-

Who We Are

- What We Do

Series: Some Macro ThoughtsRotational Pain, But Fundamentals Intact

By Nohshad Shah

EQUITIES WERE UNDER PRESSURE THIS WEEK, LED BY PRONOUNCED WEAKNESS IN THE TECHNOLOGY SECTOR – PARTICULARLY SOFTWARE. The sell-off reflected a confluence of factors. First, Anthropic launched a powerful new AI model, Claude Opus 4.6, aimed squarely at enterprise users rather than consumers. This follows January’s release of Cowork, an AI coding platform designed for firms without in-house coding expertise. Together, these developments place Anthropic at the centre of potential disruption in enterprise software, raising concerns about traditional software development business models and the durability of incumbent revenue streams. The company’s decision to make open-source Cowork plug-ins freely available across wide-ranging industries could prove particularly disruptive if adoption broadens. The sharp decline in software stocks – down roughly 25% year-to-date – was likely exacerbated by crowded positioning. Second, hyperscaler capex continues to accelerate…recent Q1 results point to over $600bn of planned AI infrastructure spending in 2026, far exceeding expectations. Alphabet alone expects capex of $175–185bn, roughly double last year’s level, while Meta has guided to $115–135bn, and Amazon’s announced spending plans of $200bn were met with investor concern, driving an 11% after-hours stock decline. Only a few months ago, numbers of this magnitude…paired with strong earnings beats…would likely have turbocharged sentiment and valuations. Instead, as I’ve highlighted for some time, investors have become far more discerning, increasingly focused on return on investment and the path to monetisation as capex rises from already elevated levels. Third, persistent weakness in digital assets has likely weighed on broader risk sentiment. Since its October highs, bitcoin has fallen more than 50%, wiping out ~$2.2 trillion in market capitalisation from the broad complex. This has coincided with a broader pickup in cross-asset volatility, including in precious metals, adding to the pressure on risk assets.

WHAT TO MAKE OF IT ALL? The market is clearly penalising technology stocks for elevated capex and has rotated away from momentum and growth factors. Importantly however, cyclical stocks remain on firm footing, suggesting these moves reflect idiosyncratic risks rather than a broader reassessment of the macro growth outlook. Tech earnings remain strong, with delivered EPS beats and robust earnings sentiment underscoring the profitability of these businesses. This is not a repeat of the dot-com era: forward P/E multiples in the mid-20s are far more disciplined and balance sheets are strong. Retail investors…who have provided consistent dip-buying support in past drawdowns…also appear well positioned, with no signs of extended positioning and household balance sheets and incomes remaining healthy. In sum, the macro backdrop remains stable, the broader AI theme is intact (albeit with greater investor scrutiny), and the current combination of high-volatility factor rotations and elevated correlations should provide good opportunities. As ever, NVIDIA’s earnings in the coming weeks may once again serve as a key market bellwether.

I-Shares Expanded Tech Software ETF (white); US Cyclicals vs Defensives Stocks (yellow)

RECENT ECONOMIC DATA CONTINUE TO PAINT A BROADLY CONSTRUCTIVE PICTURE. Forward-looking indicators point to a meaningful acceleration in growth, albeit alongside some lingering concerns about the near-term health of the labour market. ISM Manufacturing rose to 52.6, a significant upside surprise versus expectations (48.5) and a sharp rebound from December’s 47.9. This marks the first expansionary reading in twelve months, with strength in new orders signalling improving demand. The message was reinforced by continued resilience in the S&P Composite PMI at 53 and ISM Services at 53.8. The sharp rebound in the Chicago PMI is noteworthy, though its signalling power in the post-pandemic period has been limited, making it difficult to place too much weight on this data point. Overall, sentiment and activity indicators stand in contrast to some of the labour-market data released this week…Challenger reported job cuts of 108k in January, a 118% YoY increase. While eye-catching, there is little evidence at the aggregate level that firms are embarking on broad-based layoffs. The JOLTS layoff rate, WARN notices and initial claims remain far from flashing red. The recent uptick in claims appears driven by a rebound from very low levels and weather-related disruptions in the Northeast. Job openings declined, though the lagged nature of JOLTS likely reflects residual effects from the government shutdown. More reliable components of the report – the quits rate, hiring rate and layoff rate – continue to suggest a stable labour market. In short, this is a labour market characterised by sharply reduced supply (from reduced migration), subdued demand, and low turnover. My view of the US economy remains unchanged: growth remains strong, with nominal GDP tracking in the 5–6% range into 2026, implying greater upside risk to labour demand rather than the reverse.

US ISM Manufacturing

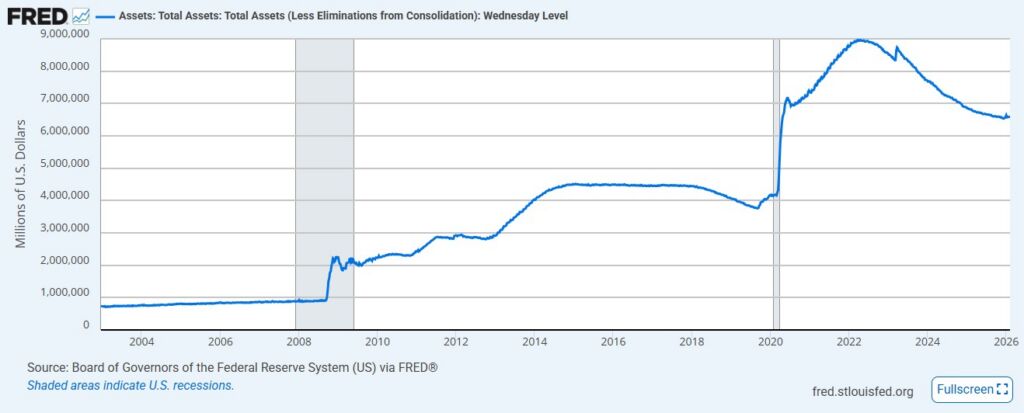

THE NOMINATION OF KEVIN WARSH AS FED CHAIR LOOMS LARGE FOR LONG-TERM MACRO INVESTORS. Last week, I noted that his selection would be welcomed by those who value the sanctity of an independent Federal Reserve – albeit one that may operate in closer alignment with political leadership. That alone reduces certain tail risks for markets. Beyond this, conventional wisdom frames Warsh as a more hawkish choice than other candidates, but the more consequential issue lies in his views on the Fed’s balance sheet. Warsh has long been a critic of balance sheet expansion and quantitative easing, arguing that they distort markets and create excessive easy money. In his view, the Fed’s $6.6tn balance sheet should be structurally smaller, with liquidity backstops remaining exceptional rather than routine. While this is a coherent and defensible framework, let’s be in no doubt that it represents a clear regime shift…one that implies far more tolerance for financial stress before Fed intervention…with meaningful implications for asset prices. Should Warsh succeed in persuading the FOMC to accelerate quantitative tightening – not a given – reserves would drain from the banking system, collateral conditions would likely tighten, and dollar funding would become scarcer. In effect, this raises the risk of a liquidity shortage that could either constrain credit supply or increase the probability of a funding-driven crisis. The implicit level of the “Fed put” would move materially lower, a potentially treacherous outcome for markets conditioned to buy the dip amidst rising leverage and record levels of UST supply. While Warsh emphasises the dangers of monetary dominance rather than fiscal dominance, the reality remains that someone must absorb the ever-expanding supply of government debt. If not the central bank, that burden falls on banks or the broader private sector. Meanwhile, the risk of an interest-rate spike driven by exogenous or endogenous shocks – such as renewed inflation pressures – cannot be dismissed. This risk is particularly relevant given Warsh’s view that an AI-driven productivity boom could allow policy rates to be cut despite above-trend growth, without igniting inflation. For now, much of this remains speculative. Still, forward-looking investors should be alert to the possibility that 2026 will mark the beginning of a new era in central banking.

US Federal Reserve Balance Sheet

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Market Insights - What We Do