-

Who We Are

- What We Do

Series: Some Macro ThoughtsEveryone is Short the Inflation Tail Risk

By Nohshad Shah

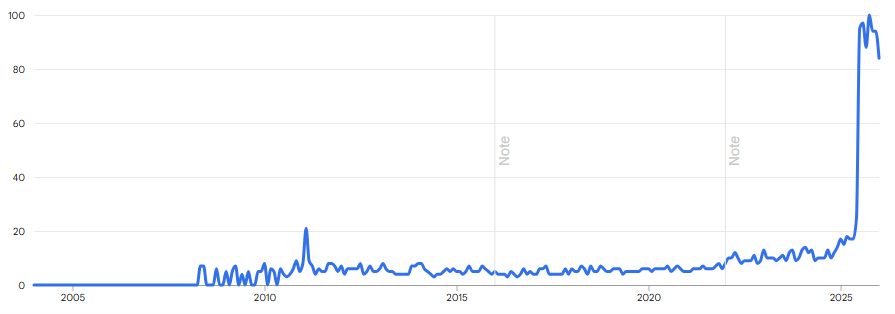

EVENTS THIS WEEK REINFORCED THE HEADLINE FROM MY LAST NOTE: “BEWARE OF COMPLACENCY”. The Greenland kerfuffle – which at one point appeared capable of rupturing NATO – was a timely reminder that we are now firmly in a geopolitical world order driven by power rather than rules, with meaningful implications for both policymakers and markets. In the immediate aftermath of President Trump’s bid to acquire Greenland, NDX fell ~2%, the dollar index (DXY) depreciated by ~1%, and 30y UST yields rose sharply by 12bps. While some of these moves have since reversed following the announcement of a framework agreement, the episode underscores that policy-driven, exogenous shocks are a feature, not a bug, of the current environment. This bold Administration is willing to challenge received wisdom on many issues, while also remaining pragmatic enough to pivot in response to market reactions and ultimately reach a viable outcome. Short-vol, carry-based investors should take note. As Davos returned to centre stage this week, an obvious question emerged…was such sabre-rattling necessary to achieve US national security objectives? The answer, as ever, is nuanced. The approach – creating visible strain within NATO, the cornerstone of Western security for 75 years – will have been objectionable to many. Yet, as Canada’s PM Mark Carney argued, the rules-based international order is no longer a functional framework for global cooperation and is being supplanted by a harsher reality of great-power rivalry. His call for “middle powers” to coordinate, diversify alliances, and pursue strategic autonomy carries particular weight for Europe, which found itself bearing the brunt of US ire. Less joint statements, more action is the clear message. America’s strength, agility, and innovative capacity are indisputable…and it is asserting them in a way the rest of the world must now internalise. Let’s give credit where it’s due…who was focused on (now-deemed-essential) Arctic security a month ago?

Google Search Intensity: “Arctic Security”

Source: Google Trends, Jan 26

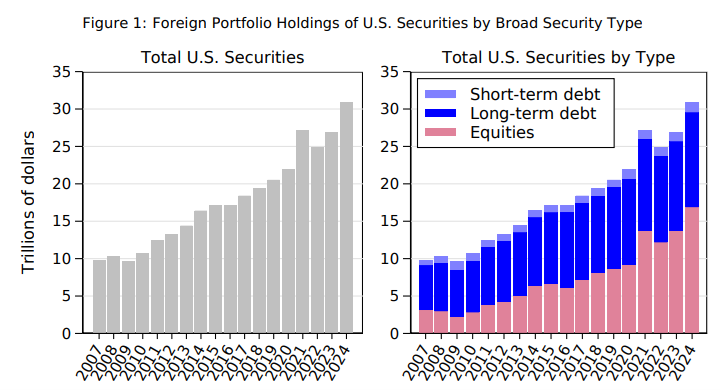

THE SELL-OFF IN JAPANESE BOND MARKETS AT THE START OF THIS WEEK IS A REMINDER OF THE GLOBAL NATURE OF FISCAL PROFLIGACY…and the implications for term premium and the smooth functioning of bond markets. Specifically, the sell off was driven by PM Takaichi’s suggestion that she would cut consumption tax for two years, a fiscal easing that would cost around $32bn (0.7% of GDP) and comes in addition to a previously announced fiscal expansion of $135bn (3% of GDP). Of course, governments and central banks have tools to address these episodes of market stress…as my colleague Frank Flight highlighted in a timely note, the BOJ appears to be willing to conduct emergency purchases should market functioning concerns persist, which unwound some of the move. However, there’s no free lunch in markets and ongoing pressure on the currency and inflation expectations will be the results of what is essentially, a (mild) form of financial repression. The broader takeaway for macro markets is that investors globally are becoming increasingly uncomfortable with current levels of government spending, making buyers’ strikes in major fixed income markets more common. The dollar’s global reserve status confers a structural advantage to US bond markets, keeping term premia lower than elsewhere as persistent foreign demand – including the recycling of current-account-deficit dollars – is channelled into Treasuries. This results in significant ownership of US assets by international investors…the TIC data from the US Treasury shows that foreign investors own ~21% of US securities outstanding at a total value of $30.9tn (based on valuations at the time of the most recent annual report, June 2024). The composition is interesting…foreign investors own 33% of USTs, 27% of US corporate debt, and 18% of US equities outstanding. Whilst there is no imminent catalyst, the combination of significant international ownership of US assets, the size of the US treasury market and the simple fact that it is the backbone of the global financial system means that the ramifications of any sustained loss of confidence in the US fiscal position would have consequences that are significantly more global in nature and severe in impact than the various bouts of instability that markets have experienced in the UK and Japan.

Source: US Treasury Department, Annual reports on Foreign Portfolio Holdings of U.S. Securities, released Feb-25 (data as of June-24)

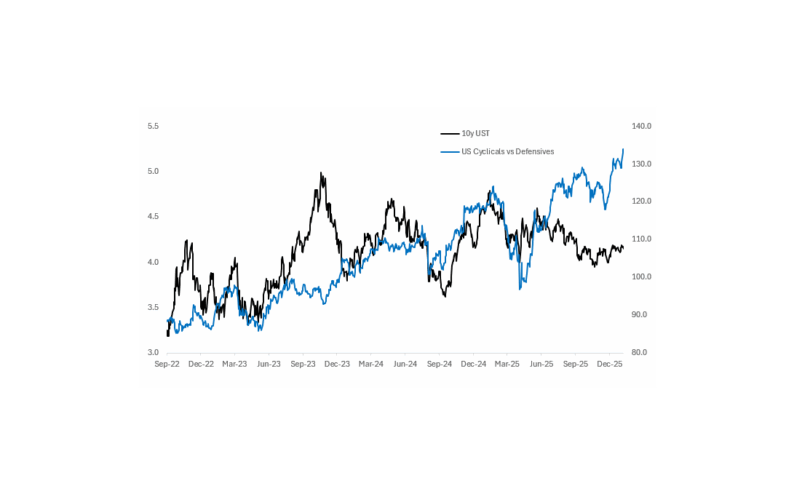

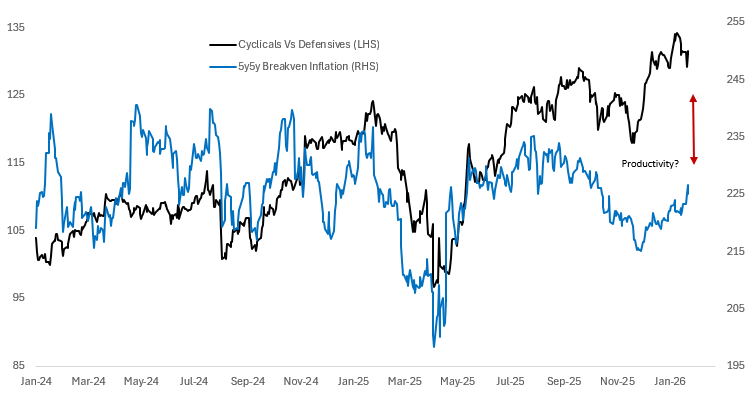

ALTHOUGH THERE IS NO IMMINENT CATALYST, DEBT IS STILL GROWING FASTER THAN THE ECONOMY…which definitionally puts debt/GDP on an unsustainable trajectory, something which will need to be addressed at some point, either through lower deficits or faster growth. Markets hope that productivity gains resulting from AI will be able to put debt to GDP ratios on a better trajectory. Indeed, relatively moderate but permanent increases in productivity growth can meaningfully alter the forward path of government debt. Over the medium term, I have no doubt that AI will be able to deliver improvements in productivity growth…however, my concern is the near-term risks are more skewed towards disappointment for two reasons. First, it seems that macro markets are already discounting a relatively elevated productivity assumption – for example, 5y5y forward inflation breakevens have become disconnected from the cyclical outlook (chart below: cyclical stocks vs 5y5y inflation) – which likely suggests that markets see a higher speed limit on the economy in which high growth does not create inflation as productivity gains boost the supply side capacity of the economy. Second, history suggests that productivity gains from technological change are incremental and compound over multiple years to create substantial improvements in total factor productivity…essentially a trajectory that is J-curved in terms of impact. In my mind, there is likely too much emphasis on immediate productivity improvements from AI, even though the medium-term trajectory is meaningfully positive. This opens up the risk of disappointment in the near term. Given that productivity is calculated as a residual and extremely hard to measure in real time (only really observable by inference from macroeconomic outcomes), the risk is that the market will find out too late (by inflation realising higher than expected) that it has over-indexed to short-term productivity gains. A strong cyclical acceleration in the economy – something which I have been discussing for some time, driven by loose financial conditions and a large fiscal stimulus – is currently expected to be accompanied by steep disinflation in the second half of this year. The extent to which that disinflation materialises will define whether or not the current goldilocks narrative of easy financial conditions, strong growth and disinflation can persist. The problem is that everyone from governments, central banks, equities, and fixed income are levered to the productivity story…and hence short the inflation tail.

Source: Bloomberg, Citadel Securities

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Market Insights - What We Do