-

Who We Are

- What We Do

Series: Some Macro ThoughtsMisson Credible, Not Mission Creep

By Nohshad Shah

STOCKS AND BONDS REMAIN HEAVILY LEVERED TO THE US MONETARY POLICY OUTLOOK – SOMETHING WHICH I MENTIONED IN THIS NOTE LAST WEEK. December’s Fed meeting will be one of the most contentious in some time…but it looks like Chair Powell will eke out another rate cut despite significant reservations from a substantial portion of the FOMC…in keeping with the consensus-building approach that has defined much of his tenure. Looking forward, the key question will be the extent to which guidance from next week’s meeting will endorse the ongoing ‘normalisation’ of policy rates currently discounted by markets in 2026 (a further ~60bps of cuts). Should the FOMC deliver a hawkish cut, as I expect, it will likely do so through an SEP which sees only one (or zero) further adjustments to the policy rate next year and a shift in the language of the statement. Currently the statement reads “In considering additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks”…in December 2024 when the Fed delivered the last of its adjustment cuts before pausing for 9 months, it changed the statement to “in considering the extent and timing of additional adjustments to the target range for the federal funds rate”. I’d expect similar language this time around and would highlight the many parallels with the Dec‘24 meeting, which saw a final cut delivered alongside hawkish guidance, whilst the market expected further rate cuts. SPX sold off 3% during the hawkish presser…this is clearly a risk this time too.

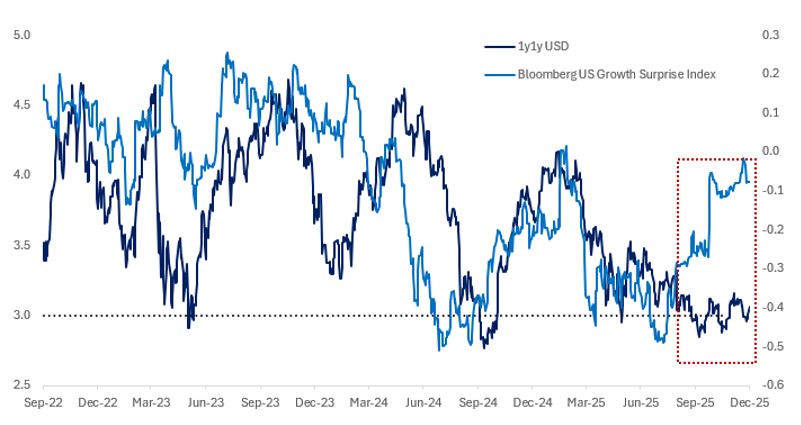

1y1y USD Swap; US Growth Surprise Index

Source: Bloomberg, Citadel Securities

MARKETS CONTINUE TO FIND COMFORT IN THE IDEA THAT EVERY CUT THE POWELL FED IS UNWILLING TO DELIVER CAN BE FORCED THROUGH BY THE PRESUMPTIVE FED CHAIR NOMINEE KEVIN HASSETT. However, this is not entirely clear for a number of reasons. The extent of division in the Fed around the December meeting, which is likely to see a number of dissents, comes at a level of policy rates that most FOMC participants see as restrictive (though they may disagree on the extent). With each passing rate cut, we get closer to most participants’ expectation of neutral…indeed after this month’s move, we will be close enough to neutral that the bar for additional adjustments will naturally rise. So, the question becomes, is there support for moving policy rates into stimulative territory? On the current evidence, this is difficult to argue – barring a much more significant deterioration in the labour market – with underlying inflation close to 3%, strong forward growth and loose financial conditions. Moreover, in a scenario where the labour market picks back up next year…which is not unreasonable given the extent of fiscal and monetary stimulus in the pipeline…and if inflation remains sticky as expected to due to ongoing pass-through from tariffs (and constrained labour supply)…I struggle to see how the new Fed Chair can garner enough support for much more rate cuts if the macro data does not warrant them. Looking at the maths of the Committee, let’s assume in the most dovish scenario that Cook, Powell and Barr all leave the Board of Governors and are replaced by Hassett and two additional doves. The remaining permanent voters are Williams, Jefferson, Bowman, Waller and Miran. Assuming Hassett, Miran and the two new Trump appointees all vote together in favour of rate cuts regardless of the economic data, they are still two votes short. Bowman and Waller are credible central bankers that will likely not vote for dovish policy unless warranted. In a scenario where Cook and Barr remain on the Board, then the ability of the new Fed chair to push through dovish policy is even more limited. The regional Fed president rotation sees Hammack and Logan rotate in as voters next year, two of the most vocal hawks on the committee. They will likely oppose inappropriate dovishness, as would Jefferson and Barr. In sum, this means Bowman, Waller, Williams, Jefferson, Barr, Logan and Hammack will all be committed to keeping Fed policy appropriate to a reasonable interpretation of the economic data. That is 7 of 12 voters…so regardless of the Chair’s views, if the data doesn’t warrant rate cuts, they will not happen. The next important point is that the Hassett himself is a credible and credentialled economist. He has however, been politically very aligned with President Trump and hence the market has naturally assumed he will deliver the dovish shift in monetary policy that the Administration has been pushing for. The issue here is not one of credibility, but of central bank independence from politics. Regardless, a new Fed Chair needs to forge consensus to ably deliver a dovish shift. Even if we assume cuts in policy rates down to neutral next year…anything beyond this will be a function of both the prevailing data, as discussed, but also the level of neutral. If real neutral rates are 1% and inflation were at target, a reasonable estimate of neutral is 3%. However, underlying inflation is running at 2.75%-3.0% suggesting that policy may already be about to be cut below the nominal neutral rate (3.75%). Even if we assume that the real neutral rate is as low as 0%…and keeping underlying inflation at 2.75%…there still remains relatively little room beyond which even an effective dovish Fed chair can cut without being at real risk of causing a resurgence of inflation, especially with terminal rates pricing in a tight 3-3.25% range in recent months. As I stated last week, this is less about dismissing the possibility of rate cuts in a weakening macroeconomic outlook and more about highlighting that it will not be trivial for the new Fed Chair to simply adopt a dovish stance in the face of an improving growth, labour market and elevated inflationary landscape.

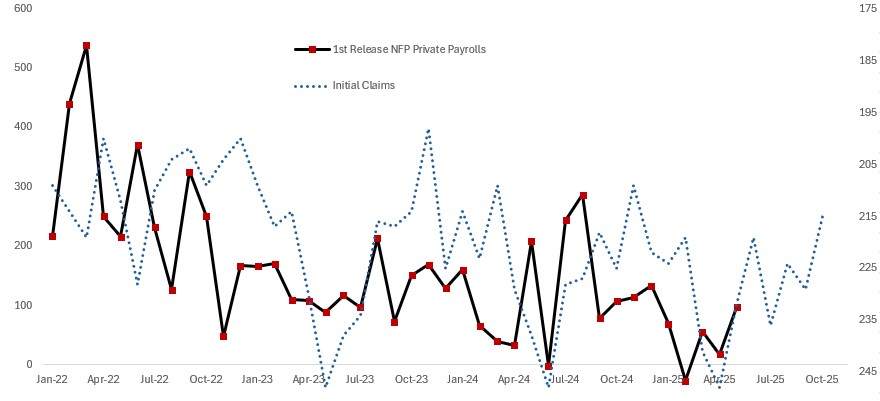

NFP Private Payrolls; Initial Claims (4wk avg. inverted)

Source: Bloomberg, Citadel Securities

THIS IS NOT ONLY ABOUT THE FED CHAIR, BUT A BROADER RE-CALIBRATION OF THE ROLE OF THE FEDERAL RESERVE. Treasury Secretary Scott Bessent has been critical of the regional Fed presidents this week, suggesting he would veto nominations of those who haven’t lived in the district for three years. The criticism seems to be in response to several Regional Fed President speeches, which made clear their opposition to rate cuts. Adding a residency requirement for regional bank presidents likely speaks to the Administration pulling every lever it can to exert further control over the central bank. Secretary Bessent has accused the Fed of “mission creep” – a criticism of the growth of activities undertaken by the Fed beyond monetary policy with operations such as QE (which he describes as a “gain of function monetary policy experiment”), the expansion of regulatory and supervisory powers, institutional complexity, and distortional effects from policy outcomes. It is certainly true to say that the role of central banks has become increasingly crucial in recent decades, and extraordinary measures have been implemented to face-off unique challenges, leading to a more expansive role for the Fed (and its equivalents in Europe). But having seen multiple crises play out through the lens of a trading floor, I can only imagine how much worse the economic outcomes would have been in the absence of central banks intervening – in a timely and credible manner – to prevent the worst case from materialising. The economic pain for citizens (that was averted by central bank actions) of mass banking failures, debt deflation and liquidity crises seem to have been forgotten in the appraisal of the Fed’s gain of function policy. One could argue that these competent and credible technocrats stepped in when politicians could not or would not. The assertion of political control over the Fed speaks to a belief held by some in Unitary Executive Authority, which suggests that all aspects of the government should be under the control of the Executive branch, ultimately answerable to the President. But the most fundamental mission of a central bank is to maintain credibility in tackling inflation – something which when lost, is difficult to regain. In simple terms, when faced with the risk of inflation de-anchoring, they have to do the unpopular thing: raise rates and tighten financial conditions to constrain economic activity and prevent a spiralling of inflation expectations – something which risks creating harsh and unpredictable outcomes. This is only possible because central bankers are not beholden to election cycles and the short-term views of the politicians that appoint them (and set their mandate). Markets remain a discipling force, and I hope that the authority of the bond market will protect central bank independence…because without it, history cautions that the economic outcomes are not favourable.

US Cyclicals v Defensives; USD 1y1y Swap

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Market Insights - What We Do