-

Who We Are

- What We Do

Series: Macro ThoughtsSticky Inflation Trumps Curve Steepeners

By Nohshad Shah

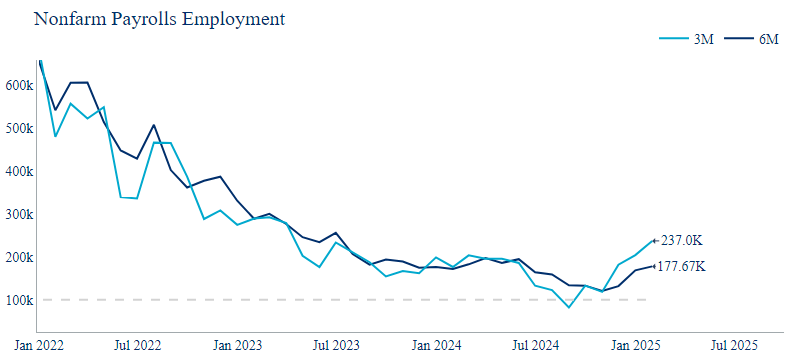

THE FED IS IN A TIGHT SPOT…tighter than their commentary (and market pricing) would suggest. Let me explain why. Despite recent signs of weakness in some of the survey data, US Real GDP has been strong throughout this cycle, staying broadly in the 2-3.5% range over the last 10 quarters…and that’s despite over 500bps of rate hikes from the Fed, trough to peak. Inflation, having receded from its post-pandemic highs, has settled in the mid-to-high 2% area over the last year. If we assume that historical assumptions of trend growth remain intact at ~1.8%, why has this level of above-trend GDP growth not generated more inflation? The answer partly lies in the labour market and the supply of large-scale immigration over recent years, which has created more slack in the economy…post-pandemic, the influx of ready-to-work immigrants significantly boosted the US labour force, with estimates of an additional 100,000 jobs per month in 2023/early 2024 (Dallas Fed). Essentially, the short-term trend growth of the economy has been higher than estimated and likely exceeded actual growth. But…recent policy changes by the Trump administration are starting to impact this trend…stricter policies have already led to a slowdown in immigration and increase in deportations, resulting in fewer entrants into the labour market…which is why we are seeing a stalling of the labour market softening that has been observable since summer 2024. At this juncture, given the growth backdrop remains robust, I see the risks of the unemployment rate dropping to 3.7% as higher than it rising to 4.3% (as the Fed expects). Indeed, if you adjust for tighter immigration policies, the breakeven level of payroll growth for an unchanged u/e rate needs to drop from ~150k to ~80k…and we’re currently running at a 3m average of 237k…

source: Bureau of Labor Statistics, 07feb25

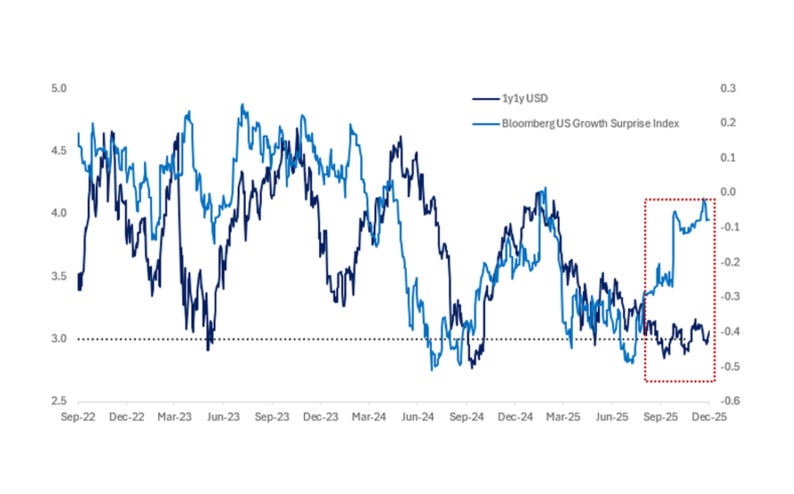

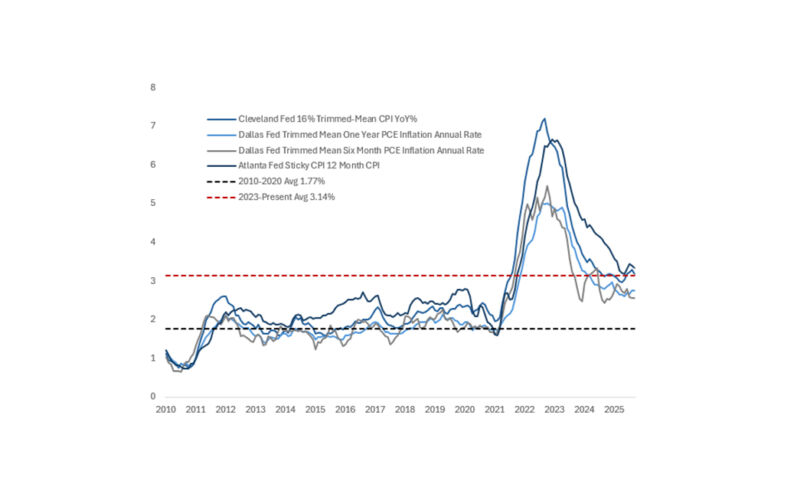

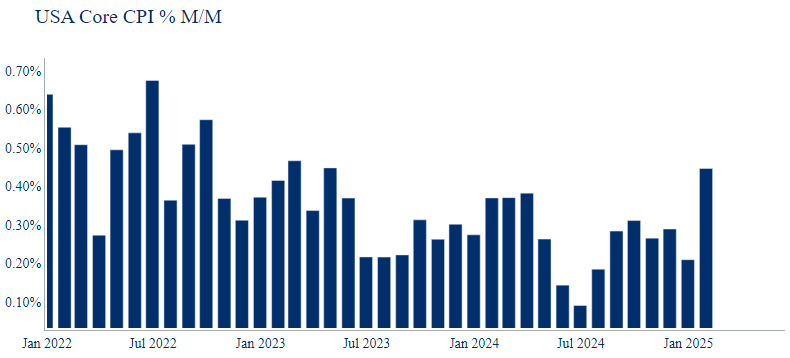

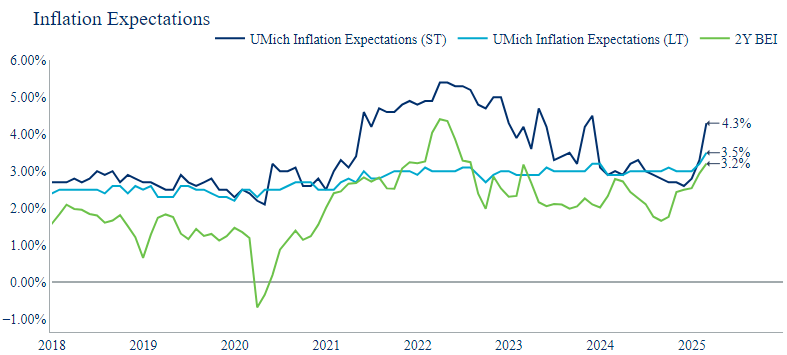

INFLATION IS THE BIGGEST ISSUE…with Core CPI coming in at 0.446% MoM SA, with strength across the components and seasonal adjustments not compensating enough. This is an uncomfortable number for the Fed…much closer to the range seen in 2022-23 than last year (chart below). Market players took comfort from the translation to Core PCE (the Fed’s preferred measure) being more benign – tracking 0.29% MoM SA and 2.6% YoY by most estimates…but I would be mindful of this as it was driven by some special items like airfares, which could easily reverse. Perhaps even more concerning, inflation expectations are rising sharply, as measured by both survey data (UMich short-term @ 4.3%; long-term @ 3.5% – highest since 1993) and the market (2y breakevens @ 3.2%)…and this is with a broadly stable backdrop on energy prices – highly unusual. All of this is prior to the new administration implementing any drastic tariff policies, with the likelihood of a one-off shift in price levels remaining high. Moreover, I would argue that a gradualist approach to tariff implementation would have the negative effects of increasing inflation in certain sectors, without the shock-and-awe impact on growth and the stock market.

source: Bureau of Labor Statistics, 12feb25

Univ. of Michigan Survey of Consumers 21feb25, Bloomberg

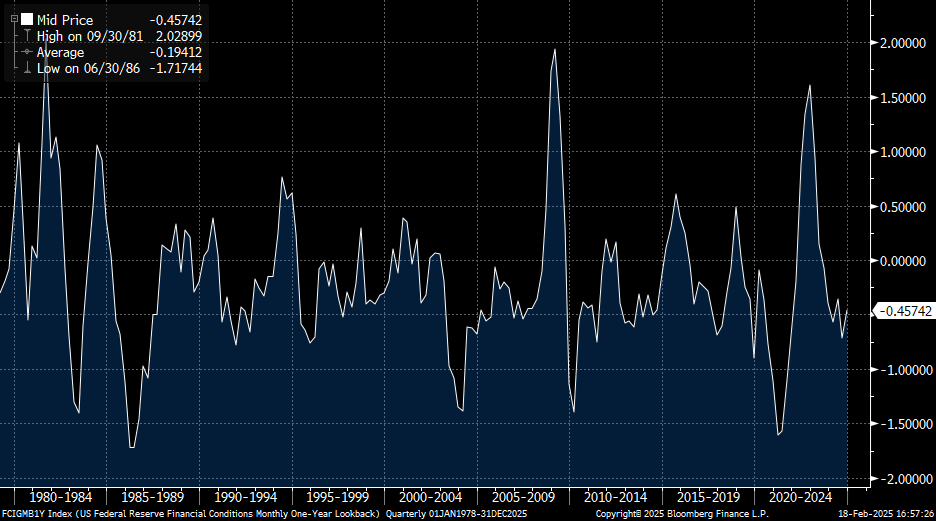

THE ELEPHANT IN THE ROOM remains President Trump’s policies, not just on trade, but for the broader economy. The starting point is deregulation – tough to model – but the direction of travel is clear. The new administration is keen to cut red tape and bureaucracy, which could easily lead to a credit-driven boost to growth. In this context, it’s important to remember that his right-hand man is Treasury Secretary Scott Bessent…an experienced market professional. This implies an inherent understanding that the long end of the curve is more important than the policy rate in terms of its impact on borrowing and the broader economy. We’ve already seen this in his comments (“we are not focused on whether the Fed is going to cut”) and market emphasis on potential changes to the Supplementary Leverage Ratio (SLR) regime, which means banks wouldn’t need to hold as much capital against Treasuries…likely boosting demand and compressing the bond term premium. Ultimately, President Trump wants to boost growth with deregulation, lower energy prices and keep long-end rates controlled…stocks up, oil down and 10y yields lower…in other words FCI easing. As a reminder, we have already unwound much of the FCI tightening driven by the Fed in 2022-23 and are moving easier…

US Federal Reserve Financial Conditions (Monthly, One-Year Lookback)

Source: The Federal Reserve Board, Bloomberg

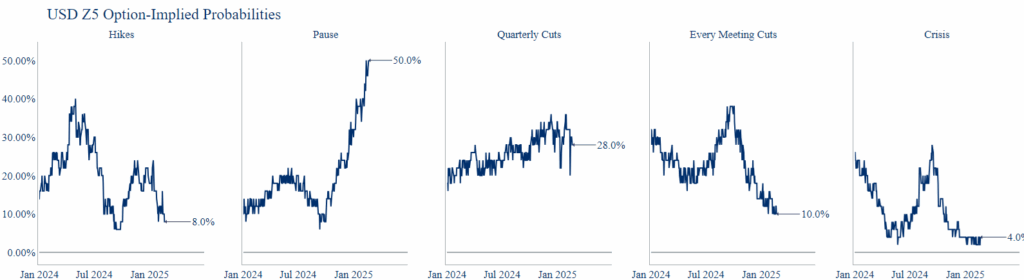

SO…HERE’S THE BACKDROP FOR THE FED: robust growth (with incoming policies likely to boost it)…a labour market that has stopped softening (with policies that are tightening it)…inflation that is somewhat stable but above target (with expectations rising and risk of tariffs)…and an action-orientated Trump administration that is determined to ease FCI. All this calls into question the monetary policy “easing bias” that the market has gotten accustomed to…the risks of Fed hikes vs cuts in end-2025 and beyond need to be much more balanced, in my view. I can envisage a scenario where government polices designed to boost growth and ease FCI start to stoke inflation back to (even more) uncomfortable levels and the Fed is forced to take back some or all the 100bps adjustment cuts made in 2024.

Market pricing does not reflect this risk. The implied probability of a rate hike in SFRZ5 sits ~8% currently (h/t: Grant Wilder), which is low…and more broadly the terminal rate sitting at ~3.90% in 2026 seems too benign for the backdrop. More interestingly, the scenario outlined above where policies are enacted to control 10y yields to create a credit-fueled expansion of the economy (alongside broader deregulation)…is one where THE YIELD CURVE NEEDS TO FLATTEN SUBSTANTIALLY, especially if the Fed is compelled to respond.

Source: Citadel Securities, 21feb25

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Macro Thoughts - What We Do