-

Who We Are

- What We Do

Series: Macro ThoughtsCuts on the Table, Despite the Outlook

By Nohshad Shah

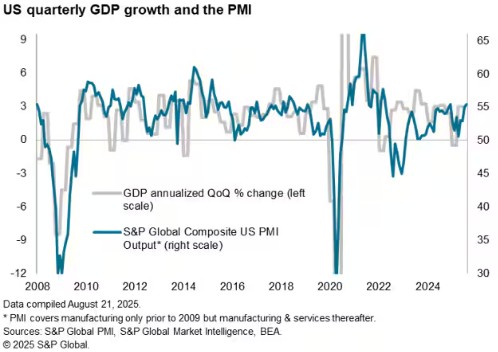

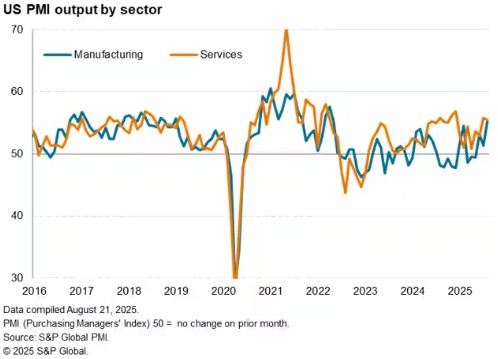

THIS WEEK’S DATA BROUGHT MORE EVIDENCE THAT THE FORWARD TRAJECTORY FOR US GROWTH IS POSITIVE AND INFLATION REMAINS CONCERNING. Flash PMI data for August came in stronger than expectations across the board with the Composite number at 55.4, an 8-month high reflecting a sustained reversal of the 5.4pts dip in April around liberation day. Along with last week’s robust retail sales data, this suggests a strong start to Q3 for businesses with the last two months seeing the strongest back-to-back expansions since 2022 according to this time series (chart below). Looking in greater detail, the continued service sector expansion (55.4) is now allied with a sharp rise in output growth in manufacturing to the fastest levels since May 2022 (53.3) with both new order inflows in goods rising (domestic demand) as well as exports (largest rise in 15 months). Moreover, the employment category rose for a sixth month in a row and there are increasing signs that companies are passing through tariff-induced price increases to customers as their pricing power is bolstered by strong demand. Though PMI data is imperfect, it is consistent with most high-frequency trackers for GDP which suggest growth remains robust and is recovering well from the April confidence shock…Dallas Fed WEI (2.5%), Atlanta Fed GDP Now (2.3%) and NY Fed Nowcast (2.1%). On the inflation side the landscape continues to get worse…Walmart, the nation’s largest retailer, said on its quarterly earnings call that tariffs are starting to bite: “As we replenish inventory at post-tariff price levels, we’ve continued to see our costs increase each week, which we expect will continue into the third and fourth quarters” with CEO Doug McMillon warning that prices will rise this summer to offset tariff-driven cost pressures on goods imported to the US. Whilst demand remained solid, margins for the company shrunk as inventory costs rose materially leading to their first earnings miss in over 3 years…I think we all know what happens next. Gamers also took a hit…Sony announced an abrupt $50 price increase for their PS5 consoles…an 11% increase in the RRP likely driven by increased costs. Similarly, Apple raised their streaming subscription price 30% to $12.99/month from $9.99. In my mind, the picture this paints is one of solid economic growth and consumer demand, with retailers – even those with substantial pricing power – choosing to increase prices as inventory depletion runs its course. Inventory accumulation was always going to distort the passthrough, but now it’s running out and tariffs have not gone lower. The important point here is that most of these companies could continue to swallow cost increases for longer…but they’re deciding not to because they feel their customers can handle it. That is very revealing.

AGAINST THIS BACKDROP CHAIR POWELL’S JACKSON HOLE SPEECH REVEALED THE FED’S PREFERENCE FOR RATE CUTS: “In the near term, risks to inflation are tilted to the upside, and risks to employment to the downside—a challenging situation. When our goals are in tension like this, our framework calls for us to balance both sides of our dual mandate. Our policy rate is now 100 basis points closer to neutral than it was a year ago, and the stability of the unemployment rate and other labor market measures allows us to proceed carefully as we consider changes to our policy stance. Nonetheless, with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance”. The labour market is certainly weaker than previously thought post the recent NFP report (including revisions)…but the important question is whether falling job creation is coming from reduced labour demand or labour supply. As mentioned in this note before, President Trump’s immigration policies have sharply curtailed net migration this year and will continue to do so in the near future…with the corresponding supply shock to the labour force resulting in a breakeven level of payrolls growth ~50k or lower. As Powell re-iterated, this means the unemployment rate becomes all-important as the only measure to consider both sides of the ledger. I agree with his remarks about the “curious” balance in the labour market…essentially a low hiring / low firing one…but my view is that the softening in supply is the more dominant factor. Moreover, when you consider income proxies (AHE x total jobs x hours worked) at 5.2%, consumer spending PCE at 2.6%, and healthy household balance sheets, personal earnings growth should remain well supported and ensure there is no persistent weakness in real household consumption. Regardless, Powell has now opened the door to rate cuts and with continued pressure from President Trump to lower rates, it’s more likely than not that the FOMC lowers policy rates in September…call it “insurance cuts” against the risk of rising unemployment in coming months. I doubt they would cut by 50bps like last year – at that time, the u/e rate was rising fast and sequential inflation was coming in lower than their forecast – categorically not the backdrop we currently have. Instead, the forward outlook remains strong…FCI is the easiest it’s been in 3 years…the unemployment rate is 4.2% with Initial Claims running at a 4wk avg. of 226k…composite PMI over 55…an 11% depreciation of the USD index…a Q2 earnings round which saw 81% of the S&P 500 beating estimates with 11.8% YoY earnings growth amidst a once-in-a-generation AI investment boom…and forward fiscal stimulus incoming of ~1% of GDP with likely some tariff dividend cheques thrown into the mix. If trend growth is ~1.5% these days, then these factors plus “risk-management” rate cuts mean the economy will be running HOT in coming quarters…just what POTUS wants.

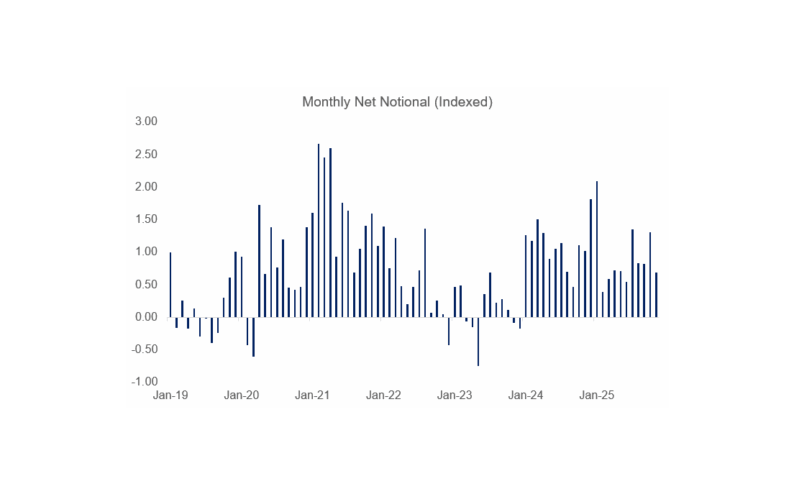

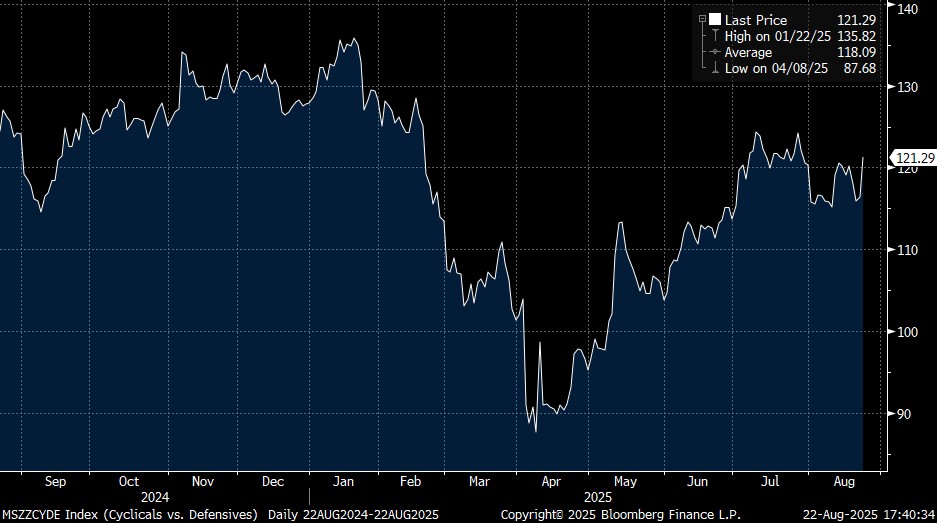

US Cyclicals vs Defensives

Source: Bloomberg, 22aug25

THIS IS EXACTLY THE OUTLOOK THAT MATTERS FOR ASSET PRICES…remember markets trade the forward outlook, not the spot. Injecting BOTH monetary and fiscal policy stimulus outside of a recession with pre-existing easy financial conditions is a VERY supportive environment for equities…and my favourite cyclicals v defensives measure performed strongly +5% reflecting the upgrade to the growth factor following Powell’s speech (albeit after a mid-week correction). The same is true for bitcoin and other growth/liquidity-driven assets. The US dollar will continue to weaken…whilst prior depreciation was likely driven by foreign hedging flows or anti US exceptionalism, the ongoing pressures stem from a (now) dovish monetary policy outlook in an environment of above-target inflation and political pressure on the independence of the central bank. As I’ve written about before, this is not just about who is Chair of the Federal Reserve, but broader control of the entire FOMC and this lever of policymaking by central government. Whilst this may be rapidly becoming the new reality, investors in bond and FX markets will be watching developments closely and I doubt the unwind of a core tenet of global markets for the last fifty years will conclude without volatility. Yield curves should continue to steepen…with more dovish policy pinning 2y rates and 10y+ yields remaining vulnerable to moves higher as the inflation story unfolds. This year’s just getting started…

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Market Insights - What We Do