-

Who We Are

- What We Do

Series: Some Macro ThoughtsStocks – On the Button, Yet Again

By Nohshad Shah

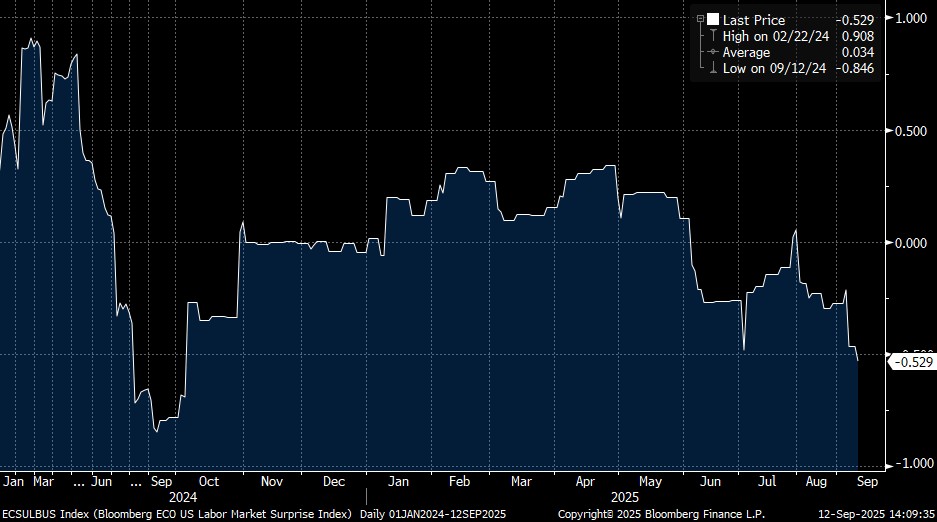

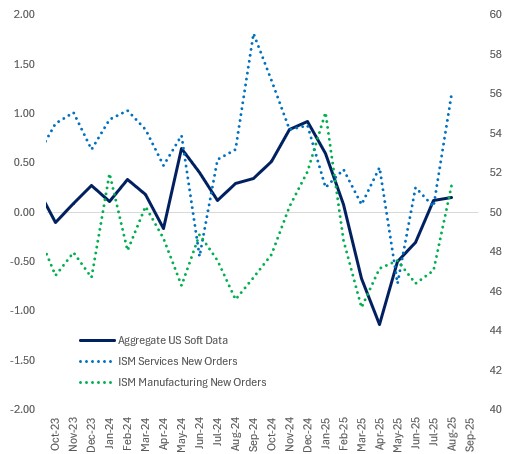

BOND AND EQUITY MARKETS ARE SINGING FROM DIFFERENT HYMN SHEETS AS IT PERTAINS TO THE STATE OF THE US ECONOMY…with 10y Treasury yields close to YTD lows ~4% and just over five rate cuts priced into the front-end, fixed income markets are concerned that economic growth will roll over in coming months. This is largely driven by the recent weakness in labour market data, exacerbated this week by preliminary QCEW payroll revisions that suggest 911k fewer jobs were created in the 12 months to March 2025 than previously estimated. This is most neatly encapsulated in Bloomberg’s Labor market surprise Index (chart below), which has taken a sharp turn lower in recent weeks. On the other hand, equity markets continue to make all-time highs…in-line with most sentiment indicators suggesting a forward outlook that is trending upwards since June. Delving a little deeper, there is a case to be made that the labour market is like an oil-tanker and once it gets moving in one direction, becomes difficult to halt. But it’s also true to say that much of this data is backward-looking into an unprecedented period of uncertainty around the economic environment, especially given dramatic shifts in trade and migration policies – both huge factors. Time will tell if the deterioration in the labour market continues, but what we do know is that sentiment amongst businesses remains robust – looking at aggregated soft data, it’s clear this has been accelerating since April’s tariff shock…especially interesting is the sharp upswing in the New Orders component of ISM (both services and manufacturing) – chart below. Notwithstanding the adage “the stock market is not the economy”, the fact remains that Q2 earnings displayed a very resilient corporate landscape…EPS growth was ~6.5% with a full 81% of S&P 500 companies reporting positive earnings and revenue surprises…with forecasts for Q3 now at 7.5%. If that materialises, it would be the ninth consecutive quarter of earnings growth and the AI capex boom is still in full swing (~$450bn for 2025), as evidenced at President Trump’s tech roundtable…and further afield – AI was cited on 287 earnings calls, the most in 10 years. So…bond markets are following the labour market data (by definition, spot)…and equity markets are reflecting the sentiment data (by definition, forward looking). Both are likely correct. I would surmise that in coming months the labour market will converge to the activity data revealing that stocks have been right and bonds are rich. As regular readers will know, my view for some time has been that whilst the spot data suggests a weak(ish) labour market and moderating growth, the forward outlook remains strong…and that’s what’s relevant for asset prices. Weakness in the labour market is relevant in so much as it accelerates and delivers significant second round effects on consumption, the backbone of the US economy. On this front, I find the comments from Alastair Borthwick (CFO of Bank of America) telling: “It has been very stable so far through the quarter and actually through much of the year. We’ve talked about the fact that last year was a record year for consumer spend in the U.S., up 3%, 3.5% on our cards. This year that’s accelerated. Last time we got together at earnings, we said it was somewhere between, you know, closer to 4.5%. It actually accelerated this year. Here we are midway through the quarter. That spending trend continues. As we look through to the asset quality, we talked about the fact that with less in the way of late-stage delinquencies at the end of Q2, we anticipated consumer net charge-offs should come down again this quarter. Generally speaking, I’d say we’re kind of on track with that. The consumer at this point appears to be exactly where we were, resilient, doing well, in a good position, and that’s reflected in our asset quality numbers”. Ultimately, whilst aspects of the labour market data suggest weakness in the economy, almost every other indicator reflects resilience…and supportive policies should ensure that follows through. The combination of easy financial conditions, the AI investment boom, broadly resilient corporate earnings, and most importantly, the pro-cyclical easing of both monetary and fiscal policy at the same time, will ensure that economic growth will not only be strong, but likely exceed trend in 2026.

Bloomberg Labor Market Surprise Index

Source: Bloomberg

Aggregated Index of Soft Data

Source: Bloomberg, Haver

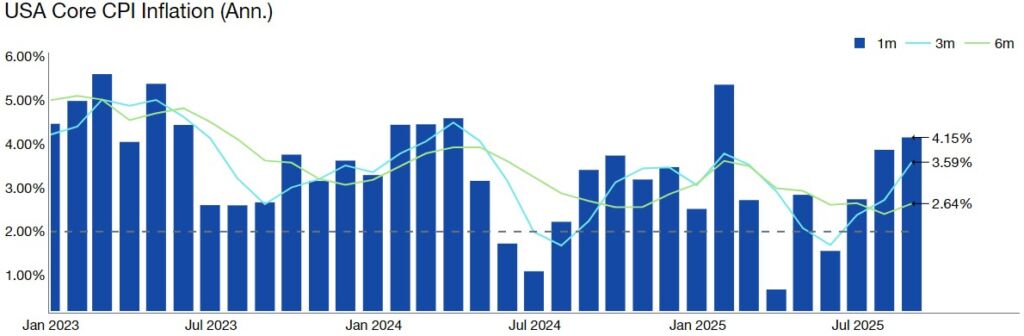

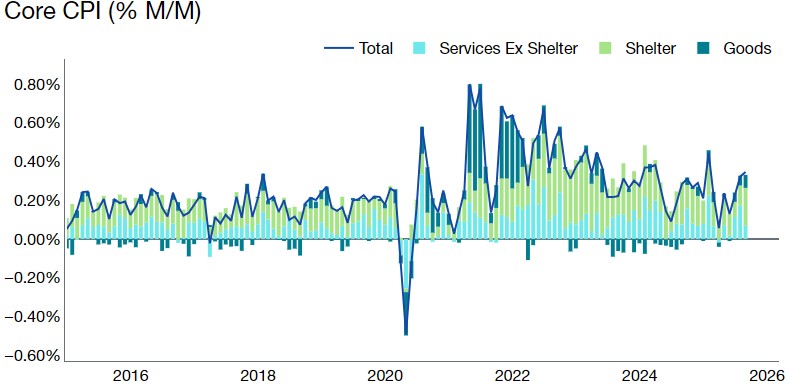

INFLATION CONTINUES TO BE A RISK. Core CPI remained elevated in the most recent August data at 0.35% MoM (3.1% YoY) and Core PCE estimates are now tracking a moderate 0.21% MoM…a relatively large wedge. This reflects concentrated weakness in software prices, which has a much larger impact on PCE than CPI. The more important point is that Core Goods remain on the soft side (0.28% MoM), reflecting a moderated passthrough from tariffs thus far. With inventory accumulation likely still playing a role, it feels like there will be a more elongated and gradual rise in prices as tariffs continue to be implemented…items like Apparel are starting to show signs (+2.2%), but the broader impact in other areas will likely be felt in coming months. However, Core Services continues to rise (0.35% MoM) with Airfares notably surging +47% annualised over the last 3 months and some impacts from tariffs coming into services such as vehicle maintenance and repair. Importantly, OER (0.41%) and rent (0.34%) both continue to show strength. And this is the problem for the Fed…if we had a sharp shock to goods prices, clearly driven by tariffs, it could easily be dismissed as a one-off price-level shift. Instead, what we have is services inflation that is too elevated and inconsistent with the Fed’s target, showing no signs of deceleration…and tariff passthrough that seems to be manifesting gradually over many months, but will still ultimately serve to push core inflation higher. Heading into next year, we could be in a situation where tariff-induced inflation is firmly kicking in at a time when growth is picking up. Not a great backdrop for the Fed’s (these days second order) mandate. Nevertheless, the FOMC has showed their hand, and I do not expect that to change in the near term – the market is right to expect insurance cuts starting in September and into the end of this year…possibly regardless of the data. I have written in the past about the importance of Fed independence…whilst some have argued that the Fed has never truly been independent, I remain of the view that it is of vital importance for markets (and by extension the US economy) that such an important institution must act independently and be seen to be doing so. Our Founder Ken Griffin highlighted this fragile balance in an OpEd in the WSJ: “Credibility in economic policymaking is built slowly, through practice and respect for processes, and can be lost quickly if those processes are disregarded. Preserving credibility is essential because it benefits all Americans by keeping the costs of borrowing money lower, supporting sustainable growth, and maintaining global confidence in U.S. institutions. Once lost, it is costly and time-consuming to rebuild. Protecting it must remain the central priority of U.S. economic policy.”

Source: BLS, Bloomberg

THE ASSET CLASS IMPLICATIONS THAT FOLLOW ARE ENTIRELY LOGICAL AND REFLECT EXACTLY THE LANDSCAPE I HAVE OUTLINED. The debasement theme remains intact – Gold is breaking out reaching $3650, up 6% MTD and a whopping 40% YTD. The broad-based dollar index (DXY), having underperformed for much of the year, is now torn between sticky inflation/a cyclical upturn versus spot concerns around the labour market and financial repression/debasement fears. I remain bullish stocks…this can be the only conclusion when you have strong revenue and profit growth…a deregulation agenda that should create supply side expansion (unlocking energy infrastructure and bank balance sheets)…company and household balance sheets that remain healthy…a record capex investment boom (not only AI)…lower policy rates…and incoming fiscal stimulus (with tariff revenue running at $30bn in August, another potential source of stimulus funds). I simply do not see the trigger for a correction, at least from the macro lens. As I’ve been saying for months – WATCH THE RIGHT TAIL. 10y USTs look rich to me around 4%…at this stage we are pricing pretty much peak dovishness relative to the current data…and if I’m correct about the forward, we should see a decent sell-off.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Market Insights - What We Do