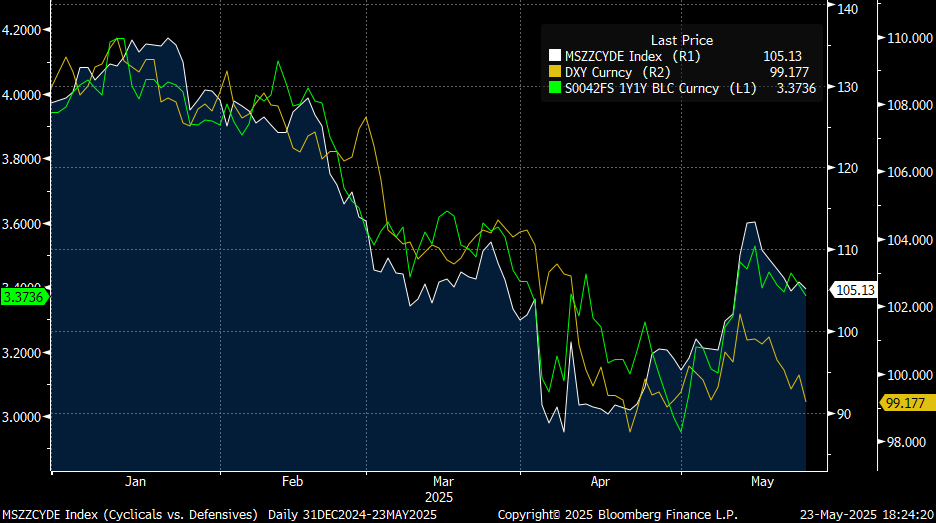

WHAT DOES IT MEAN FOR ASSET PRICES? Higher nominal growth, elevated inflation and increased issuance from further fiscal expansion is not good for bonds. Whilst the weak 20y auction this week was telling – especially barbelled by the downgrade and budget news – my sense is, however, that a lot of the negative sentiment is already in the price. Locally, I can see yields stabilize especially with 2y, 5y and 7y auctions coming up next week, sectors which should garner more meaningful demand. Moreover, the recent strong equity market performance, relative to fixed income, should lead to re-balancing flows at month-end from ALM investors – the chart above (h/t: Ivo Stefanov) suggests the depth of relative performance on a 1m trailing basis is significant. Indeed, looking at Citadel Securities market-leading internal flow data (chart below; h/t: Liang Wu), we see a meaningful increase in buying activity in fixed income ETFs (having troughed in April)…with more room to go. Another interesting aspect going forward will be potential demand from foreign investors, given the weakness in the US dollar. The sustained weakness in DXY means that US equities are now much cheaper on an unhedged basis. For those that subscribe to the pro-growth narrative, SPX is now ~7% cheaper in GBP terms and ~9% cheaper in EUR terms…a meaningful pick-up. When looking through a growth lens, the dollar looks out-of-whack with other proxies such 1y1y forward swaps and cyclicals vs defensives (chart below). I would expect this to revert, should the market go back to trading rate differentials, the more traditional valuation metric for FX. Indeed, when looking at the Eurozone backdrop, whilst I don’t expect anywhere near 50% tariffs to be implemented, policymakers in Europe seem complacent about their ability to land an agreement in the same way that China has. Further bad news on this front would be detrimental to an already shaky Eurozone economy, adding weight to the case for further ECB cuts, beyond the circa two 25bp cuts priced by year-end. This is a risk for popular EURUSD longs.

Source: CitSec Internal Data, 23may25

Cyclicals vs Defensives, USD 1y1y Swap, DXY

Source: Bloomberg, 23may25

S&P 500 ETF in USD, EUR and GBP terms

Source: Bloomberg, 23may25

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Macro Thoughts - What We Do