-

Who We Are

- What We Do

Series: Macro ThoughtsDo Not Bet Against the US Economy

By Nohshad Shah

FOR MANY YEARS WHEN NEW GRADUATES STARTED ON THE TRADING FLOOR…I would stick a post-it note on the edge of their screens with the following words in bold type: “DO NOT BET AGAINST THE US ECONOMY”. Investors would be well served to remember this phrase, which has gone from a pithy motto to a core tenet of global macro investing. Time and again, market participants get excited at the prospect of a weak US economy, seeking out black swans that do not exist and betting on deeper imminent rate cuts from the Fed as a result. This week, the economic data confounded these expectations yet again with a strong employment report reflecting a labour market in solid health. Not only did Nonfarm payrolls significantly beat expectations (147k vs 106k), but more importantly the unemployment rate declined to 4.1%, suggesting even a tightening path for the labour market going forward (more on this below). The summer 2024 playbook that some have been anticipating…of weakness in the labour market allowing for a window for the Fed to cut rates…is derailing rapidly. Instead, financial conditions continue to ease with a heady mix of weaker USD FX, stable 10y Treasury yields and rising risk assets. Spot growth is fine with no material softening in the labour market, whilst we await the impact of tariffs on the inflation data. But, even if inflation is elevated, we are still far from levels which would warrant rate hikes. Furthermore, with an incoming large positive fiscal impulse to boot, this leaves the forward outlook for growth on an especially strong footing. The rally in risk assets has room to run.

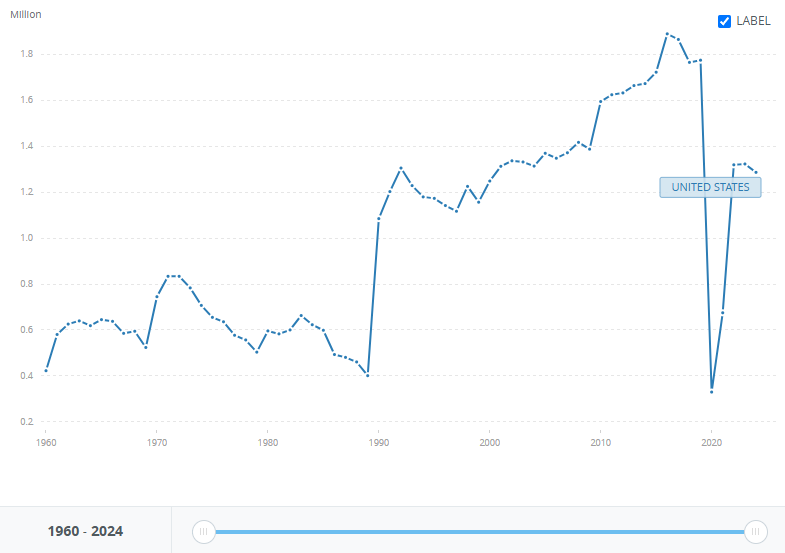

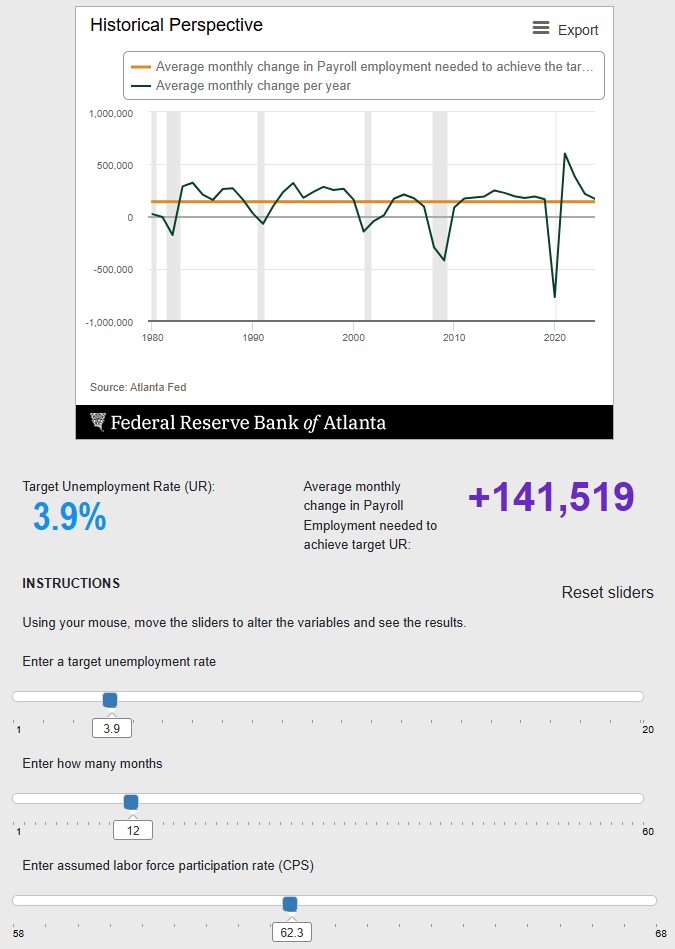

WHILST THERE HAS BEEN MUCH DISCUSSION ABOUT TARIFFS AND FISCAL…arguably an equally important policy priority has been overlooked – immigration. In recent months, President Trump has embarked upon an unprecedent crackdown on illegal immigration and created new entry barriers for certain legal immigrant constituencies, which will have profound implications for the US labour market. The combination of increased arrests and deportations, enhanced border enforcement, policies designed to reduce access to the asylum system, and a reduction of other legal forms of migration such as student visas and country bans will all serve to reduce net migration. An important study by the American Enterprise Institute (AEI) estimates that net migration could turn negative for 2025 with a predicted range of −525,000 to 115,000…that’s compared to post covid levels in 2022-24 of around +1.3 million (chart below). This will have a significant impact on labour supply, which puts the Fed in a tricky spot…when assessing the health of the economy, the payroll figures need to be understood within the context of a shrinkage in the labour force. Whilst in the medium-term this will also have negative implications for economic growth, the short-term focus is on understanding the level of payroll growth commensurate with an economy operating at full employment…AEI estimate the breakeven rate of monthly job creation (the rate that keeps the U-rate constant) could be as low as 10-40k per month by the second half of 2025, down from 140-180k in 2024. Even if we conservatively assume that the breakeven rate of job growth is in the 50-100k range, this week’s 147k should be considered a hot number, because any print above the breakeven reflects a tightening impulse on the labour market. This runs contrary to the narrative in economists’ circles of a softening labour market (a mistake that was made in 2024 as well). The market is conditioned to focus on measures of labour demand in assessing the labour market trajectory, but it is imperative to assess labour demand relative to labour supply given the later has become significantly more volatile in recent years. The bottom line is that the decline in the unemployment rate itself (which reflects both demand and supply of labour) leaves me with the view that we are nowhere near levels that would concern the Fed. Indeed, if we use the Atlanta Fed’s Jobs Calculator, further NFP prints above 141k (with constant labour force participation) could signal a move towards 3.9% in the U-rate (see below)…food for thought for Chair Powell and the FOMC (regardless of whether the jobs are private or public sector). Even this week’s JOLTS survey showed a rise in job openings reaching 7.769mln, exceeding market expectations and the highest since November 2024, with Quits and other aspects of the report remaining steady. In sum, the unemployment rate has stabilised in the 4.0-4.2% range for the last year signalling a labour market that remains resilient in the face of elevated levels of policy-induced uncertainty in recent months. The flexibility of the labour market has always been one of the core strengths of the US economy…and it remains the case for now. Despite immense pressure to cut policy rates, the Fed has no reason to do so at this stage…front-end market pricing reacted to this week’s data taking down the probability of a rate cut in July to 5%. The dominos are falling one by one…and I would expect September meeting pricing (18bps priced) to do the same as we continue to see the outlook improve over the summer.

Net Migration – United States

Source: World Bank

Source: Federal Reserve Bank of Atlanta

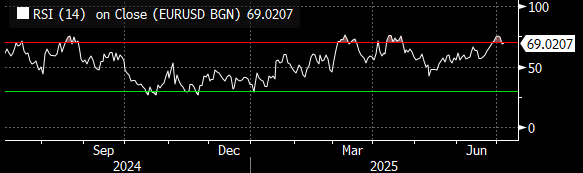

PERSISTENT WEAKNESS IN THE US DOLLAR…has been a consistent theme with a sizeable ~12% depreciation in DXY since the beginning of the year. A confluence of factors have contributed to this move, most notably hedging of USD exposure, diversification of assets out of US into Europe, and recently, expectations of a more dovish Fed with data weakness. At this juncture, my sense is that we are reaching levels where this move is likely to stall…we are now firmly beyond peak policy uncertainty (April-May), which was a clear accelerant in the move. Indeed, when looking at fund flows – inflows into Europe ETFs peaked in the Mar-Apr period and similarly, April marked the lows for allocation into US equity ETFs (FFLO on BBG), suggesting a normalisation of flows as investors achieve greater clarity on President Trump’s tariff agenda. Relatedly, the economic data continues to improve in the US relative to Europe, making it less attractive to play for further Eurozone growth. Indeed, the ~15% appreciation in EURUSD we have seen this year will serve as a material deflationary input for the European economy, impacting the competitiveness of the export sector. If we approach ~1.20, the ECB will have no other option than to start factoring this into their policy narrative…likely leading to a further dovish tilt (not unwarranted given recent weakness in data)…especially given their forecasts assume EURUSD below spot levels over the forecast horizon, meaning there is a mark-to-market upcoming when they refresh their inflation forecasts in September. Moreover, whilst it’s difficult to ascertain high quality positioning data in FX, anecdotally short USD has become the trade du jour for the FX community and technical indicators such as the 14d EURUSD RSI at 69 suggest the dollar is oversold (chart below). Whilst I’m not suggesting an aggressive turn in the dollar, the reasons for a continued depreciation are withering and if I’m correct on my bullish outlook for US growth, US dominance in global assets could re-assert itself rapidly and the dollar could be the next shoe to drop…especially if portfolio hedging flows start to slow.

Source: Bloomberg, 04jul25

PRESIDENT TRUMP’S “BIG, BEAUTIFUL BILL”…was approved by Congress just prior to his self-imposed Independence Day deadline. The bill’s successful passage reflects a consolidation of his political power over the GOP for what is the mainstay of his domestic political agenda. As reflected in this note even during May’s bond market wobbles, Trump was never going to allow anyone, or anything derail this piece of legislation. So…the fiscal profligacy of the US continues unabated and despite adding $3.4tn to the federal deficit through 2034, bond market vigilantes have been MIA (did they all migrate to the UK??). The annual deficit is now likely to rise to 9% of GDP (from ~6% currently) by 2035 and the Debt/GDP ratio to over 120%…levels which should concern any sensible investor. This week’s sell-off in UK Gilts serves as a warning of what happens when investors lose confidence in a country’s fiscal prudence…PM Keir Starmer’s welfare reform bill, which was mooted to save £5bn from the budget, had to be gutted following a rebellion from within his own Parliamentary Labour Party along with rumours (now debunked) of the Chancellor’s resignation. Bond markets reacted sharply with 30y Gilt yields rising over 20bps intraday. The UK government is left with only two choices for this Autumn’s budget – find cost savings elsewhere (unpopular with the public) or raise taxes again (bad for growth). The third option to abandon the Chancellor’s self-imposed fiscal rules is no longer available following the Lizz Truss crisis of 2022 – which is the primary lesson here: like one’s reputation, it takes decades to build trust…but it can be lost very quickly…and once gone, is extremely difficult to recover. These days, investors have little confidence in long-end Gilts, meaning that any government will struggle to manoeuvre beyond these constraints.

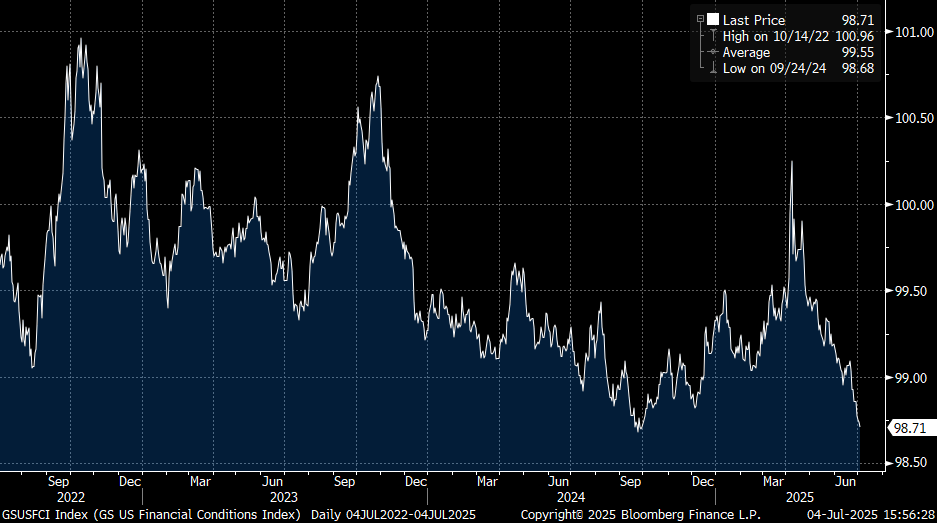

WHILST US BOND MARKETS REMAIN SANGUINE; EQUITY MARKETS ARE EBULLIENT – stocks continue to make new all-time highs as the forward outlook for growth continues to brighten. FCI is the loosest in 3 years (chart below) providing a flashing green signal for risk assets to rally further in what has been one of the most unloved rallies in recent memory. Whilst ballooning the deficit over the 10yr horizon, the fiscal bill will provide a front-loaded boost to GDP of +0.9% in 2026…likely designed for peak impact ahead of the midterms. As oft stated in this note, fiscal policy has been the dominant driver of macro markets in recent years following the end of the QE era. Do not underestimate the magnitude of this fiscal impulse to drive animal spirits in a US economy that is already on solid footing. Add into the mix an AI investment boom (with results still pending) and even some potential for easier Fed policy (whether from this Chair or the next)…and we could be in for an almighty surge in equities. From our market leading equities franchise, my colleague Scott Rubner notes that net notional buy skew has been higher for 11 out of the past 13 weeks amongst retail clients, with this week being the largest buy imbalance in dollar terms for 9 weeks => no signs of a slowdown in retail buying, despite record levels. On the other hand, institutional participation has remained muted…BUT as the macro picture continues to improve, vol comes down (both spot and vol control lookback windows) and the trend continues to assert itself (driving CTA buying)…institutions will increasingly be forced into the market.

US Financial Conditions Index

Source: Bloomberg, 04jul25

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Market Insights - What We Do