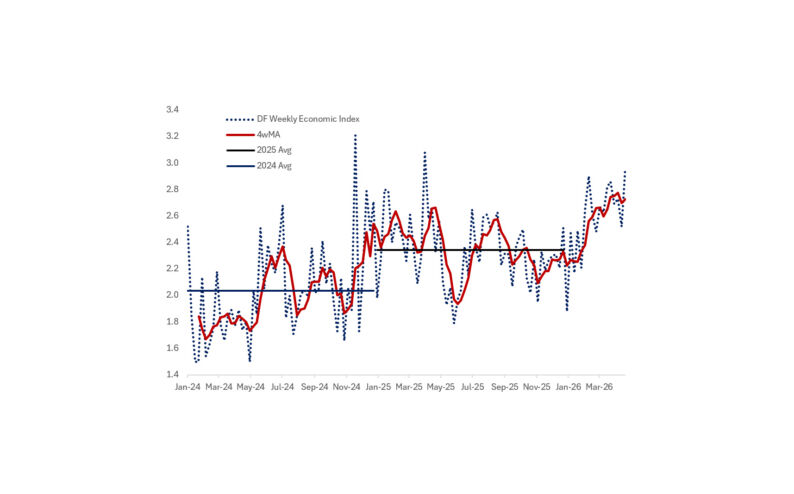

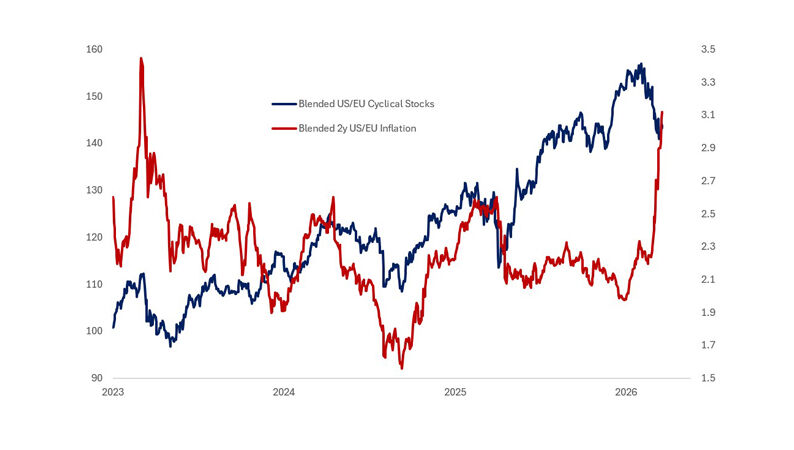

FIXED INCOME MARKETS ARE WAKING UP TO THE REALITY THAT EQUITIES HAVE BEEN PRICING FOR SOME TIME…namely, “more growth, more inflation” as per my last note. Since early April, as investors became comfortable that the second derivative stress impulse of the Iran conflict was no longer worsening, and that the worst-case tail scenario was unlikely to materialise, FCI has eased all the way back to multi-year lows led by a buoyant stock market focused on a once-in-a-generation AI transformation. Accordingly, US growth dynamics look healthy – my favoured high-frequency tracker the Dallas Fed’s WEI is at 3% scaled to Q4 GDP growth. Indeed, our own factor-based growth model implies elevated market pricing for US growth to the tune of +2 std dev (chart below). This makes sense…with the backdrop of a huge AI capex boom ($750bn in 2026), robust corporate earnings (NVIDIA capped off what was pretty much a blowout Q1 reporting season: 28.4% YoY earnings growth; highest since Q4’21) and policy stimulus. However, this signal has been inconsistent with the monetary policy factor in our model, which has remained close to neutral in the 0-0.5 std dev range. In essence, this implies that the Fed outlook has been behind the curve, relative to fundamentals. Following this month’s FOMC meeting, the market has rightly started to correct investors’ long-held dovish mindset predicated on the assumption that any Fed Chair nominated by President Trump will immediately cut rates. This has been the dominant view amongst many in the macro community ever since the Fed Chair discussion came into view…and something I have been pushing against consistently. Moreover, persistent fears about the health of the labour market have proven to be unfounded. US economic fundamentals have (yet again) proven their resiliency…inflation not the labour market is the greater risk. Front-end policy pricing for 2026 has gone from 60bps of rate cuts to 25bps of rate hikes in recent weeks reflecting a rates market that is awakening to the reality of a hot economy with risks of a classic demand-induced inflation process…but crucially, with a much higher starting point for core inflation…and supply side shocks that may prove persistent. So, the market reaction we have seen is appropriate…first, equity markets rallied following the easing of war dynamics and re-assertion of the AI story…then bond yields have risen to reflect a more hawkish policy factor, logical given the underlying fundamentals. The Fed should take note and adjust their stance soon, lest they get behind the curve.

Source: Citadel Securities

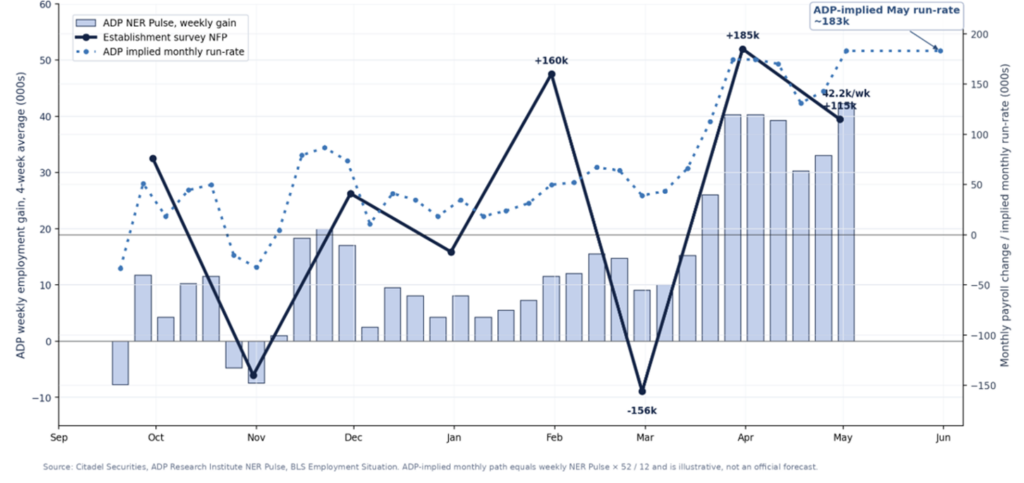

CHAIR WARSH WILL NEED TO NAVIGATE AN AWKWARD FACT PATTERN AT HIS FIRST MEETING…where participants are likely to meaningfully upgrade their inflation forecasts in response to the ongoing energy shock. The challenge is that the inflation impulse no longer looks confined to headline energy…April PPI showed final-demand prices up 1.4% m/m and 6.0% y/y, with clear upstream pressure from energy, transportation, and intermediate goods, including gasoline, diesel, crude petroleum, truck freight, steel, lumber, and industrial chemicals. ISM survey data also point to broadening input-cost pressure, with the manufacturing prices index at 84.6 and the services prices index at 70.7, the latter tied for its highest reading since October 2022. Consumer expectations are moving in the wrong direction as well, with the New York Fed’s Survey of Consumer Expectations showing one-year-ahead inflation expectations rising to 3.6% in April (from 3.4% in March), even as medium and longer-term expectations remained more stable. In sum, these data point to faster passthrough and a broader risk that the energy shock is becoming embedded in near-term price-setting behavior. Policymakers have simply been too optimistic about the intermediate trend in inflation…and this is not only about supply shocks; inflation remains significantly about target in numerous categories, especially services. Against this backdrop, the FOMC is likely to force a change in the statement language, shifting from an easing bias to an explicitly neutral bias. The influential Governor Waller alluded to the same in his speech on Friday. That would be consistent with the signal from the minutes, which suggested that a majority saw “some policy firming” as likely to become appropriate if inflation continued to run persistently above 2%, while “many” participants would have preferred to move to a neutral bias at the last meeting. The more awkward development for Warsh is that the labour market also appears to be inflecting stronger. High-frequency indicators, including ADP’s weekly NER Pulse, suggest private-sector hiring has firmed, with the latest four-week average rising to 42k per week, equivalent to a monthly run-rate of roughly 170k-180k if sustained. While the series is preliminary and not a one-for-one payrolls forecast, the recent pickup is consistent with a jobs market that is reaccelerating rather than cooling. That pickup could become problematic for Warsh’s presumed goal of avoiding a renewed hiking cycle. With hiring reaccelerating at a time when the Fed now acknowledges that breakeven payroll growth is close to zero, the risk is that the unemployment rate begins to ratchet lower, putting renewed upward pressure on wages. In that scenario, rate hikes would become difficult for any Fed Chair to avoid.

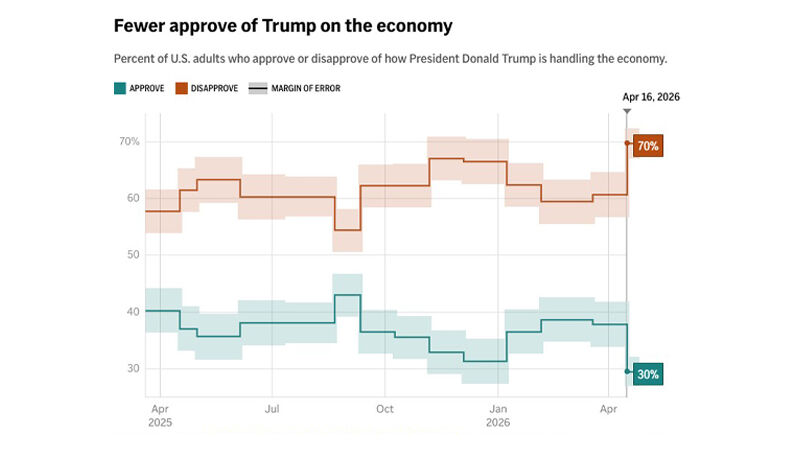

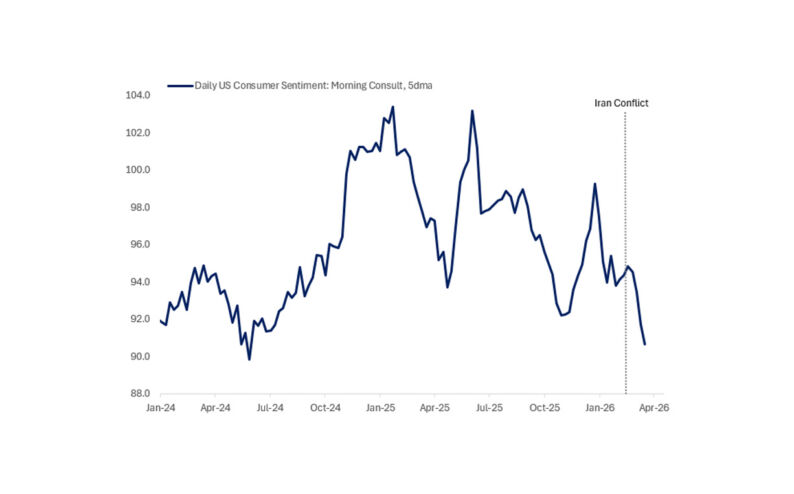

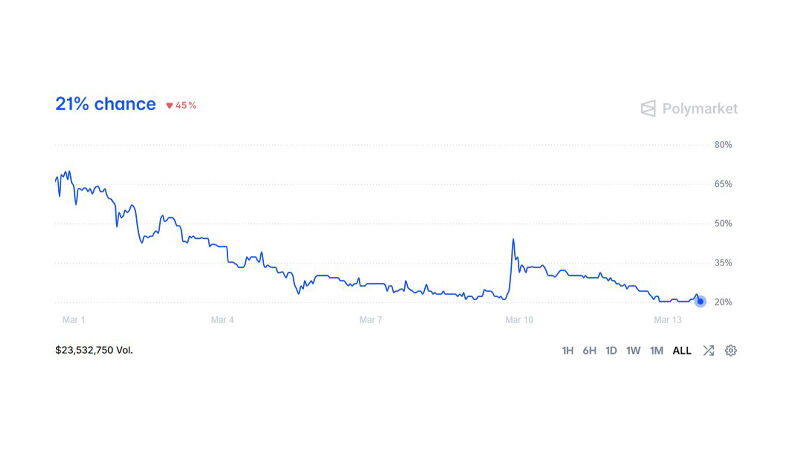

INFLATION IS A PROBLEM NOT JUST FOR THE FED, BUT FOR THE WHITE HOUSE TOO. A CBS News/YouGov poll conducted 13-15 May found only 27% of Americans approve of President Trump’s handling of inflation, while 77% say their incomes are not keeping up with prices. The same polling found 70% feel “angry” or “frustrated” about the economy, showing how emotionally charged cost-of-living issues remain heading into the midterms. As we saw under the Biden Administration, inflation is politically toxic because voters don’t experience “disinflation”…they simply feel higher grocery bills, rent, insurance, and gas prices that never really went back down. Moreover, the Iran war is proving unpopular…79% of Americans say the war affected their cost of living and 62% say it’s become harder to pay bills in the last six months, according to a report from the institute for global affairs. However, modern-day US elections are fought by galvanising the base, so it’s noteworthy that 73% of Republicans approve of President Trump’s handling of the war and only 19% disapprove. Nevertheless, my sense is that the Iran conflict and its repercussions are exposing tension inside the Republican coalition. Indeed, the House leadership pulled a vote this week to restrict POTUS’ ability to conduct military strikes against Iran after it became clear that the resolution was likely to pass – something that would’ve been an affront to the President. In reality, traditional hawks remain supportive of the war, but support softens substantially when voters are confronted with the prospect of higher gas prices, inflation, or talk of long-term troop deployment…concerns that are especially salient amongst the GOP’s working-class populist base. The modern GOP base is increasingly non-college educated, working/middle-income and more economically stressed than traditional Republican suburban voters. Gas prices above $4.50 matter…a lot. On top of all this, US electricity demand is now rising materially for the first time in decades largely because of the AI data centre expansion. Utilities, grid operators, and regulators have repeatedly warned that hyperscaler AI buildouts are accelerating power demand forecasts…grid operators in Texas, Virginia, Georgia, Arizona, and parts of the Midwest have warned that data centre growth is becoming a major driver of future capacity needs and transmission investment. The political framing risk is clear: ordinary consumers paying more so trillion-dollar tech companies can train models and build hyperscale compute clusters. The politics become even more combustible when rising energy costs are paired with fears of AI-driven job displacement, creating the perception that ordinary workers are being asked to subsidise technologies that may ultimately replace them. The reaction from graduates to mentions of “AI transformation” in recent commencement speeches is telling. Ultimately, the politics on this topic may increasingly resemble the politics of globalisation…diffuse long-term gains paired with highly visible local costs, which risk a political backlash. Personally, I’m a genuine believer in the transformative potential of this technology and its ability to reshape the global economy, enhance scientific advancement to solve some of the world’s most pressing problems, and improve the everyday lives of many people. But the politics are becoming harder…if AI is increasingly associated with higher energy costs, job anxiety, and concentrated corporate power, the industry needs far more compelling advocates capable of articulating the upside. Welcome to the politics of AI.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/