-

Who We Are

- What We Do

Series: Some Macro ThoughtsDon’t Let the Labour Market Get You Down

By Nohshad Shah

EQUITY MARKETS ARE POWERING HIGHER AS INVESTORS EMBRACE MY “RIGHT TAIL” SCENARIO. Since early May, I have been bullish on both the US economy and risk assets as the fog of tariff-induced uncertainty cleared and the heady mix of loose financial conditions, a once-in-a-generation AI capex investment boom, and pro-cyclical policy easing have combined to generate significant upside in stocks. This is now much better reflected in pricing than it was a few months ago. Bond markets show concerns around spot weakness in the labour market and a dovish pivot by the Fed – Chair Powell has made it clear that the FOMC is unwilling to tolerate heightened risks of a deterioration in their employment mandate. But equity markets are forward looking, discounting an outlook that sees stronger economic growth and higher margins for corporates. This reminds me of one of my core investment mottos (along with my favourite “Do not bet against the US economy”)…”if you want to be long growth, get long equities…if you want to be short growth, get long bonds”. Of course, this week’s shutdown of the US government was a reminder that tail risks can emanate from anywhere…markets have been sanguine about past shutdowns for two reasons…first, they have typically been short (since 1976, we’ve had 20 shutdowns lasting on average 8 days)…and second, federal employees have been furloughed (rather than laid off). The risk here is that the combination of an emboldened President Trump and a Democratic Party that is willing to take the fight to him leads to a long shutdown with negative consequences for growth and unemployment. As a reminder, the last shutdown was during Trump I in 2018 and lasted 34 days. The issue at stake here is repealing Obamacare, something which the President has long called for…but ending the subsidies would result in higher premiums for 20 million people, at a time when the cost of living and inflation remain a key concern for voters. Interestingly, out of 75 congressional districts where at least 10% of the population is enrolled in the Affordable Care Act, 62 are in GOP-leaning Texas, Georgia, and Florida, according to the Kaiser Family Foundation. A typical lower-income enrolee would see monthly premiums rise by 165%….heading into next year’s midterm elections, this could become a serious issue. Moreover, senior White House officials have stated that “firing” of federal employees will start in coming days – which if confirmed at scale, would mark a departure from prior furlough schemes and pose a threat to an already weak labour market picture. One cannot ignore the impact of hundreds of thousands of federal employees being furloughed (with some at-risk of being fired), discontinued or reduced provision of public services and the resulting confidence shock if this continues for weeks-on-end. It does not feel like either side is in the mood for compromise and President Trump is unlikely, in my view, to pay heed to past precedent when it comes to shutdown negotiations. Markets are under-pricing the probability of a prolonged crisis and its impact.

Bloomberg US Economics Surprise Index, 2Y UST Bonds

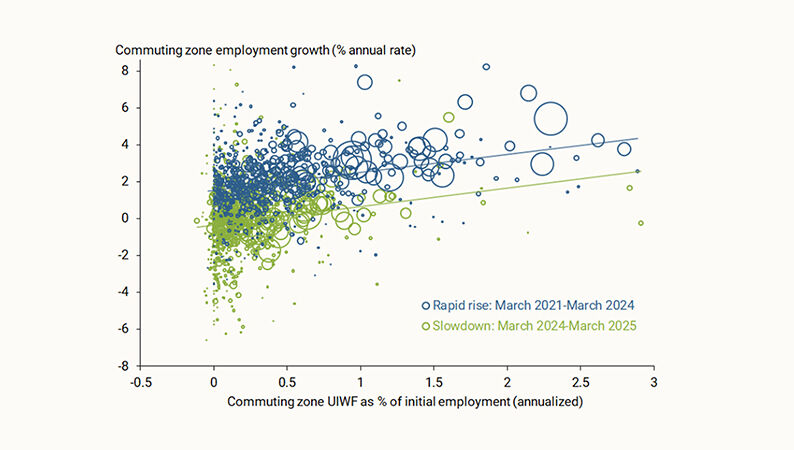

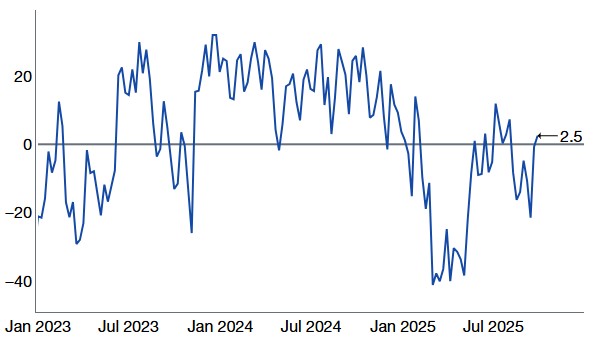

ECONOMIC ACTIVITY DATA CONTINUE TO SURPRISE TO THE UPSIDE…reflected neatly in the Bloomberg Economic Surprise Index (chart above). Similarly, the Dallas Fed’s high-frequency tracker (WEI) is at 2.4% (scaled to Q4 growth) and the Atlanta Fed’s GDPNow sits at 3.8% (for Q3). This represents robust consumer spending and business investment as the economy moves on rapidly from April’s confidence shock. An interesting paper by Nicholas Bloom examines the impact of uncertainty shocks on production and employment…he finds that peak impact typically occurs around 4-5 months following the shock (chart below)…so, the historical analogue suggests that the worst effects of the tariffs shock should be being felt around now. My sense is that timelines have accelerated since the publication of this paper…but even if this is somewhat accurate, then there should be plenty of upside to economic growth from here as companies and consumers get even more comfortable with the improving outlook. The labour market data continues to suggest weakness, though I see this more as a low-hiring / low-firing employment landscape with immigration playing a substantial role in lowering the breakeven rate for NFP to sub 50k. Whilst the latest Payrolls release is delayed, ADP private payrolls showed -32k, reflecting a decline for two months in a row…but the figure included a benchmark to data from the Quarterly Census of Employment and Wages (QCEW), which lowered figures by 57k and 43k for the August and September prints, respectively. This highlights a problem since the pandemic – seasonal patterns of employment have been much more unpredictable, and so seasonal adjustments to data are proving less reliable. On that note, when you look at non-seasonally adjusted Initial Claims (as well as ADP), the picture looks much more reassuring for the labour market (chart below). So where is the weakness? It stems from a couple of factors in my mind – first, the structure of the labour market means that immigrants and US born workers often do not compete for the same jobs…instead, they typically complement US employees and increase their productivity (think low-skilled immigrant labourers allowing farmers to expand agricultural production). In the current environment of reduced net migration, what this practically means is not only a shrinkage of labour supply, but a reduction in hiring…not because the jobs do not exist, but because the available workers will not fill those vacancies. Second, uncertainty around both government policy and the implications of AI has likely played a role in firms’ hiring plans…and whilst sentiment indicators are already inflecting upwards, it takes longer for employment decisions to be made…but referring back to the shock chart below, the peak negative impact should be around now…and if this is the worst the labour market is going to get, then we should avoid a full-blown recession. Add into the mix the fact that the Fed is cutting rates to avoid exactly this recessionary outcome, then we should be in solid shape. In sum, whilst the labour market is clearly weak (and stagnant), my estimation is that we will not see an accelerated deterioration…and most other aspects of the economy are doing just fine…whether you look at retail sales, durable goods orders, household and corporate balance sheets or business investment…the US economy has (yet again) shown remarkable resilience and flexibility. As expansionary policies play out in coming months – and along with it the Q4 data – we should expect to see hiring pick up and labour market slack to reduce…I see no reason why the sensitivity of the labour market to economic growth should reduce, over the long-term.

Non-Seasonally Adjusted Initial Claims

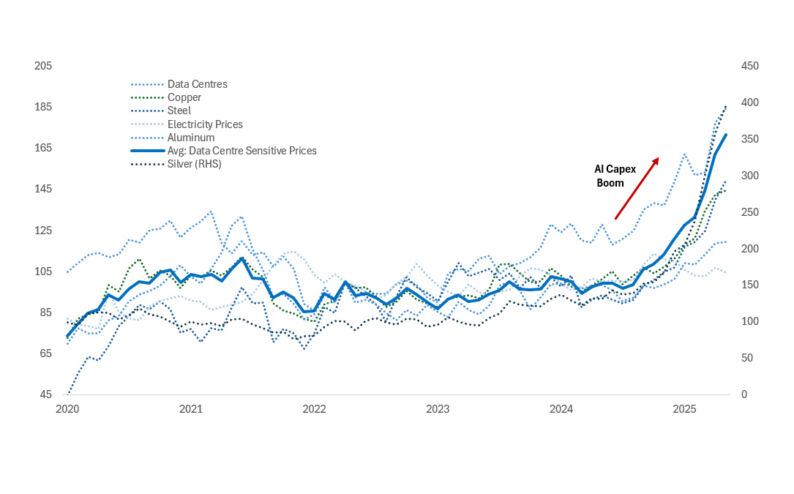

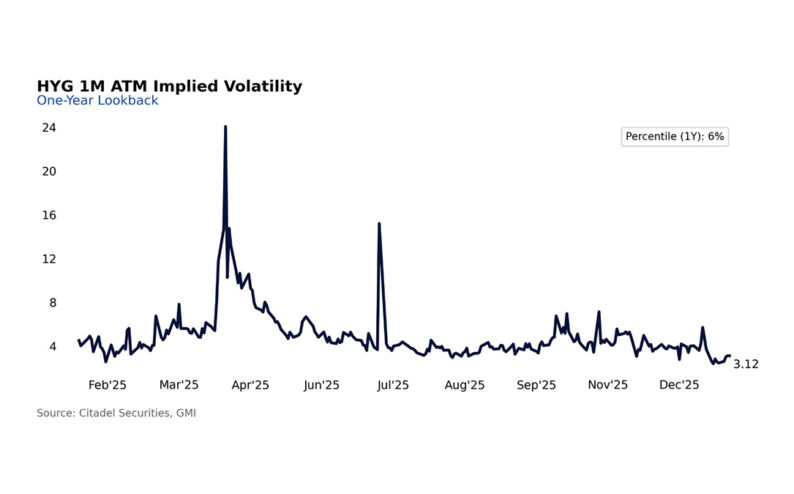

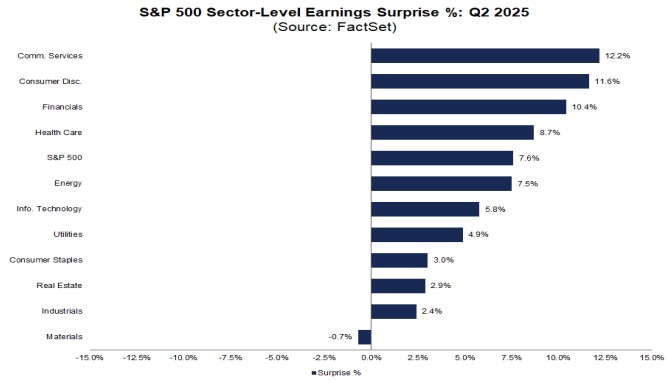

WHAT ABOUT MARKETS? The Fed is now committed to a series of rate cuts into the end of this year (Oct + Dec)…in the current climate I do not see Chair Powell departing from the plan outlined in September’s SEP – the political risks are too grave. If I am right about the activity outlook, this means we have embarked upon a non-recessionary rate cutting cycle, which is very favourable for equities performance to the tune of ~18% for the following 12-month period. Market measures of implied vol such as VIX (for stocks) and MOVE (for bonds) remain very subdued (chart below), suggesting the market is not concerned about recession risks. Financial Conditions (FCI) are the easiest they have been in over 3 years…and both fiscal and monetary policy are set to ease further, providing a rich backdrop for risk assets. Q3 earnings season will be upon us in short order…and following a strong Q2 (+11% YoY earnings; 81% beat estimates), expectations will be high. As my colleague Scott Rubner notes, this may create the risk of disappointment. One aspect of the Q2 results I found interesting was the surprising breadth of earnings beats – spanning Comm. Services, Consumer Discretionary all the way down to Industrials…and equity valuations tend to re-rate higher when earnings surprises are broad-based and sustained. As we enter potentially the ninth consecutive quarter of positive earnings growth, it’s safe to say that this is happening. Many institutional investors have avoided investing heavily in stocks this year, as evidenced by the Bull-Bear Spread (chart below) which is barely in positive territory and certainly a long way from levels seen in 2024. They have been spooked by a combination of April’s tariff confidence shock and concerns around an “AI bubble”. This has proven to be costly. Instead, retail investors have benefited as evidenced by our flows at Citadel Securities. Whilst there are certainly signs of frothiness (especially in some of the deals being announced), the fundamentals behind this rally remain sound…valuations are high, but earnings are keeping up…leverage is not extreme by any measure and balance sheets remain healthy (except the government’s!)…positioning is somewhat stretched, but participation is not broad…IPO activity is not in speculative territory…macro conditions are healthy….and government policies are designed to deregulate and stimulate the economy further. The stock market is being propelled higher, not by broad-based buying across the entire investor complex, but by the concentrated ownership and performance of Hyperscaler companies determined to win the AI arms race, spurring a once-in-a-generation capex boom. These companies see AI not simply as a source of revenue, but as a matter of survival – they must invest or risk going to zero in a world where innovation in LLMs, robotics, superchips and energy infrastructure is lightning fast…and rewards will flow only to those who win. Some of these companies are almost certainly ‘throwing good earnings after bad’…and I fully expect some to not be here in the future – investors should be aware of this. This is how innovation happens. But the broader point is we are amidst a megatrend, which both the largest companies and the largest governments (US and China) are fully invested in. As Jeff Bezos aptly noted this week, this is a “good” bubble, distinct from past ones and “This is real. The benefits to society from AI are going to be gigantic”. Once the dust settles, widespread adoption of AI will enhance productivity, which in turn should boost earnings and trend growth…it’s important to differentiate the near term frenzy from the lasting benefits.

Implied Vol in Bonds (MOVE) and Equities (VIX)

Source: Factset

AAII Bull – AAII Bear Spread

Source: AAII

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Some Macro Thoughts - What We Do