U.S. equity options volume reached a new all-time high in May, with average daily volume surpassing 73 million contracts at the OCC. Retail activity also climbed to record levels, but unlike previous surges driven by speculative trading in smaller single-stock names, this wave of activity was concentrated in the market’s largest and most influential companies.

The same mega-cap technology and semiconductor stocks that drive index performance became the primary targets of retail call demand, reinforcing the link between investor positioning and market returns. As investors continued to chase upside in the market’s biggest winners, equities experienced one of the most extreme “spot up, vol up” environments on record – a dynamic that has extended into the first trading sessions of June.

As the #1 US retail market maker executing approximately 35% of all US-listed retail volume[1], Citadel Securities has a unique vantage point on retail investor behavior and the market forces shaping price action. This perspective provides valuable insight into how retail flows are influencing both individual securities and broader market performance.

Record-breaking Retail Options Volume

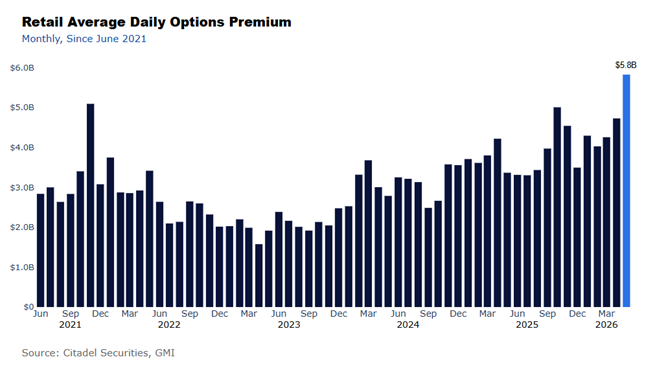

Average daily options volume on the Citadel Securities retail platform reached a record high in May, a 20% jump from the trailing one-year average and besting the previous October 2025 record by 4%.

Retail investors traded a record $5.8 billion of options premium per day during the month of May on our platform. Positioning was heavily skewed toward upside exposure, with calls accounting for $4.3 billion of daily premium traded (73%).

Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

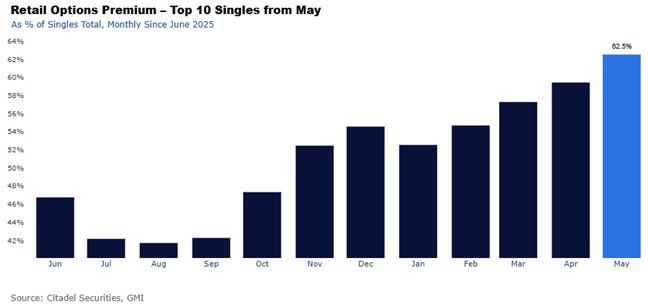

Activity was also unusually concentrated. Retail investors’ ten most-traded stocks accounted for 63% of all single-stock options premium traded, led overwhelmingly by mega-cap technology and semiconductor names. Just one year ago, that share was less than half the total traded premium, highlighting their increasingly narrow focus.

The composition of activity was as notable as its magnitude. During the meme-stock rally of 2021 and the volatility-driven surge in October 2025, retail flows were focused on idiosyncratic single-stock stories often driven by short-squeeze dynamics. In May, retail investors instead focused on the same companies driving benchmark returns and institutional positioning.

Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

The Return of Momentum: “Spot Up, Vol Up”

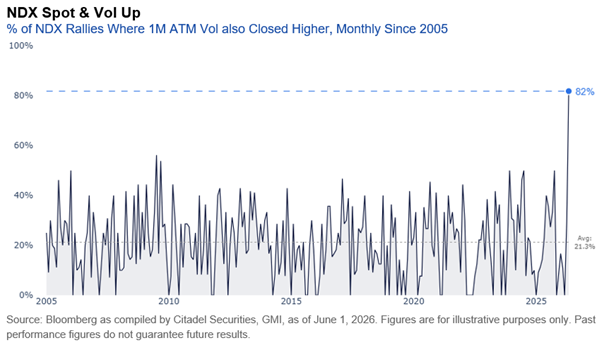

The impact of this concentration was most evident in the Nasdaq-100. Despite a relentless rally that saw the NDX close at new all-time highs on 10 of May’s 20 trading sessions (the highest frequency since December 2020), retail investors continued to add upside exposure through calls. As the index gained 10.6%, marking its second consecutive double-digit monthly advance for the first time since 2009, call demand helped reinforce the unusual combination of rising prices and higher implied volatility.

This marked a sharp reversal from retail’s behavior earlier in the year. From January through April, retail investors were typically net sellers on up days, with an average Call/Put Direction Ratio of 1.6% better for sale. In May, that pattern reversed entirely, with the average Call/Put Direction Ratio on NDX up days shifting to 1.7% better to buy.

This resulted in one of the most extreme “spot up, vol up” regimes on record – The NDX recorded nine sessions in May where both spot and 1-month ATM implied volatility rose together, accounting for 82% of all rally days during the month. That is the highest frequency observed since 2005 and compares with a long-run average closer to 21%.

If anything, the trend has strengthened in June. In each of the first two NDX rallies of the month, 1-month ATM implied volatility also increased. Retail investors were 5% better to buy on both up days (more bullish than the average May rally) suggesting the same dynamics remain firmly in place as June begins.

Retail’s Highest-Conviction Growth Themes: Semiconductors, Memory, and Space

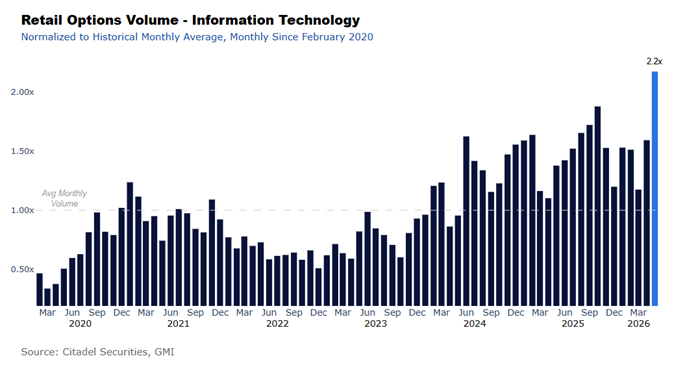

Retail options activity in the Information Technology sector surged in May, with volume reaching 2.2x its average level. More specifically, semiconductor, memory, and space-related stocks emerged as the highest-conviction themes, attracting outsized retail participation and signaling where retail volume may continue to grow in the months ahead.

Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

Semiconductors and Memory

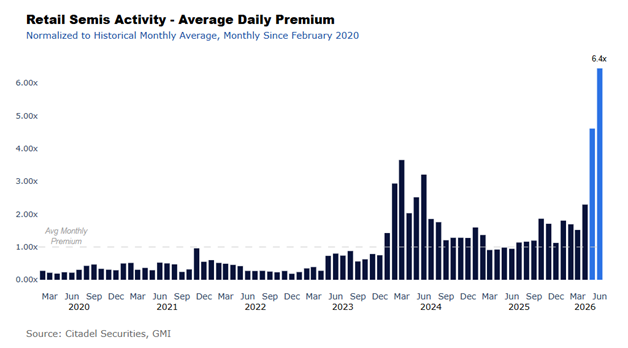

Semiconductors sat at the center of retail activity. Average daily options premium traded in Semiconductor stocks on our platform reached a record $1.6 billion in May – more than double April’s level, roughly 5x the historical average, and 26% above the previous record. The trend has accelerated further in early June, with average daily premium traded rising to $2.3 billion per day, or 6.4x the historical average. Positioning remains decisively bullish, with retail investors trading 2.2 calls for every put (83rd percentile) in the group.

Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

Space

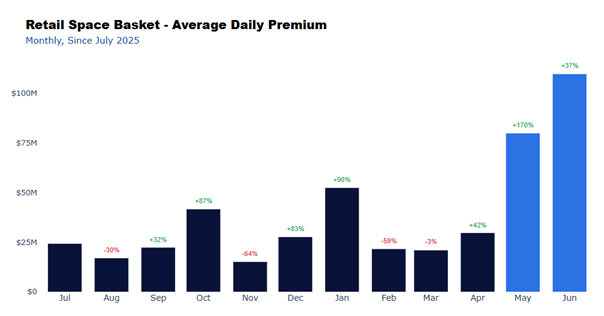

Beyond AI, anticipation surrounding the large IPOs drove a sharp acceleration in retail demand for space-related equities. Options premium traded in these stocks increased 167% month-over-month. Each exhibited an exceptionally strong call bias, with roughly seven calls traded for every put and consistently bullish positioning.

The surge drove record participation across our Space basket. Average daily options volume jumped 3.5x from its historical average. Average daily premium traded rose 170% month-over-month – nearly 10x its historical average. The momentum has continued into June so far, with average daily premium traded already running more than 37% above May’s record pace at over $100 million per day on our platform.

Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

[1]Measured based on sampled SEC 605 public reporting of executed shares of marketable orders as compiled by Citadel Securities, as of April 2026.

Copyright © Citadel Enterprise Americas LLC or one of its affiliates. All rights reserved.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CDGE”) authorized and regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch authorized and regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the Japan Financial Services Agency (“JFSA”); and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”), Financial Industry Regulatory Authority (“FINRA”), and Securities Investor Protection Corporation (“SIPC”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC, FINRA, and SIPC, or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity. Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at www.citadelsecurities.com/GlobalSalesTrading.