-

Who We Are

- What We Do

Series: Macro ThoughtsForward Trajectory > Spot

By Nohshad Shah

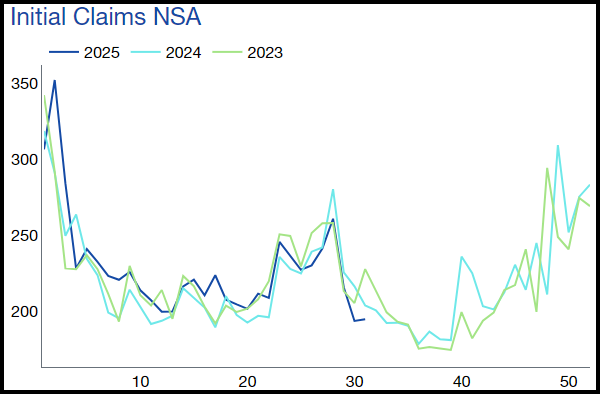

WEAKNESS IN THE US LABOUR MARKET IS MORE PRONOUNCED…with the recent Payrolls report bringing down the 3m Avg. for NFP to 35k. Although revisions of this magnitude could signal a recession, it’s important to consider the broader backdrop before reaching that conclusion. As mentioned in this note before, following President Trump’s tighter immigration controls, the breakeven level for NFP is ~75k now, and whilst the all-important u/e rate did rise to 4.2479% (the highest since Oct 2021), it remains broadly within the 4.0-4.2% rounded range of the last 15 months…so weakening, but not recessionary…especially when compared to historical levels. Similarly, Average Hourly Earnings (AHE) have been stable…and Initial Jobless Claims 4wk Avg. is ~220k, still far from concerning levels (350k+) and exhibiting some of the seasonality we have all become accustomed to (chart below). However, private sector job creation has undoubtedly weakened in recent months. So, what to make of the substantial 258k cumulative downward revision in NFP? Front-end rates were quick to extrapolate the weakness and price in greater recession risk, reflecting the approx. 3-std deviation move below the mean of historical revisions. An interesting paper by Peter Earle of the AIER, highlights that NFP revisions are not normally distributed. Instead, monthly revisions have very high kurtosis (21.56) reflecting a distribution that is prone to producing outliers: “High kurtosis is a signature of a “fat-tailed” distribution: one where extreme values occur more frequently than a normal model would predict.” Past revisions reflect this behaviour, with even 7-std deviations from the mean. In other words, when looking at these revisions, it’s important to remember that the heavy-tail nature of BLS payroll data means it produces unusually large outliers more frequently than a normal distribution would predict – so whilst the -258k revision was certainly large, it wasn’t necessarily a game changer and policymakers should be wary of putting too much weight on this one number alone. That said, revisions of these magnitude are often clustered around turning points/shocks. The natural question then, is whether these recent revisions signal a turning point…we can’t rule it out…but I would argue that the April tariff announcements would qualify as a revision inducing event. To further quote from the article: “many of the most extreme revisions cluster around periods of major economic stress or transition, such as the 2008–2009 financial crisis and the COVID-19 pandemic, when labor market conditions shifted rapidly and initial estimates were based on incomplete or outdated assumptions”. Of course, these extreme turning points (GFC, COVID) were not reversed one month later as April’s tariff shock was…the rapidity of the decline in uncertainty following the tariff pause and subsequent market recovery should limit the extent to which we extrapolate past experience into this specific set of revisions.

Source: US Dept of Labor

Source: The Daily Economy, BLS

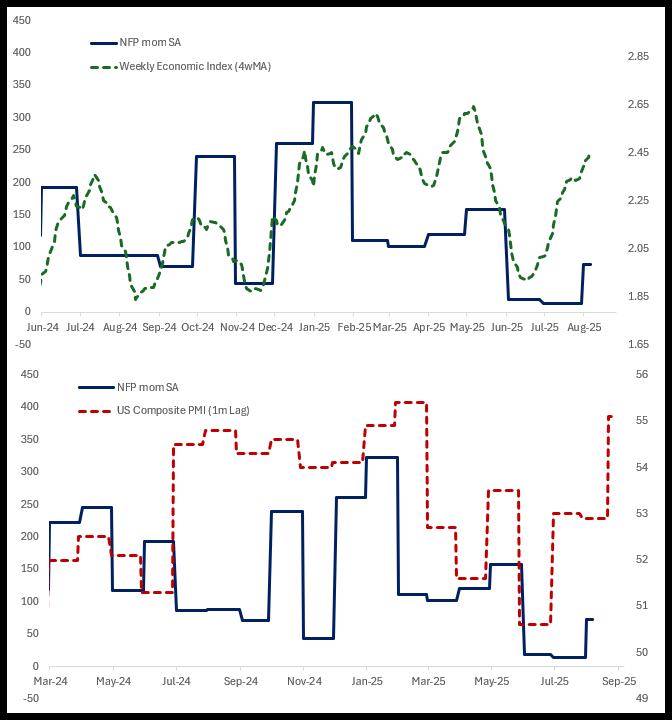

In my mind, what’s more important is the forward trajectory of the labour market in the context of the broader economic landscape…on that front, when looking at the Dallas Fed Weekly Economic Index, which is based on high-frequency economic data, we can observe the impact of President Trump’s April tariff measures creating a softening from May to mid-June…but since then, we have seen a clear uptick (chart below). Naturally, jobs data will operate with some lag, but this suggests we could see a swing upwards in NFP in the coming months. True labour market weakness – of the recessionary kind – only happens when you have an acceleration of layoffs…and we are just not seeing that.

Non-Farm Payrolls with Dallas Fed Weekly Economic Index & Composite PMI

Source: Dallas Fed, BLS, S&P Global

WHAT ABOUT THE BROADER BACKDROP? Q2 earnings season has been strong with 82% of S&P 500 companies beating EPS estimates and once complete, earnings growth is likely to be ~10% YoY, marking the third consecutive quarter of double-digit earnings growth. Whilst expectations were on the low side due to tariff concerns, this reflects a resiliency in corporate America which we’ve seen time and again. Tech hyperscalers have re-committed to their AI capex spend, taking the total to an estimated $360bn in 2025, a 60% YoY increase – this will continue to be a strong tailwind for the forward growth outlook. Consumption should hold up well with the boost in asset prices (both stocks and housing) and income proxies are running at 5.2% (AHE x total jobs x hours worked)…a healthy figure that should support personal earnings growth and ensure there is no persistent weakness in real household consumption. Financial conditions (FCI) are the loosest they’ve been in 3 years (chart below), suggesting a very supportive environment too…the rolling change in FCI should contribute +0.5% to GDP growth in 2026, should this continue. And President Trump’s recently approved fiscal package should add +0.9% to growth next year…especially important for individuals when considering the provisions regarding tips and state and local income tax (SALT) deductions. If we assume trend growth for the economy is around 2%, but is somewhat lower under reduced immigration, call it 1.5%…the above factors could still easily bring 2026 growth towards the 3% figure. And that’s before we consider what happens with tariff revenue…almost $30bn was raised last month, a 242% YoY increase. Secretary Bessent estimates a total of $300bn for 2025, which does not sound unreasonable…the question is what does President Trump do with this money…pay down the national debt? I doubt it. My bet would be he does another round of fiscal easing by distributing “tariff dividends” as a direct transfer to citizens, likely just ahead of next year’s mid-term elections. For all these reasons, I struggle to construct a bearish argument for US growth, even though the current spot outlook might be slightly weaker than originally expected. And remember, for markets, the FORWARD OUTLOOK is the only one that matters.

US Financial Conditions Index

Source: Bloomberg, 08aug25

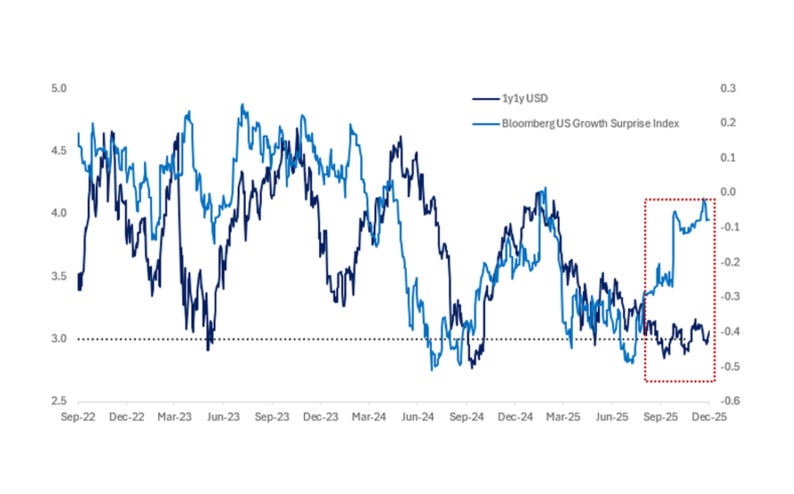

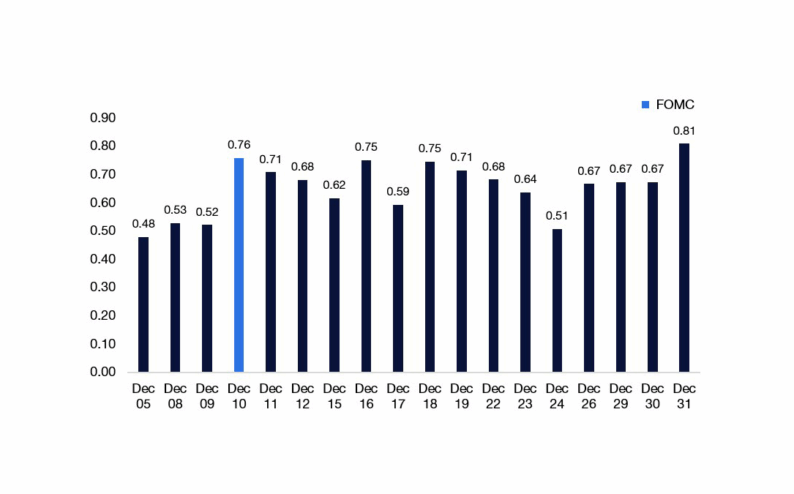

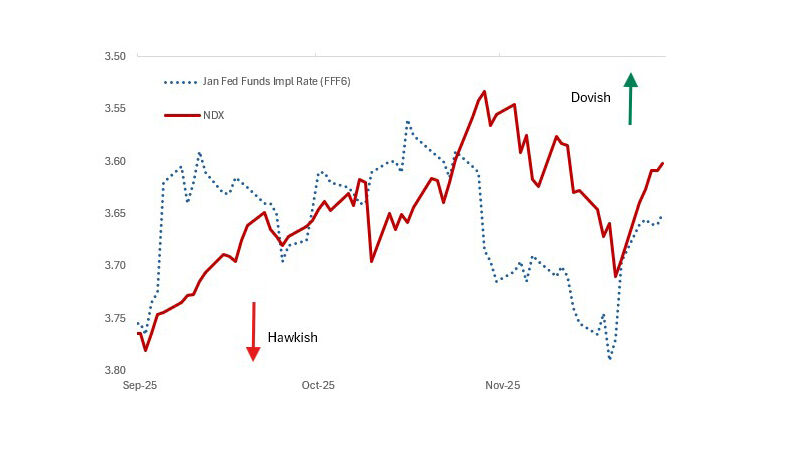

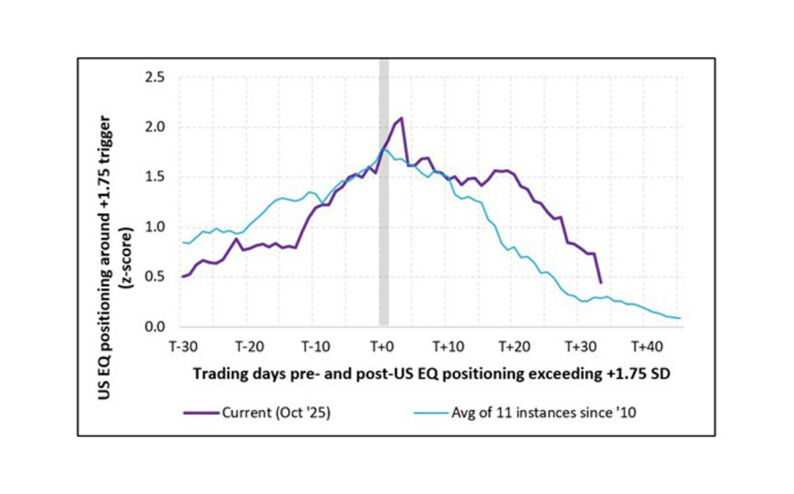

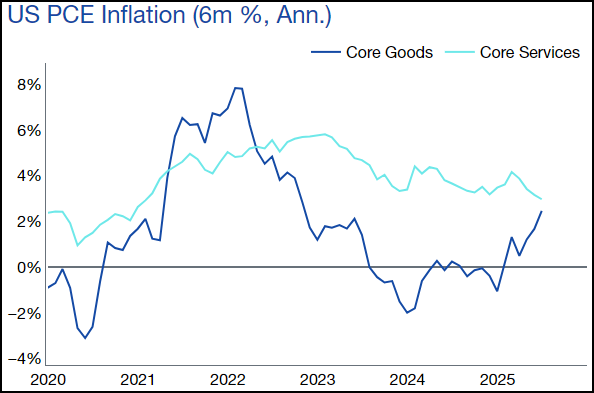

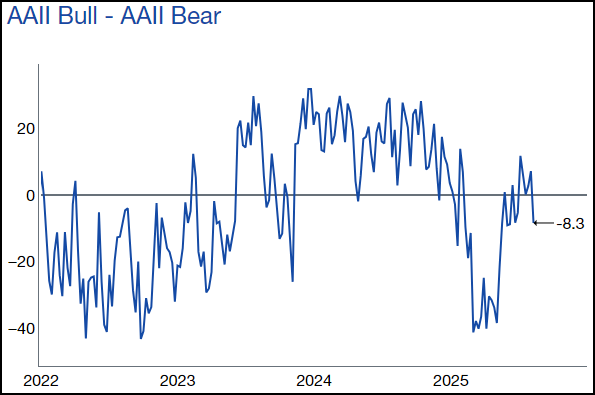

WHAT DOES IT MEAN FOR THE FED & MARKETS? Regular readers will know that my view has been that rate cuts are not warranted given the state of the US economy…with stock markets making new highs, FCI continuing to ease and inflation that remains meaningfully above-target (and likely to rise). My core view has been that growth, and the labour market have been moderating from strong levels, but we are not going to see a recession anytime soon…but more importantly, the forward outlook for growth has been on a positive trajectory since May. I continue to hold this view. If it were up to only Chair Powell, I doubt he would cut rates…but given the ongoing pressure from President Trump to lower policy rates and the recent labour market data, it’s now more likely that the FOMC will take the opportunity to do a 25bp insurance cut in September’s meeting. I still see this as a 60-40 likelihood and doubt they would consider a 50bp move like last year – at that time, the u/e rate was rising fast and sequential inflation was coming in lower than their forecast – categorically not the backdrop we currently have with Core Goods inflation rising worryingly and Core Services remaining stubbornly high (chart below)…with tariff effects yet to be fully felt. The next two CPI prints (starting Tue) will be key in determining the Fed’s level of comfort for any cuts. For asset markets, this leaves me bullish equities – a view I’ve held since early May. Indeed, our industry leading equities franchise continues to see retail buying in large volumes with 14 out of the last 16 weeks seeing net purchases, whilst institutional sentiment remains bearish (though we note some signs of change with a sharp increase in call option activity last week). My colleague Scott Rubner notes that this is the sixth longest bullish streak since 2020…I don’t see any imminent reason for that streak to end. In 10y rates, the bullish-but-still-rangebound move I had predicted is set to continue with no meaningful catalyst to break out of the 4-4.60% range, which will only add weight to the stock market rally. So, what’s the risk? Inflation. As I’ve been arguing since the beginning of the year, inflation remains a serious issue for the Fed…now even more so with this Administration’s policies = tariffs, fiscal expansion, reduced immigration, and tilting the Fed in a more dovish direction.

HAWKISH MPC DISAPPOINTS ONCE AGAIN…with a very close call on the August cut with an initially tied vote at 4-4-1, which upon a forced revote pushed the cut over the line by the finest of margins. The Bank completely de-emphasised the labour market weakness in favour of the salience of headline inflation (particularly food) on the formation of household inflation expectations. This was the argument put forth by Chief Economist Huw Pill back in May when he noted the risks associated with rising food and utility prices in causing second round effects via the real income resistance channel. The forecasts were revised up to see inflation peak at 4% and despite the long run inflation forecasts being at 2% over the policy relevant horizon, we should heed the message – Huw Pill is winning the argument. Despite the labour market weakness, the core of the committee seems to be shifting towards him (e.g. Lombardelli switching her vote). The burden is now on the inflation data to undershoot to resume quarterly cuts, and the baseline is likely to be “on-hold” until the MPR meeting in Feb 2026.

Source: Bureau of Economic Analysis

Source: AAII

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Market Insights - What We Do