By Nohshad Shah

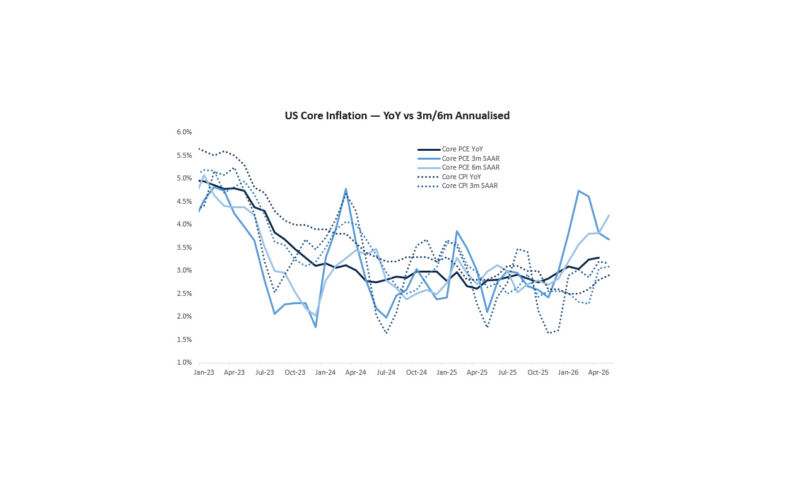

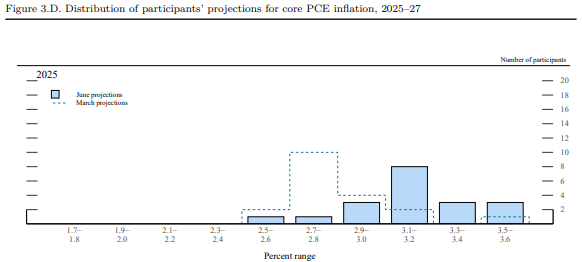

THIS WEEK’S FED MEETING…was a reminder of my oft-stated view that monetary policy remains in the passenger seat whilst government policy (especially the fiscal kind) is the driving force for markets. Despite President Trump’s best efforts, the FOMC decided to keep rates unchanged with only a slight change to the statement acknowledging that “uncertainty about the economic outlook has diminished”. In the Summary of Economic Projections (SEP) 2025 median expectations for growth were revised down (1.4% from 1.7%)…Core PCE revised up (3.1% from 2.8%)…and the unemployment rate up (4.5% from 4.4%). Expectations for the policy rate remained unchanged with two rate cuts pencilled in for the year. None of this will have been a surprise to the market…but the committee is clearly split with nine members signalling one/zero cuts, whilst ten are looking for two/three cuts. This is very much driven by concerns around tariff-induced inflation, as reflected by the shift in mean expectations on 2025 Core PCE from 2.7-2.8% to 3.1-3.2% for 2025…a substantive change (chart below). Chair Powell re-iterated his wait-and-see approach in the presser, largely justified given uncertainty around both sides of the dual mandate. The Fed will wait until it’s September meeting to make a call on the next move – three months of data should be enough to ascertain whether there is true pass-through to inflation and/or if the labour market materially weakens. My sense is that we are entering a period where we can see a moderation of the hard economic data…but not enough to warrant a recession. If markets price in deeper rate cuts off the back of this…combined with seasonally supportive flows into bonds…then this will only serve to ease financial conditions further. Meanwhile, the forward-looking sentiment data should continue to improve with economic tail risks diminishing and expansionary fiscal policy on the horizon. This, combined with continued AI-driven investment and innovation should continue to support risk assets once we move beyond the current geopolitical tensions. We may be headed into a goldilocks summer with both bond and equity markets performing well.

Source: Federal Reserve

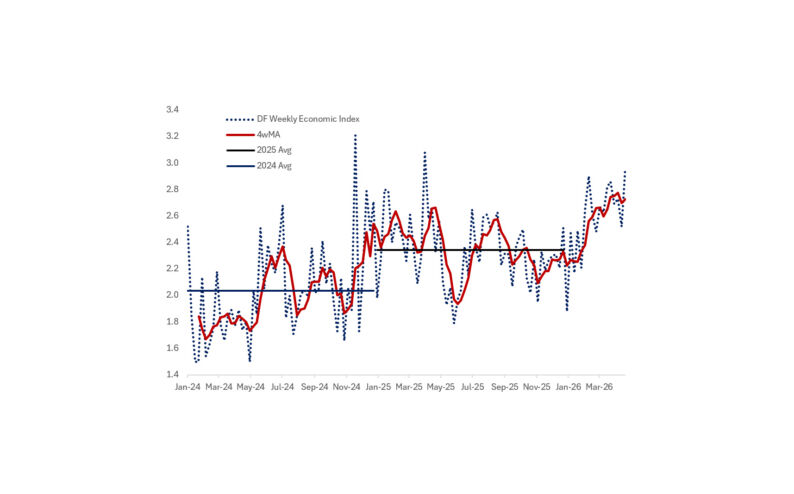

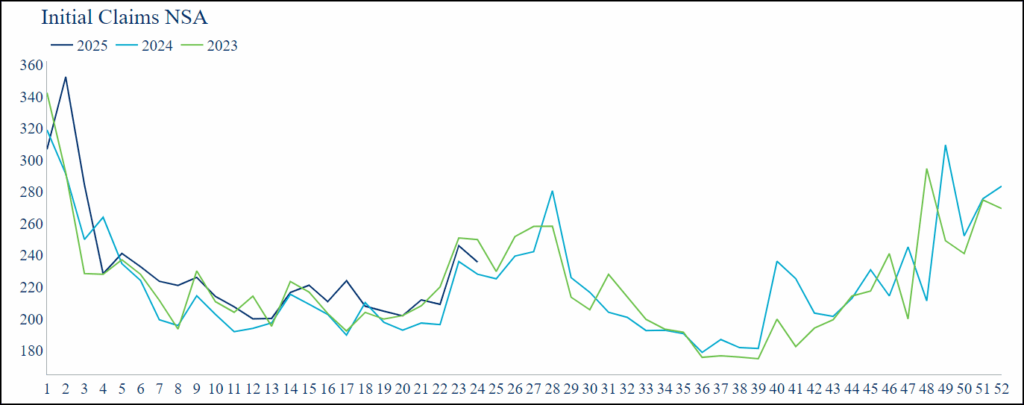

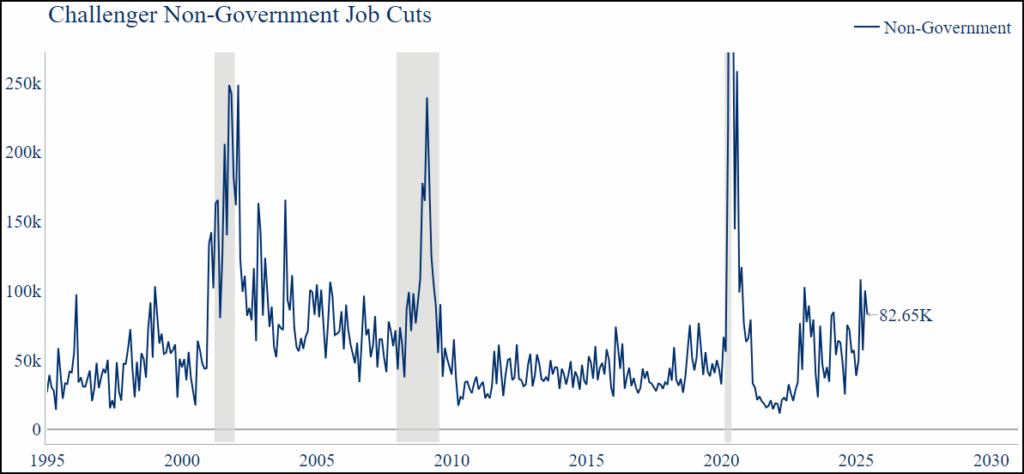

LET’S BREAK IT DOWN. The labour market is showing some signs of weakness…but nothing that should cause alarm. Initial claims are on the rise with the 4-week moving average at 245.5k…but this is not unusual when you look at the seasonal pattern over recent years – for the last two summers we have seen a similar rise, only for a normalisation shortly thereafter…and we are still far off levels typically associated with a recession (~350k+). Similarly, the closely watched Challenger Job Cuts were 93.8k for May, which if we strip out federal jobs, becomes 82.6k – a little elevated, but again, far from recessionary levels (chart below). On the activity side, it’s a similar picture…the latest reading of the Dallas Fed Weekly Economic Index (which tracks the state of the US economy using high-frequency data) is at 2.01% annualised quarterly GDP equivalent (13-week moving average: 2.25%)…suggesting a steady economy that’s treading water with some underlying components – temporary staffing (highly cyclical; now below trend), rail traffic (freight volumes sluggish), steel production & fuel sales (softening a touch) – reflecting yellow flags. This is not altogether surprising given the unprecedented level of policy uncertainty this year…but, as regular readers will know, my view is that we will not tip over into recessionary territory. I can envisage a scenario where these early signs of data weakness (which could accentuate in coming weeks) are interpreted by the market as signs of a recession, leading to greater rate cuts being priced into 2025 and 2026. In my mind, this would only serve to further ease financial conditions – lower yields, lower USD, tighter credit, and higher equities – from already easy levels of FCI (chart below).

Source: US Dept of Labor

Source: Challenger, Gray & Christmas, 5jun25

US Financial Conditions Index

Source: Bloomberg, 20jun25

THE SAGA OF THE UNITED STATES’ INFAMOUS LINEAGE OF FISCAL PROFLIGACY continued this week with revised dynamic estimates from the Congressional Budget Office (CBO) suggesting President Trump’s fiscal bill would raise budget deficits by over $300bn more than previously thought, putting the total figure at $2.8tn over the 10yr horizon. The analysis expands on prior calculations in two ways – first, reflecting the effects that the nontax provisions would have on the economy…and second, considering the effects of interest rate changes on net interest outlays for debt projected in the baseline. Because of the large stock of debt projected in the baseline, those increases in interest payments more than offset the primary deficit reductions driven by increases in economic output. The estimates also conclude that public sector debt would increase to 124% of GDP by the end of 2033…with total deficits increasing by $3.4tn over the decade. Quite something. The bond market continues to shrug this off…at least for now…10y UST yields remain rangebound at 4.42%, which is not a concern for anyone. Recent tick data released for the month of April showed a very modest $36.1bn reduction in total foreign holdings of Treasuries, keeping the overall number still above a whopping $9tn. As mentioned in this note before, this simply reflects the inability of the world to reduce its dollar exposure whilst the US continues to run large trade deficits. Whilst one can expect changes in the asset mix – likely away from bonds and into equities – the broader picture won’t change that dramatically anytime soon. The bond vigilantes are MIA. In the meantime, the growth impact of expansionary fiscal policy will be very meaningful…the CBO estimates a real GDP impact of +0.5% over the decade horizon, but more importantly for investors, this is front-loaded with peak impact coming in 2026 at +0.9%. On top of this, private sector investment in AI is likely running at ~$600bn, combining both hyper scaler capex and broader private initiatives. One can easily surmise a significant forward tailwind to short-term growth through this capex channel, and then furthermore via the productivity route in the coming years. All of this leaves me bullish growth in 2026, and I expect forward-looking equity markets to look through any short-term noise. If they do not…buy the dip.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/