-

Who We Are

- What We Do

Series: Macro ThoughtsPlaying to Lose (Reserve Status)

By Nohshad Shah

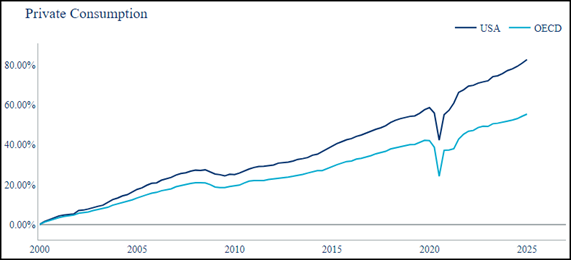

SINCE THE PEAK IN JANUARY, THE BROAD DOLLAR INDEX DXY IS DOWN ALMOST 10%…about half of that since “Liberation Day”. This reflects the Trump Administration’s new trade policies and is a natural consequence of their desire to eliminate the US trade deficit. An abrupt re-ordering of global trade in this way necessitates the unwind of the US capital account surplus as foreign countries have less dollars to recycle back into US assets. At the most fundamental level, this is a risk to the dollar’s reserve currency status…something which has benefitted the US for roughly 100 years. That benefit has come in the form of lower financing costs (used to fund deficits)…higher equities (wealth creation)…and tighter credit spreads (for corporates). These factors, plus global leadership in tech innovation…the world’s best academic institutions…being a magnet for global talent…and the rule of law with independent institutions, have combined to ensure that the US has been the most competitive place on earth to do business and growth has exceeded most of the developed world by a wide margin…a.k.a. “US exceptionalism”. Indeed, in the post-covid years with the onset of AI, it seemed as if the private sector was pressing home it’s competitive advantage – playing to win. This is most vividly on display when looking at Private Consumption in the US vs OECD averages, which shows a dramatic gap having opened up in recent years (chart below; h/t Grant Wilder). The story is simple…US households have been a massive beneficiary of globalization – one can argue about the distribution of this amongst the population – but in aggregate, this is a fact.

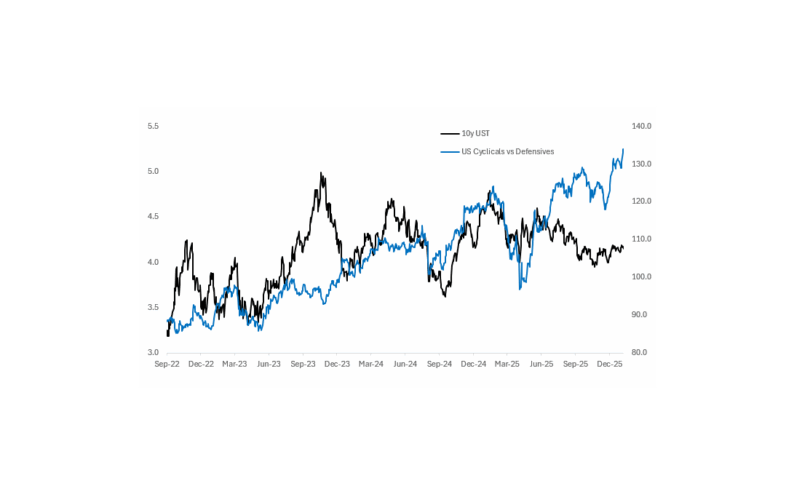

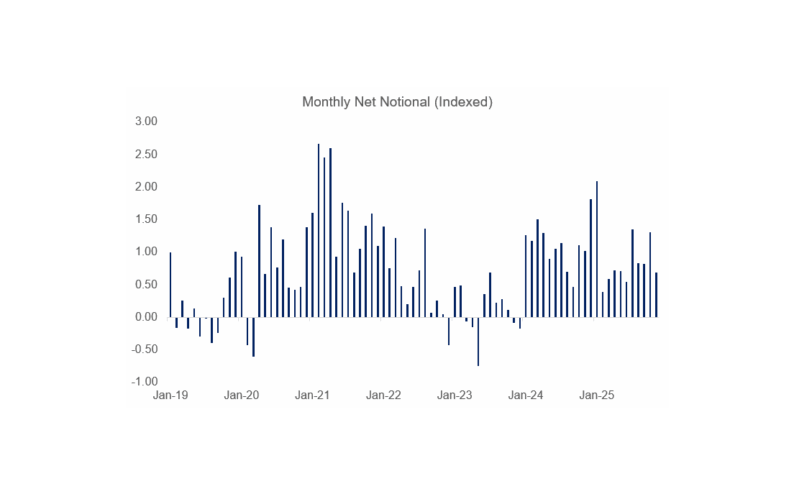

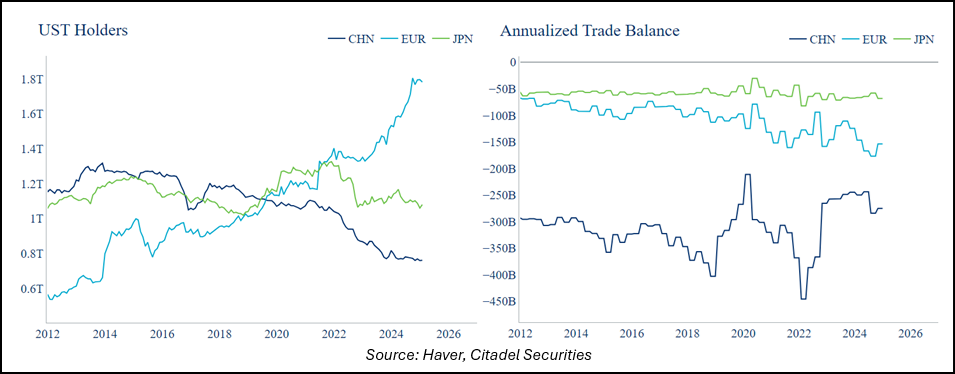

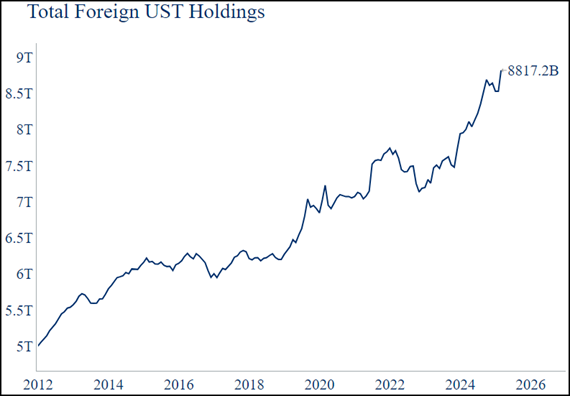

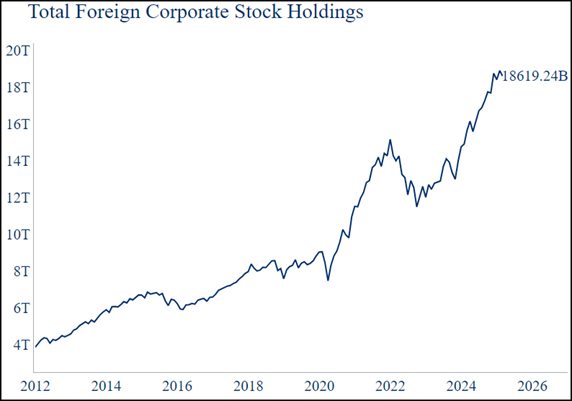

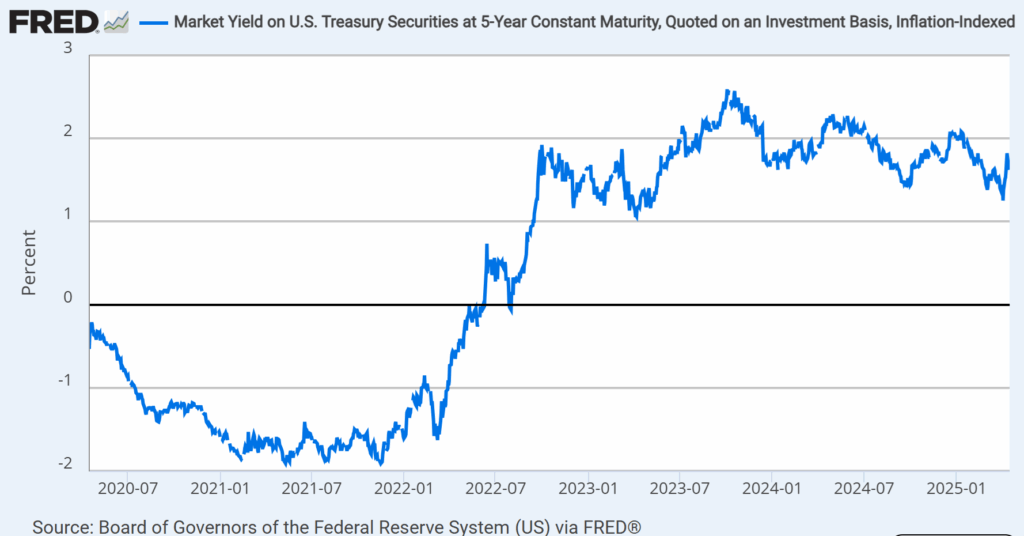

WHAT ARE THE IMPLICATIONS OF AN UNWIND OF THIS…EVEN PARTIALLY? The foreign ownership of US Treasuries stands at just under ~$9 trillion (chart below), having experienced an upsurge in the last 5 years…at the same time net issuance has gone up to $1.5 trillion per year. Similarly, ownership of US equities by foreigners has risen to ~$19 trillion. Given the magnitude of these numbers, any dent will cause a sharp correction in the price of USTs and equities…which is what we are starting to see. Thus far the most acute impact has been the sharp underperformance by ~10% of the USD versus the other global safe-haven currencies CHF and JPY since the beginning of the year. US assets have benefitted from 20 years overinvestment…an unwind will be painful and not without casualties. In a mirroring of trade balances, capital flows out of US assets will benefit foreign ones…but to be clear, de-globalization is negative for global growth. So ultimately, the policy response from the EU, China, and the other major trading nations will determine future returns for investors. As mentioned in prior notes, I expect a meaningful fiscal policy response from most of the major blocs. Domestically, what’s interesting is the move in real yields…having initially sold off sharply in response to the tariff announcements (in line with risk assets, a typical correlation), they have now stabilized with 5y real rates ~1.60%. In an environment of lower growth and higher inflation, inflation-protected yields stand out as attractive and I would expect them to perform well over the medium term (chart below).

Source: Haver, Citadel Securities, 17apr25

Source: Haver, Citadel Securities, 17apr25

Source: Haver, Citadel Securities, 17apr25

GLOBALIZATION INCORPORATES THE EFFICIENT ALLOCATION OF RESOURCES ACROSS COUNTRIES…if you believe in free markets, the less government intervention, the better. As mentioned last week, the US has been one of the primary beneficiaries of this world order, creating a productivity boom which has improved living standards for the majority of its population. Tariffs are a supply-side stagflationary shock… re-shoring labour-intensive supply chains will come at the cost of higher value-add activities with business investment reflecting this shift. A less efficient allocation of capital and labour will lead to lower productivity, lower trend growth and higher inflation…for a given level of GDP growth. On a practical level, this will have a dramatic impact on the lives of ordinary Americans in terms of their consumption of goods…~80% of air conditioners, ~70% of mobile phones and ~60% of shoes are made in China…now, with a tariff rate of 145%(?!)…you do the math. And that’s before you get into a discussion of component manufacturing, raw materials and ingredients for pharmaceuticals. Could these goods be made in the USA? Possibly, but it would take a lot of time, expertise, and adjustment in business investment. And this is the hub of the issue…it is not just an issue of the price of labour, it’s a question of quantity. Does the US have the scientists, the engineers, the mechanics and the broader skilled and unskilled labour in adequate numbers required to produce these goods at scale? Given the makeup of the US economy in recent decades with the emphasis on knowledge workers, I have my doubts. Countries like China and Germany have invested for decades in skilled manufacturing to be able to produce everything from children’s toys to EVs to semiconductor chips at scale. It would take the US economy many years to re-orientate their education system and structure of society to compete. As an interesting sidebar, in a Cato Institute poll when asked whether the country would be better off if more Americans worked in manufacturing, 80% responded in the affirmative…but, just 25% agreed that they would personally be better off in a factory instead of their current work. Quite.

WHERE DOES THAT LEAVE POLICY? A supply-side stagflationary shock of large-scale tariffs challenges both sides of the Fed’s dual mandate. This was confirmed this week by Chair Powell: “The administration is implementing significant policy changes and particularly trade is now the focus. The effects of that are likely to move us away from our goals.” and “the same was likely to be true of the economic effects, which will include higher inflation and slower growth”. With estimates of Core PCE running above 4% (2% above the Fed’s target) under most tariff scenarios, it makes sense that Powell’s leaning is towards caution. On the employment side of the mandate, the hard data remains fine…but at this point is lagging far behind the rapidly changing news flow. High-frequency data we are tracking shows consumer front-loading in goods ahead of tariff-implementation, which has supported the consumption data in March and will likely bleed into April as well, coming at the expense of services. Once that’s done, it’s reasonable to expect a sharp deterioration, matching some of the survey consumer confidence data, which has displayed historical levels of weakness. If forced to choose between the employment and inflation sides of the mandate, Chair Powell gave a hint as to which way he would lean: “without price stability, we cannot achieve long periods of strong labour market conditions”. In my mind, he does not want to repeat the mistakes of past Fed Chairmen who reacted to supply-side shocks with rate cuts, only to exacerbate inflation and have to hike rates again sharply thereafter. But there’s more at risk here…IF President Trump does indeed proceed with a full-fledged re-ordering of global trade…AND the US dollar (and assets) faces outflows as a consequence…AND we have inflation running much hotter than usual…AND deficits remain at record levels with further tax cuts (something I predict will come to the fore very soon)…then cutting policy rates in this environment risks de-anchoring the US Treasury market. 30yr USTs at 6%?…I should hope not. Chair Powell knows this…which is why he will want to wait until there’s much more clarity around where these tariffs settle and the economic implications. This is not the regular Playbook. In sum, this leaves me with the conclusion that Fed policy will be on hold through summer…enough time for some deals to be struck on tariffs and for the hard data to reveal the extent of the damage to the economy. Powell can play the waiting game, knowing that he can cut deeply…with 50bp increments if warranted…later in the year.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Market Insights - What We Do