-

Who We Are

- What We Do

Series: Some Macro ThoughtsLooking Through the Noise…Still Upside

By Nohshad Shah

EQUITY MARKETS HAVE PERFORMED WELL (SPX +20% from the April lows) as the forward-looking outlook for US economic growth improves. One by one, the roadblocks (often policy-induced) have been removed…some by the market, some by US institutions pushing back against The Executive. This week’s big news was the US Court of International Trade ruling that President Trump’s “liberation day” tariff scheme was illegal. The federal court ruled that POTUS does not have the authority under the International Emergency Economic Powers Act (IEEPA) to impose the sweeping tariffs outlined on 2 April. The judgement impacts both the 10% baseline tariffs, as well as the higher reciprocal tariffs…but not the sectoral ones imposed on steel and automobiles. However, a US federal appeals court swiftly provided a reprieve on Thursday, putting the ruling on hold in an “administrative stay”, whilst the merits of the arguments are assessed. The Federal Circuit ruling effectively freezes tariffs where they are, without making a judgement on the case itself. Open questions remain as to what happens next…with discussions around alternative provisions (Section 122) that might be used to affect the same outcomes…and ultimately if the Supreme Court will uphold the CIT’s verdict or allow for a broader interpretation of Presidential authority. As with legal cases during the Biden administration, I would expect this saga to run for months…and in the meantime, the Administration’s negotiating hand vis-à-vis trading partners would appear to be substantially reduced. Whilst it’s still likely that the baseline 10% tariffs will ultimately hold, it’s difficult to see countries succumb to “Art of the deal” tactics, when US domestic courts are tying the Administration’s hands. In any case, the broader point for markets here is that the extreme tail risks around negative economic shocks are receding fast. Whilst not providing a clear picture, this week’s announcement is, at the margin, better for growth and better for inflation. In the short-term, the risk is for a Goldilocks environment for equities. Indeed, Nvidia’s quarterly results reporting a ~70% YoY surge in revenues was a timely reminder of the underlying strength of US technology companies. This has been the most unloved rally in risks assets in recent memory, largely because of policy uncertainty, which has been tricky to navigate. But…as I have been repeating for many weeks…WATCH THE RIGHT TAIL.

FISCAL IS THE DOMINANT POLICY LEVER FOR MARKETS…and this week’s developments continued to push on the theme of greater budget deficits. When President Trump’s bill passed through the House of Representatives, the assumption was that tariff revenues would offset some of the ~$3.8tn increase to the deficit over ten years. Estimates varied broadly, with anything from $200bn to $400bn a year being discussed. But now, if this number is substantially lower, then we should expect the deficit will expand further. Similarly, Elon Musk stepped down from his cost-cutting role at DOGE this week. Having originally planned to cut ~$2tn from the annual federal budget, thus far the department has claimed only $175bn in savings, much of it difficult to verify. Ultimately, this represents a missed opportunity…whilst some will have found his style objectionable, there’s no doubt that Musk highlighted egregious levels of waste within certain areas of government and shed light on vested interests entrenched within Washington. The fact that he was unable to make any headway tells you what a tall order it is to tackle public sector spending in the USA. All of this adds further pressure to budget deficits, which are now likely to hit ~7% of GDP…meaning that long-end bonds are unlikely to rally anytime soon. Whilst I was correct in my forecast last week that the bond market sell-off would stabilize into month-end (with re-balancing flows and heightened short positioning), it’s reasonable to expect over the medium-term that investors will continue to demand an elevated premium with the current backdrop. Foreign demand will not be helped by a provision (Section 899) in last week’s bill that allows the US to impose additional taxes on investors from countries that it deems to have punitive tax policies – something to watch, for sure, as this legislation continues its passage through Congress. As mentioned last week, however, my belief is that the US economy can handle higher yields, as evidenced by the robust growth picture over the last couple of years…so long as we don’t see a dramatic sell-off (the speed matters), I do not expect current yields to be a hinderance to economic growth or equity markets. Financial conditions remain relatively easy (chart below) with the weakness in the US dollar offsetting some of the impact of higher yields…indeed if the dollar continues to depreciate, then this becomes a meaningful forward tailwind for growth as it offsets the “typical” drag you’d expect from higher bond yields thereby increasing the fiscal multiplier compared to the past.

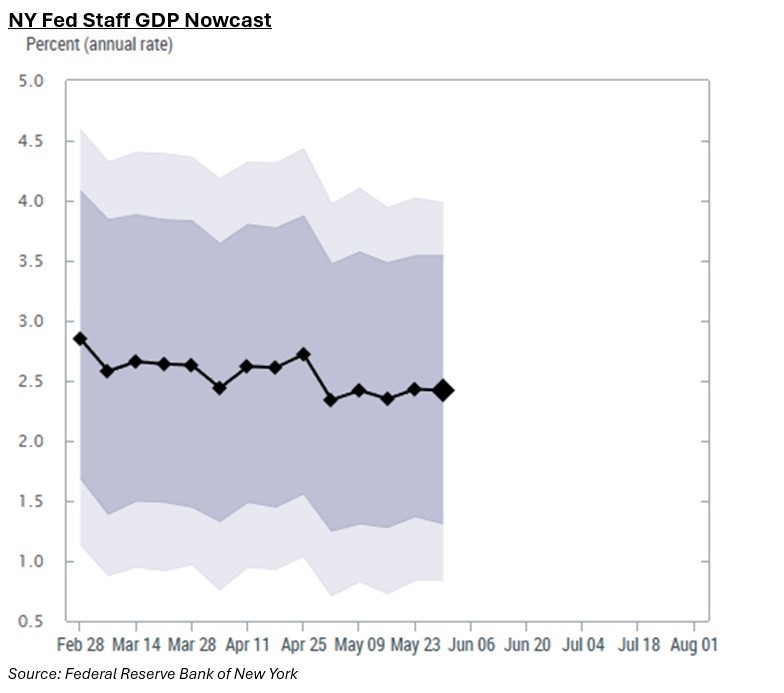

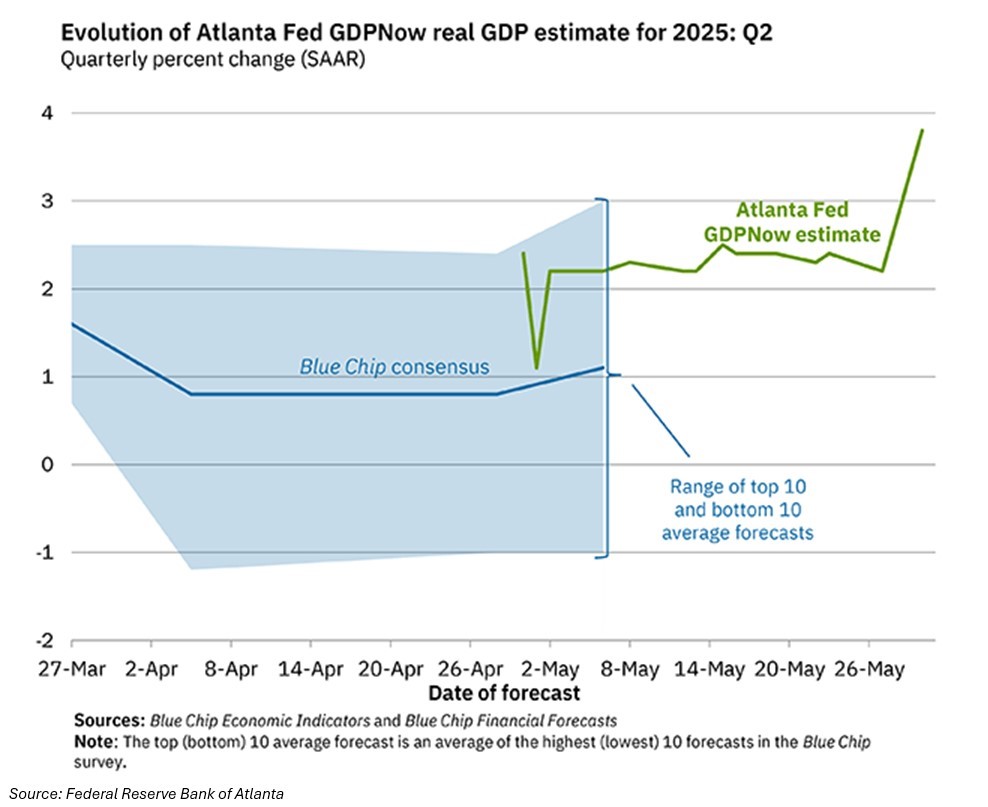

TREASURY SECRETARY BESSENT’S comments of the importance that “the economy grows faster than the debt” were important. This is the revealed preference of this Administration – the US must grow its way out of the debt. Accordingly, it’s very clear to me that there will be no course-correct on the fiscal trajectory from President Trump…the plan is to cut taxes, reduce regulation and lower energy prices to allow the US economy to do what it does best – innovate and expand. Part of the deregulatory agenda are two important proposals…first, changes to the supplementary leverage ratio (SLR) used to regulate banks, which should allow banks to hold more Treasuries by reducing capital requirements…and second, stablecoin legislation (part of the Genius Act) which encourages issuers in this space to hold T-bills. Both pieces of legislation should help support bond markets at a time of heightened issuance…however, the long-end will remain difficult as even these changes have a heavy emphasis on short-end duration. So, the playbook is clear…run the economy hot and grow your way out of debt troubles…whilst using parts of the regulatory toolkit to keep bond vigilantes in check. Well…as I’ve been arguing for many weeks, the growth picture is becoming clearer…both the top-down NY Fed GDP Nowcast and the bottom-up Atlanta Fed equivalent have US Real GDP tracking at 2.4% and 3.8% respectively (charts below)…not too shabby. This week’s Conference Board Consumer Confidence numbers showed a sharp reversal from the lows…as expected following the relief induced by President Trump’s reversal on tariffs. I would expect the hard data to follow this, but more importantly for market participants, the forward-looking outlook for risk assets will only continue to improve with incoming fiscal expansion and productivity gains unleashed from A.I. innovation in the coming 12-18mnths. In my mind, it’s very likely that trade policy will become a minor blot on the broader landscape of US growth dominance.

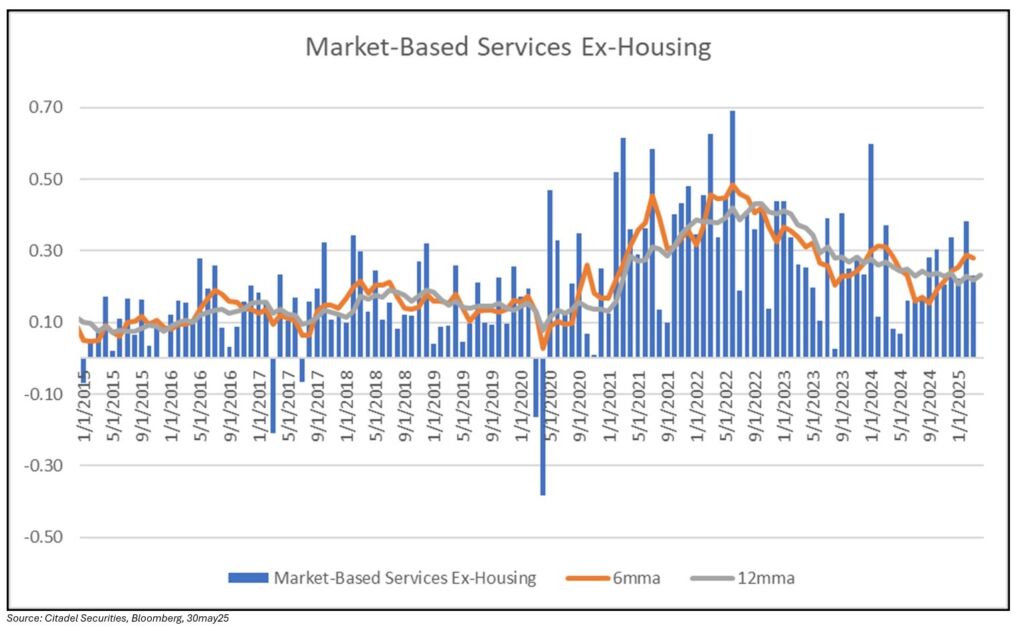

SO, WHAT’S THE CATCH? Inflation continues to remain elevated. Whilst at the top line Core PCE came in line with expectations (0.1% MoM, 2.5% YoY)…our inflation expert Durham Abric noted a drop in portfolio management fees was the driving force behind the moderation (which the Fed will care less about) and market-based core came in at 0.252% (3.07% annualised), which is not exactly cool. Moreover, Market-based Services Ex-Housing (Supercore), once the metric du jour, came in at 0.25% in April and maintains a 6mma of 0.27% (3.3% annualised) – that’s similar to levels we saw in April 2024 and higher than the average reading over the last two years – chart below. It’s hard to call that progress. If the economy is about to accelerate, these are not pleasing numbers for the FOMC. Chair Powell has rightly guided policy firmly to an on-hold stance…something which will not change anytime soon and I do not expect rate cuts in 2025. What’s more interesting perhaps, is what happens as he leaves the playing field…traditionally, the Chair sets the direction of travel and policy stance ahead of his departure – most transitions usually incorporate continuation of policy, at least for some months. If the bullish economic backdrop I’ve outlined materialises, then it would be natural for most central bankers to have a hawkish bias…which would stand in stark contrast to both President Trump’s preference…and likely the next Fed Chair. We shall find out what happens soon enough…whilst there’s no specific timeline, I wouldn’t be surprised to see a name soft proposed as early as late summer. Governor Kugler’s term ends on 31 Jan 2026…and her replacement will likely be the next Fed Chair. Another (unprecedented in 70 years) possibility is Powell remaining on the board, just not as Chairman…perhaps to monitor developments. Lots to play for. For asset prices, I remain of the view that equity markets should continue to perform well in this environment, buoyed by expansionary fiscal policy, steady interest rates, and deregulation…even more so as tail risks around policy-induced negative economic outcomes recede. In foreign currency terms, US equities are even more attractive given the circa 8% depreciation of DXY YTD. I would be a buyer.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Market Insights - What We Do