-

Who We Are

- What We Do

Series: Macro ThoughtsStructural Not Cyclical

By Nohshad Shah

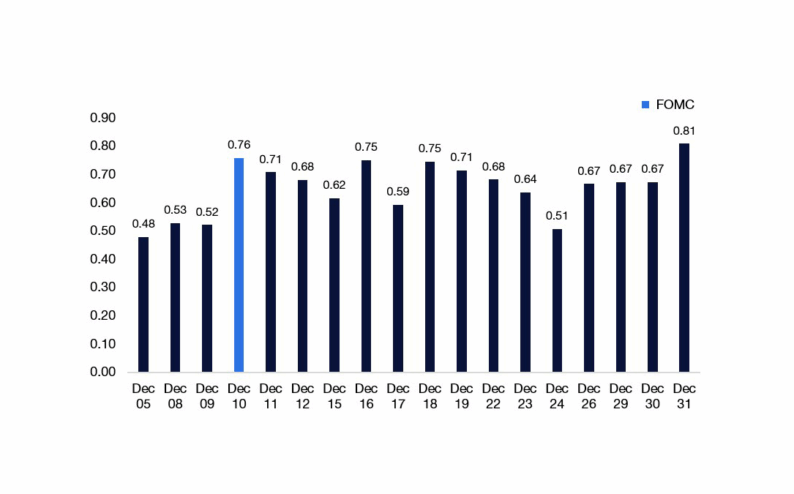

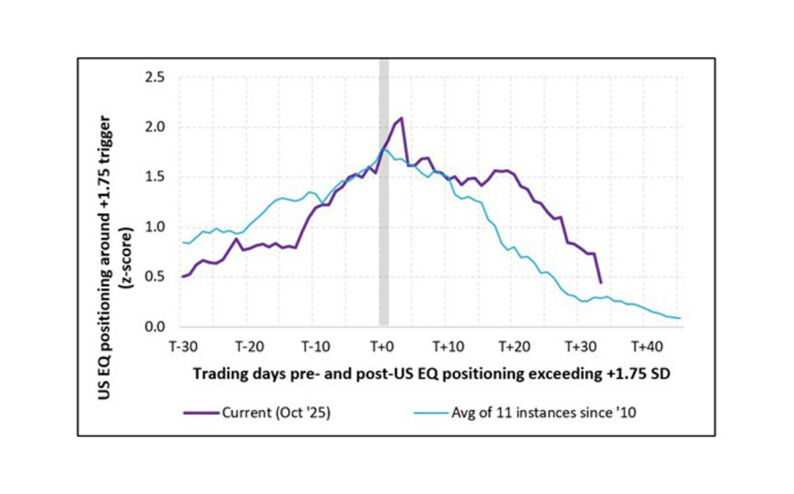

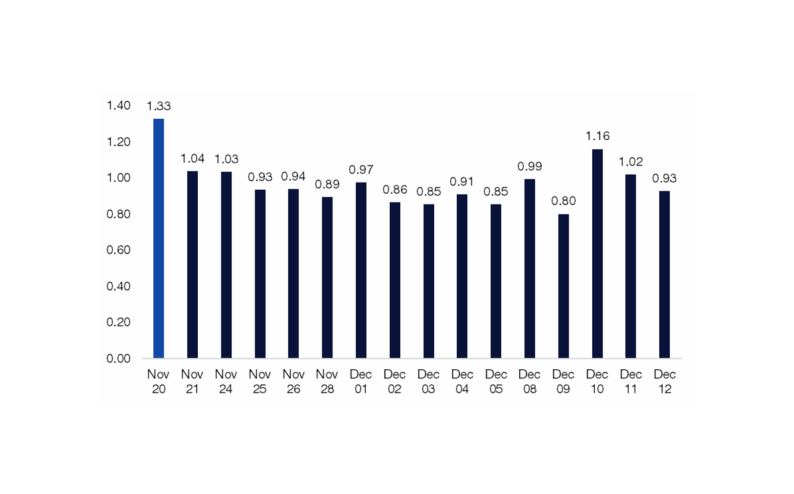

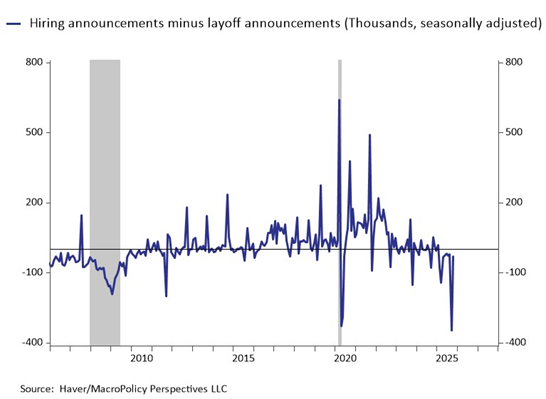

THE SUPREME COURT HEARD ORAL ARGUMENTS THIS WEEK ON THE USE OF THE INTERNATIONAL EMERGENCY ECONOMIC POWERS ACT (IEEPA) FOR PRESIDENT TRUMP’S TARIFFS…with the tone of the Justices’ questioning suggesting that the court may not uphold the authority. Kalshi pricing of the supreme court ruling in favour of the Administration dropped from 45% to 20% following the hearing. The ruling is important for both stock and bond markets as it reduces economic uncertainty and is an implied tax cut via a decline in the effective tariff rate (ETR). However, the implications are nuanced by the specifics and how the Trump Administration responds when it concludes. Questions around the breadth of the ruling are important – for example, will it cover all tariffs (reciprocal + trafficking tariffs on China/Canada/Mexico) and will it require automatic refunds (which are in now the region of $100bn). A broader ruling that requires immediate and automatic refunds could generate a curve steepening effect on the bond market due to the fiscal impact of having to refund tariff revenues with additional issuance required to fund such an eventuality. For stocks, the more important implication is how much the ETR (which currently sits at around 18%) reduces. It’s highly likely that the Trump administration quickly rolls out alternative tariff measures based on one of the many different authorities available (Sec. 122, 232, 301 etc.)…a good baseline expectation is that an ETR of 15% is quite straightforward to reimpose. Any decrease in the ETR should reduce economic uncertainty, and moreover, represents a small consumption tax cut year-on-year…assuming it is passed onto consumers. In sum, this should be a moderately bullish impulse for risk assets and economic growth. Speaking of growth, the economic data continue to reinforce my view that equities have done a good job of sniffing out the forward cyclical upswing in the US economy in 2026. The final composite PMI for October rose to 54.6 confirming the economy is still expanding at a solid pace, and importantly, ISM services PMI rose to 52.4 from 50.0 returning to an expansionary phase with robust readings in new orders (56.2), prices paid (70.0)…and importantly, a sequential improvement in the employment component (48.2 from 47.2). Labour market data this week showed moderate improvement…with ADP moving back into positive territory (42k from -32k) – despite a high seasonal adjustment hurdle – and initial jobless claims remained steady around 220-230k. The fly in the ointment was the Challenger job cut announcements which showed 153k in October, leading the 12m average to rise to 100k per month from 91k. However, I’m a little sceptical of the signal from this data for a couple of reasons….first, the series is extremely volatile, warning against putting too much weight on any one print…second, Challenger also releases hiring intention data which saw a large rise on a NSA basis…so once we net hiring and layoffs, the signal seems much less concerning as the rise in layoffs is largely offset by a rise in hiring plans on a seasonally adjusted basis (chart below).

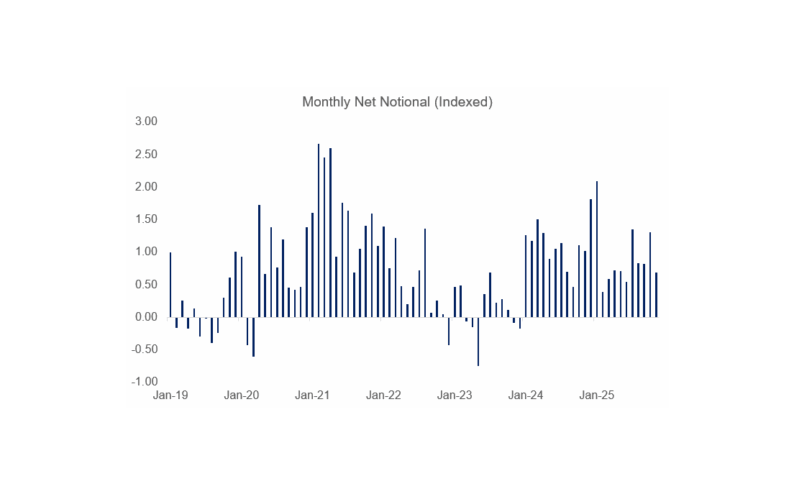

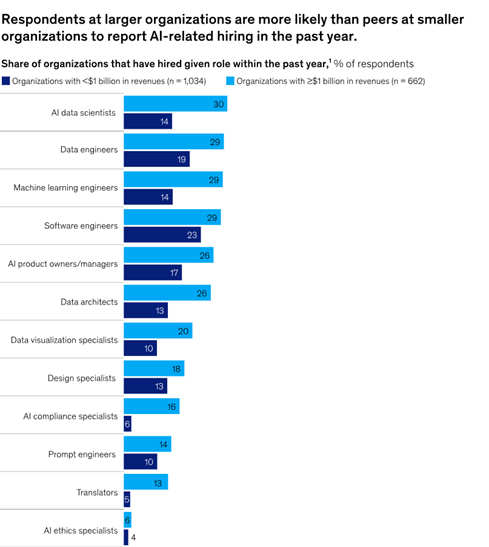

STRUCTURAL NOT CYCLICAL IS QUICKLY BECOMING THE MOST IMPORTANT THEME THIS YEAR…especially when it comes to understanding labour market dynamics. The Trump administration’s drive to curb immigration has had a dramatic impact on labour force supply…strikingly, 1.2 million foreign born workers have left the jobs market from March to Aug this year. This smaller overall labour pool has inhibited jobs growth, especially in sectors heavily reliant on foreign workers such as agriculture, construction and hospitality. With employers competing for a smaller pool, there is a risk of upward pressure on wages if the economy accelerates, especially given the fact that this cohort are often complements rather than substitutes for domestic born workers. Perhaps even more important, structurally lower population growth will reduce trend growth over the medium term…a point I’ve highlighted in recent notes. Of course, the other structural factor that we must grapple with is the impact of AI…on the one hand companies are adopting this technology to enhance productivity and deliver efficiency gains, but the consequences for hiring remain uncertain. In a recent McKinsey survey, 32% of organizations expected a reduction in hiring because of AI adoption, but 43% expected no change and 13% an increase. This is not surprising…whilst it’s likely that efficiency gains for administrative processes will be significant, the balance between AI being a magnifier for growth versus simply creating margin expansion through large scale layoffs of white-collar jobs is unclear. This same lack of clarity is being reflected in the low-hiring / low-firing labour market that has been the mainstay for much of 2025. This represents the current challenge for the Fed…structural changes in the make-up of the US economy are muddying the waters for interest rate policy, which is primarily supposed to address cyclical swings. Both markets and policymakers have come to associate weak labour market data with recessionary outcomes…but aspects of the current landscape do not necessarily imply a poor economic backdrop, just structural change…and in fact, the activity data and stock market performance paint a substantially different picture. Whilst the stock market is not the economy and the Fed’s mandate is not growth…it is true to say that the central bank’s job is to manage the forward outlook and tackle risks on both sides of their mandate.

Source: McKinsey

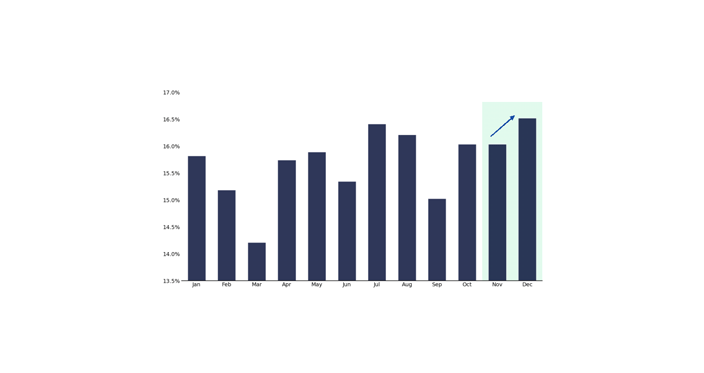

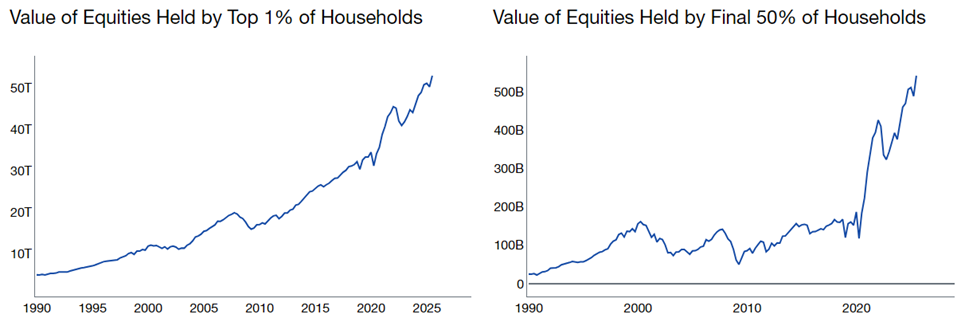

REGULAR READERS WILL BE ACCUSTOMED TO MY BULLISH VIEW on the forward growth outlook, driven by a combination of record levels of FCI easing, pro-cyclical rate cuts, late-cycle fiscal stimulus, and an AI capex spending boom which is growing at an almost incomprehensible rate. This is not a recessionary backdrop, but what some have called a “K-shaped” economy where inequality is growing between those who hold assets and those who earn only from their labour. But the picture is likely more nuanced, especially when looking at gains from the equity market…retail investors now account for 22% of total US equity volumes – they are THE price setters in the market. The top 10% of households have benefitted the most from the rally in stock markets, but this cohort are typically not active traders. Indeed, it is the bottom 50% of households where the wealth impact has been most dramatic in recent years – it has grown five-fold since 2020 (charts below). This participation in wealth creation by the majority cohort of households is important as it offsets some of the lost ground from the K-shaped economy. Economics 101 will remind us that the marginal propensity to consume of this group is much higher than wealthier ones…an important driver of consumption, which has remained robust in recent months…folks spending stock market profits in the grocery store is the narrative. Bory Cox, the CFO of JP Morgan’s Corporate and Community Banking Unit spoke at a conference this week and made some interesting comments on the health of the US consumer based on their credit card and deposits data. She noted “consumers remain generally healthy and resilient, and we do not yet see any material deterioration in their position, whether you’re looking at…cash buffers as a key metric..or whether you’re looking at delinquency trends…and certainly spend. In fact, when we are looking at spend trends, after a relatively softer, although still pretty solid second quarter, we’ve seen strengthening both in confidence, and that reflected in a little bit of strengthening in spend into the third quarter. We’re still early into the fourth quarter, but we continue to see those trends in the fourth quarter as well. When you unpack that, it’s really also in discretionary categories, whether it’s retail or travel and dining.” A regular refrain I hear is that in the K-shaped economy much of consumer spending is being driven by the top percentiles, but the JPM data questions this narrative; Cox goes on to say: “When you unpack it by income bands, and we look at it across four different income categories…there really isn’t any divergence in the trends, whether you’re looking at the level of cash buffers that each income category has…its stable…if you’re looking at delinquency trends, same story…we [also] look at payroll disruptions and how those are trending both in our small business population as well as by income segment. Again, they continue to remain quite steady. Continue to look for it, but it’s a resilient consumer as of right now.” The bottom line is that this is simply not an economy which is showing real signs of distress…which is why policymakers are being cautious about their next moves.

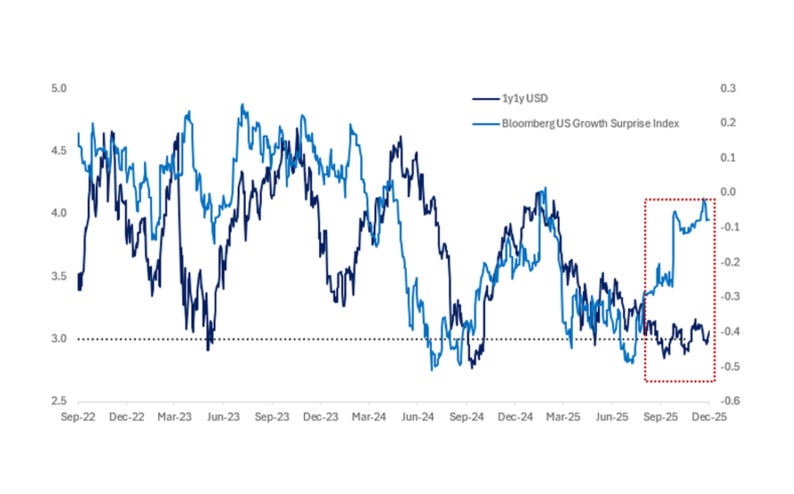

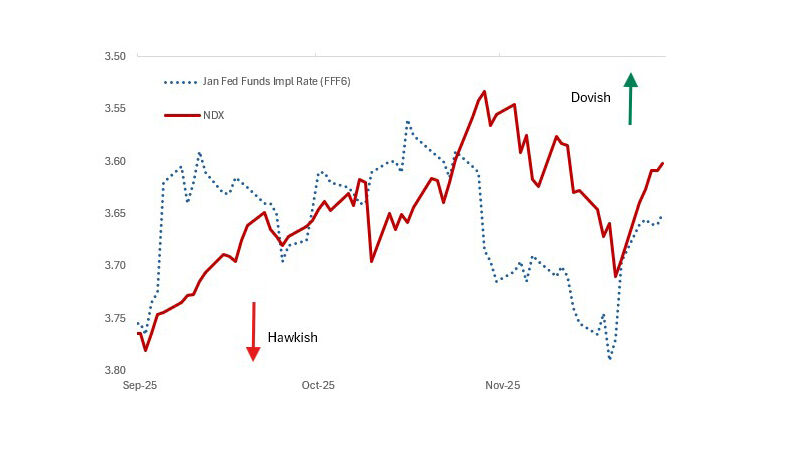

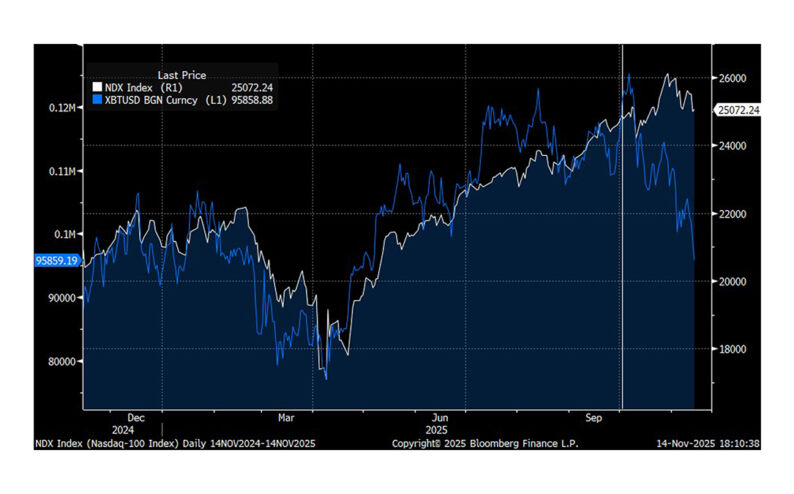

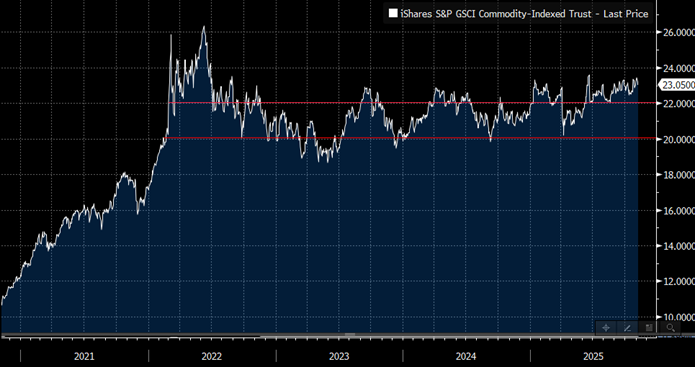

ULTIMATELY, I RETURN TO MY VIEW THAT THE REFLATIONARY NARRATIVE IS LIKELY TO DOMINATE FROM HERE. Inflation is at-risk of rising as easy FCI powers a cyclical uplift in the economy and supply side factors limit economic slack. As I had expected, US yields have started to move higher to reflect this more reflationary landscape, but we should see continued strength in equities as high nominal growth drives earnings momentum. A reflationary rise in yields should not be a risk to equity markets, as long as real rates remain anchored. The driver of yields moving higher is crucial when considering the performance of equities in a higher rates regime – higher rates due to higher nominal growth is a much more risk-friendly backdrop than a rise in yields due to a hawkish impulse…in other words, rising yields signal stronger growth, not restrictive policy. In this environment, cyclical equities should outperform defensives and going into 2026 as nominal growth rises and fiscal spending remains elevated, I would expect more tailwinds to the debasement theme, which should be bullish for commodities. Naturally, a run up in commodities (which appear to be on the edge of a breakout – chart below) would further fuel the reflation theme, especially as data centre power demand starts to push up energy prices. TOO MUCH OF A GOOD THING?

Source: Bloomberg

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Market Insights - What We Do