-

Who We Are

- What We Do

Series: Macro ThoughtsCourse Correct

By Nohshad Shah

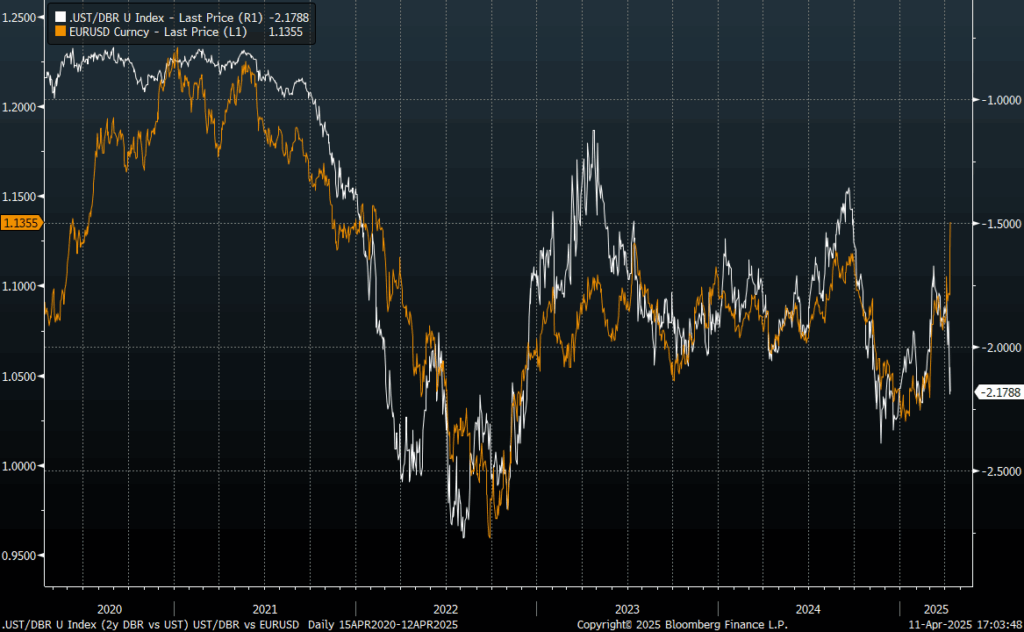

THE MARKET IS THE GREATEST SELF-CORRECTING MECHANISM IN THE WORLD…and so it proved to be with President Trump’s trade policies this week. Following four tumultuous trading sessions after “Liberation Day – 2 April” with SPX selling off ~13% pretty much in a straight line, Trump was obliged to pivot into a 90-day “pause” for tariff implementation…ex China. Whilst on the surface this provided some relief, the reality is that the ratcheting up of China tariffs (currently ~145% all in), leaves the effective tariff rate for the US economy at 27% (Yale Budget Lab)…pretty much the same as where it was prior to the 9 April announcement and the highest that we’ve seen since 1903. These levels are way beyond what any forecasters had imagined and entirely uneconomical…be in no doubt, until these tariff rates come down, the US is in an effective trade embargo with China. As mentioned in my previous notes, an America First agenda that incorporates a retrenchment of the United States from the world, both economically and geopolitically, cannot be good for the value of the US dollar, nor for US assets more broadly…and this is what we’ve seen play out with a continued selloff across USD fx, rates and equities remaining jittery. Effectively, this is a re-rating of the foreign sponsorship of US assets…with investors of all stripes liquidating or sharply reducing their exposure. This has been most acute in US Treasuries where 10y yields have sold off ~50bps and swap spreads widened ~15bps to the widest levels seen in a decade. These moves are a perfectly logical consequence of the current Administration’s desire to eliminate the US trade deficit…if you reduce the trade surplus of foreign countries, there are simply less dollars that need to be recycled, typically into USTs. Moreover, the economic consequences of these trade policies are likely to lead to deterioration in growth…which may well lead to further fiscal expansion down the line… and finally, you have the inflationary impulse. In sum, this implies a rates curve that should naturally exhibit more term premium…higher yields…wider swap spreads…and a currency that looks much less like a reserve one. For some time, I have argued that the clearest trade throughout has been a weakening of the US dollar…this remains the case…and can be seen most clearly in the decoupling of EURUSD from the rate differential of the two currencies (chart below).

EURUSD & 2Y DBR-UST Yield differential

Source: Bloomberg, 11apr25

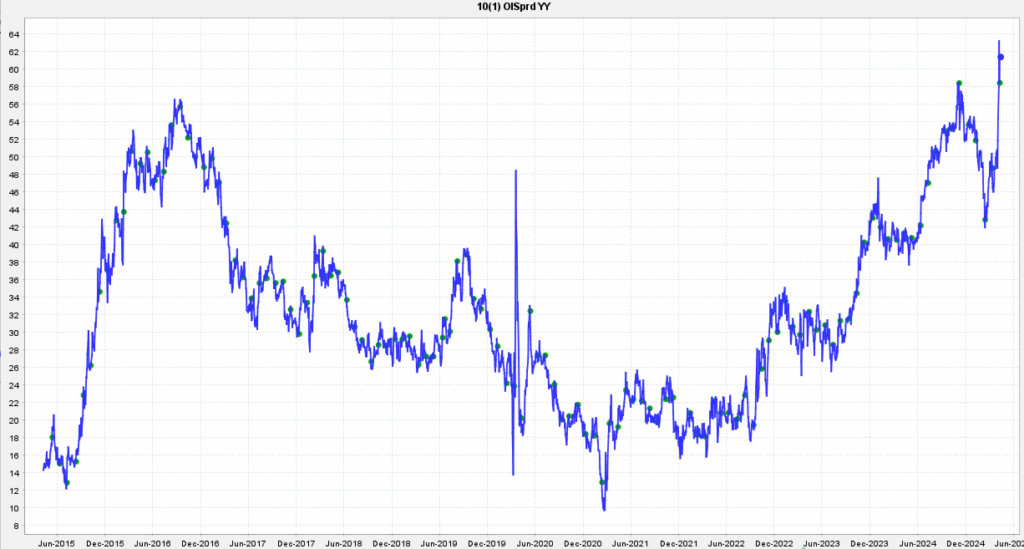

10Y UST vs OIS Spread

Source: RiskVal, 11apr25

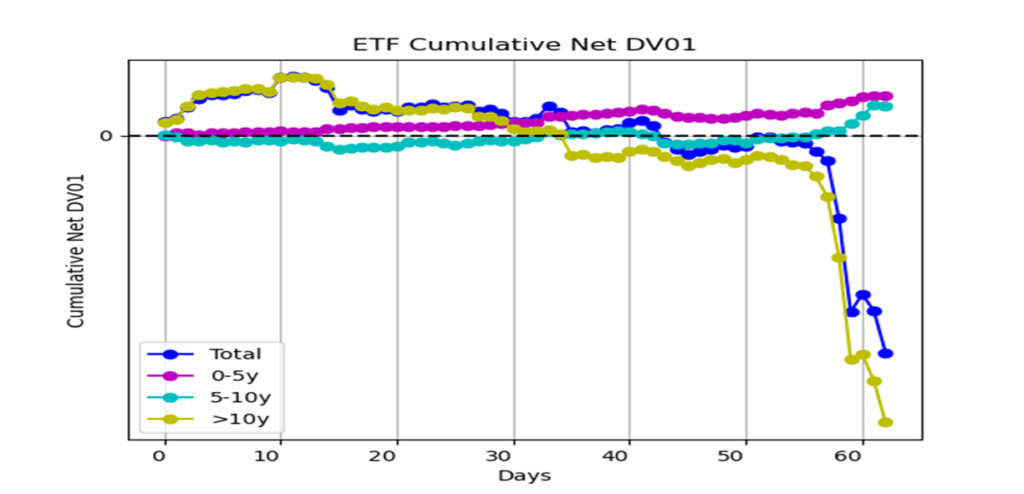

Cumulative US Rates ETF Flows

Source: Citadel Securities, 11apr25

WHAT ARE THE BROADER ECONOMIC RAMIFICATIONS OF A RE-ORDERING OF GLOBAL TRADE? Globalization, in its simplest form, creates country-based specialization in the production of global goods and services, based on comparative advantage. The US has been one of the primary beneficiaries of this, creating a productivity boom which has improved living standards for the majority of Americans (as well as many other countries). The current account deficit is funded by a capital account surplus, which means that international capital flows into US assets support the US dollar reserve status, becoming a key driver of US exceptionalism. A further benefit of being the world’s reserve currency has meant that in a globalized system, the US has been able to finance its twin deficits (budget + current account) at extremely attractive levels. This is now at risk. Tariffs are a stagflationary supply-side shock. If more goods are to be produced domestically, this will lead to a less efficient allocation of capital and labour, resulting in lower productivity, lower trend growth and higher inflation. Put simply, if Nike sneakers are to be fully manufactured in the US, where real wages and costs of production are higher than elsewhere…this leads to a price level shift from tariffs, but also persistent inflation as a function of lost productivity (for a given level of growth). The market has not yet grasped these medium-term implications…sure, there’s an appreciation of heightened uncertainty…with a one-off price shock…followed by demand destruction and a recession, which will ultimately be met with a combination of monetary and fiscal policy measures that save the day. I’m less convinced, especially if we are truly facing a re-ordering of global trade and there isn’t a dramatic u-turn in the levels of these tariffs. In many ways, the risk scenario is what happened in the UK…a self-inflicted supply-side shock (Brexit), that has damaged productivity and lowered trend growth…leading to a prolonged stagflationary impulse with dramatically reduced fiscal space.

Source: Citadel Securities, 10apr25

AS FOR TARIFF NEGOTIATIONS…there seems to be something of a stalemate with China’s latest raising of retaliatory tariffs to 125% on US goods, but with the caveat that further rises from the US would be ignored because “given that at the current tariff level, there is no market acceptance for US goods exported to China”. In my mind, this perhaps represents an off-ramp for President Trump to reach a deal in coming weeks…whether he will take it or not, is another matter. Ultimately, a full-blown trade war with China is not good for anyone…the US certainly has the stronger hand…but I would not underestimate the tools that China can deploy (c.f. the move in CNH), nor its ability to be long-term and strategic in their approach….especially compared to the more short-term nature of the US political cycle. This was on display in asset price moves this week. My expectation is that coming weeks will see trade deals taking place, starting with close allies…and despite the complications around non-tariff barriers, VAT and other aspects, timelines need to be accelerated given the magnitude of economic disruptions. As mentioned in previous notes, my belief remains that the Administration’s tax cut agenda will soon come to the fore…as soon as we have some stability in trade discussions, the conversation will quickly move to the revenue raised from tariffs and the magnitude of tax cuts they can pay for. Indeed, one could argue one of the primary reasons for Trump’s pivot this week was driven by the need to ensure unity amongst Congressional Republicans, crucial to the budget reconciliation process.

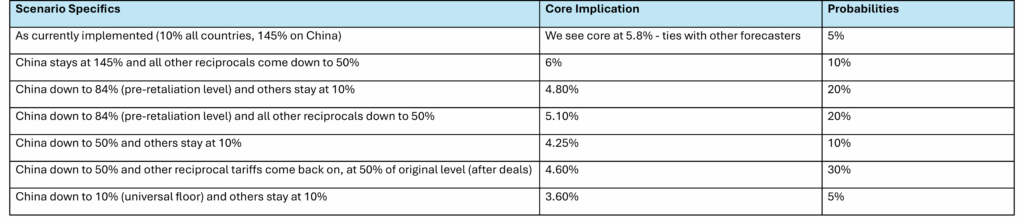

WHAT ABOUT POLICY? The Fed is in a tricky spot. What they (and most in the market) considered to be a maximalist approach to the tariff agenda (10% across the board and ~20% China) has now become the floor. As highlighted in the above table (h/t Durham Abric), in most tariff scenarios inflation is heading substantially higher with Core PCE > 4%…which is 2% above target. And yet, the hit to growth will be large with estimates in the -1% range for 2025 (Q4-Q4) with much uncertainty around the magnitude. Tariffs are a stagflationary shock, so will challenge both sides of the FOMC’s dual mandate…so it’s natural for them to be cautious about their next move. Despite survey-based measures of inflation expectations being elevated, more importantly for the Fed, market-based 10y breakevens are calm at ~2.20%…and indeed have dropped from ~2.50% in Feb. Could this provide cover for the Fed to cut rates? Possibly…but I would expect that to happen only once the hard data indicate a forceful slowdown that unequivocally throws the employment side of their mandate into distress and some confirmation that trade-policy induced inflation shocks are indeed temporary. Ultimately, Chair Powell will not want to respond to policy-induced market stress with expansionary monetary policy when inflation is so elevated. Central Bank independence exists to make the tough decisions, without recourse to politics. And as the FOMC’s Austan Goolsbee highlighted at this week’s ECNY lunch…in almost every country where there’s political interference in monetary policy, the outcomes around growth, inflation and employment are substantively worse. Where I can see policymakers act is in Treasuries, where markets are at-risk of disorderly moves…clearly a continued sell-off in long-end yields is highly disruptive and it’s paramount to maintain liquidity in the world’s “risk-free” rate…and we know Secretary Bessent has a heightened focus on long-end yields and their impact on financial conditions. As such, if liquidity conditions become more constrained in the coming weeks, I wouldn’t be surprised to see an intervention…whether that be in the form of term repo…changes in SLR…or some form of emergency facility (as used by the BOE during the “Truss crisis”) that allows officials to calm the market. In terms of monetary policy, the Fed is a bystander here…they are not operating on the same timelines as the market…they will likely wait for tariff negotiations to play out and assess the true economic implications before acting. The bar for policy rate cuts remains high.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Market Insights - What We Do