-

Who We Are

- What We Do

Series: Macro ThoughtsFlooding the Zone (with Good News…Mainly)

By Nohshad Shah

THE MARKET’S RE-RATING OF US ECONOMIC GROWTH IS NOW IN FULL SWING…buoyed by the US Administration’s dramatic U-turn on China tariffs on Monday. Following a sharp ratcheting after liberation day, there was an equally dramatic de-escalation this week with both sides agreeing to slash tariffs by 115% and a 90-day pause, suggesting further normalization to come. President Trump proclaimed a “total reset” in relations with China with a likely discussion with President Xi soon. Whilst there will inevitably be further headlines on this topic, in my mind this reflects a firm desire from POTUS to swiftly conclude the broader tariff agenda and focus on pro-growth policies…namely tax cuts and deregulation. Comments from Secretary Bessent, Director Hassett and the President himself all suggest that they want to move on from this saga…whilst we can expect some deals with the EU, Japan, and India, it seems likely that the Administration will unilaterally agree tariffs with the majority of trading partners. The market has realized this…first easing FCI through the rates risk-premium channel…then upgrading expectations of cyclical growth, led by performance in the equity market (SPX +20% from the lows). In simple terms, from mid-February financial conditions tightened, reaching their peak just after liberation day, signalling a stagflationary shock – a big hit to growth, likely leading to recession…and an inflationary spike driven by tariffs. This was a big headwind for business investment and consumption, and more broadly for investors in US assets…the beginnings of an unwind of “US exceptionalism”. Following acute pressure from both bond and stock markets, President Trump’s reversal has now caused a sharp easing of financial conditions, turning those same headwinds into tailwinds. As Q2 takes shape, the backdrop for US economic growth has become very bullish.

US Financial Conditions Index

Source: Bloomberg, 16may25

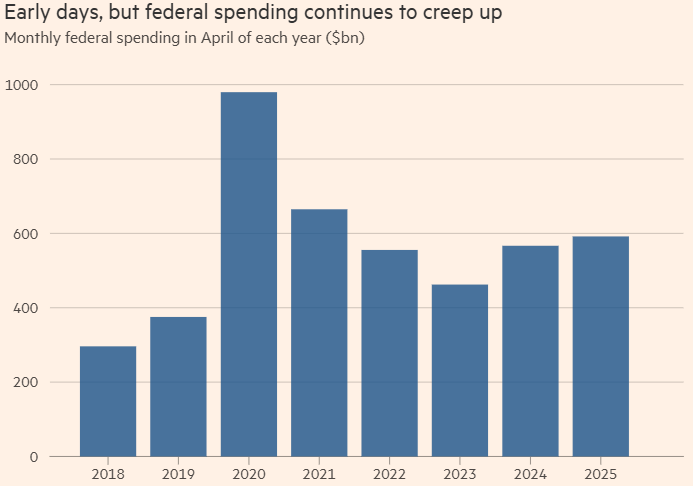

WHAT’S THE BULLISH CASE? Let’s start with fiscal. As budget negotiations continue to evolve, it’s becoming clear that the House bill would add $3.3tn to the debt (including interest) or $5.2tn if temporary provisions are made permanent, according to the Committee for a Responsible Federal Budget (CFRB). This is partly because new borrowing is front-loaded, whilst offsets are back-loaded…essentially leading to massively increased deficits in the next few years. CFRB estimate a $600bn boost to the deficit for FY27 with ~$770bn of new borrowing and ~180bn of cost reductions. This is a full 1.8% of GDP and represents a one-third increase in total projected deficits to $2.3tn and a doubling of the primary deficit. As the chart below shows, the bulk of tax cuts and spending happens in the 2026-29 window, whilst savings don’t kick-in until the second half of the 10yr budget window. Make no mistake. This is clearly by design and represents a substantial fiscal impulse and boost to growth (and inflation). Meanwhile, the much-anticipated savings from DOGE – once mooted to be as much as $2tn – are rapidly paling into insignificance. Their website claims $170bn in savings, but an FT investigation suggests only a fraction of that can be verified. At the same time, federal spending continues to rise with total outlays of $592bn in April, up both in MoM and YoY terms.

Source: FT, US Treasury

NEXT, CONSIDER THE OIL PRICE…we’ve had a 23% correction from January (chart below). One has to be careful here, because the US is now a net exporter…however, it’s still true to say that the impact on reduced transportation and energy costs and both the increase in disposable income for US consumers, as well as the stimulative effect on business investment cannot be ignored. Though there will be sectoral considerations (c.f. energy corporations), with consumption forming 70% of US GDP, the multiplier effects of lower energy can be very significant, so in aggregate I expect there to be a short-term boost to the US and global economies. The contribution to lower headline inflation will also be welcomed by the Fed.

Oil

Source: Bloomberg, 16may25

THIS WEEK’S PHILADELPHIA FED data reflected some of the recent optimism given it was collected 5-12 May. The diffusion index for current general activity rose from -26.4 to -4.0, but more interestingly, the New Orders reading went from -34.2 to +7.5…offsetting nearly all of April’s decline with most firms also indicating an increasing in employment. This is an early sign of the bounce back in the survey data that we are likely to see in coming weeks. Ultimately, these diffusion indices represent the sentiment of consumers and businesses, and one would expect them to be turning positive in short-order as the forward-looking outlook shifts to a more positive tone. On that note, President Trump’s visit to the Middle East brought with it much in the way of commercial deals…$300bn (with plans to increase it to $1tn) of commitments from Saudia Arabia…$243bn from Qatar…and $200bn (with a prior commitment of $1.4tn over 10 years) from the UAE. Whilst there was clearly some hyperbole on display, there’s no doubting the desire from these petrodollar rich nations to strengthen their relationship with the USA using FDI…likely in exchange for the US security umbrella. Semiconductor stocks got a boost from the scrapping of a Biden-era rule restricting the export of artificial intelligence chips that was due to take effect on 15 May and the announcement of plans to build the largest group of AI data centres outside of the US in the UAE – with 2mio of Nvidia’s latest generation of GB200 chips.

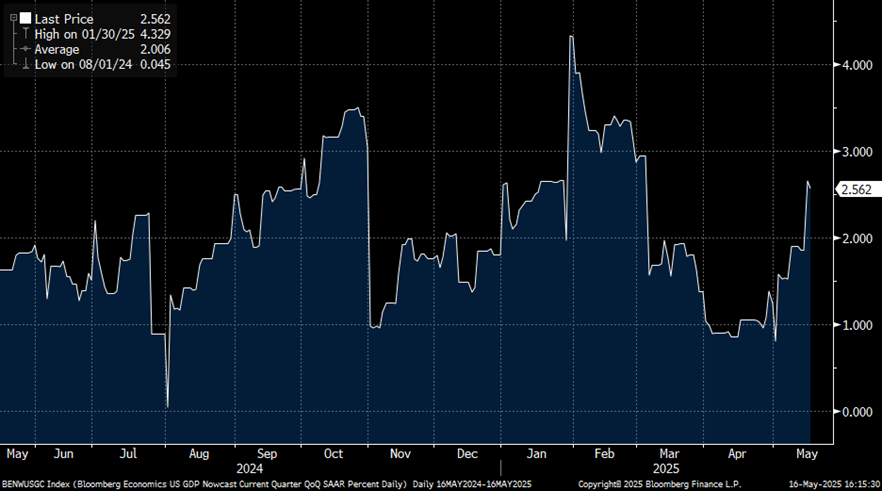

All of this reflects what I have been stating in this note for the past few weeks – having been boxed-in by markets on the tariff agenda, the sharp reversal we have seen to normalize relations with China to a more agreeable level reflects a desire by President Trump and his advisors to move-on and focus on his pro-growth policies. Given a starting point of 3% Core GDP in Q1…and the upcoming fiscal boost…combined with lower energy prices and further deregulation…the backdrop for nominal growth looks strong. The Bloomberg US Real GDP Nowcast neatly reflects this growth upgrade…we are going from expectations of ~1% GDP growth to 2.5-3% (chart below). Strong nominal growth is typically an environment in which equity markets perform well, which is what we’re starting to see play out. As mentioned last week, this is an “unloved rally” with most investor segments (with the exception of retail) under-exposed to US equities. Should the good news continue to build, expect more of them to get “stopped in” to this rally. Watch the right tail.

Bloomberg US GDP Nowcast

Source: Bloomberg, 16may25

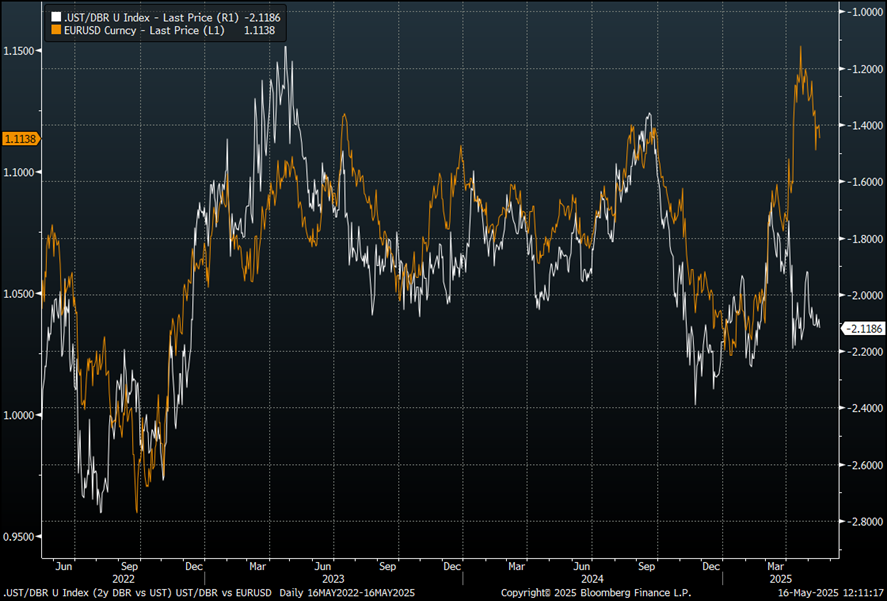

THE FED REMAINS OUT OF PLAY. An environment of moderate tariffs is problematic for anyone expecting rate cuts. With current proposed levels, after consumption shifts, the effective tariff rate for the US economy is 16.4% according to the Yale Budget Lab (though I would say there is downside risks to this number, given the direction of travel). This has a Real GDP impact of -0.65% on Q4-Q4…not enough to warrant a recession, given the starting point. At the same time, Durham Abric, our inflation expert, estimates Core PCE at 3.35% YoY under these circumstances. That is not an environment in which the Fed is cutting rates…and I do not see them cutting at all in 2025. I mentioned last week that the US front-end was pricing too much in the way of cuts and this has continued to correct, moving from 100bps of cuts priced on 30 April to ~55bps now. Given this represents a probability-weighted distribution of outcomes, it no longer looks out-of-whack, though I would expect it to trend towards zero gradually over time. Where valuations do look out of lockstep are in USD fx…whilst the market was focused on the unwind of “US exceptionalism” theme, it made sense that the currency took the brunt of the hit…both from hedging of fx exposure and the sale of US assets. With the 180 degrees change in the narrative…and equities and rates responding accordingly…the desire for global investors to own US assets on an unhedged basis should revert closer to where it was…and the fx market should move back to trading rate differentials. On that basis, EURUSD looks around ~8% overvalued (chart below).

WHAT ARE THE RISKS? Late on Friday, Moody’s stripped the US of it’s sovereign triple-A rating warning about rising levels of government debt and the widening budget deficit…“While we recognise the US’s significant economic and financial strengths, we believe these no longer fully counterbalance the decline in fiscal metrics”…a quite sobering statement. With S&P removing the top rating in 2011 and Fitch in 2023, the US does not hold a AAA rating from any of the top 3 agencies for the first time in history. This has been a long-time coming and investors would do well to remember the last time this happened in 2023, when the bond market experienced a mini-tantrum with a circa 100bps sell-off in 10y Treasuries over the course of two months, catalyzed by the Fitch downgrade (though other factors certainly played a role). This is a very real risk, especially with the lack of demand for long-end bonds with the current backdrop. Buyer beware.

EURUSD vs rate differentials (2y DBR/UST)

Source: Bloomberg, 16may25

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Macro Thoughts - What We Do