-

Who We Are

- What We Do

Series: Some Macro ThoughtsSupply Constraints + Cyclical Acceleration = Inflation

By Nohshad Shah

INVESTORS SHOULD APPRECIATE THAT THE POST-PANDEMIC ERA OF IMMACULATE DISINFLATION IS DEFINITIVELY OVER. The re-opening surge that followed the pandemic shutdown – supported by record levels of fiscal stimulus – created elevated demand in the US economy leading to levels of inflation not seen since the 1970s. This strong growth backdrop was met with two things – first, a surge in labour demand…and then supply (supported by swelling immigration under President Biden)…and second, a (delayed) Fed hiking cycle in 2022 to quash said inflation. Though financial conditions tightened, consumption and growth remained solid with supportive fiscal policies. What then transpired in 2023-24 was a drop in inflation without a sharp rise in unemployment…aka immaculate disinflation. The US economy grew at >2.4% (above estimates of trend 1.5-2.0%) for nine of the ten quarters between Q3’22 to Q4’24 whilst core inflation fell from 5% to 3%. A major factor in the high growth disinflation that the economy experienced over that period was the boost to trend growth from immigration. Remember that trend growth is essentially just productivity + hours worked + population growth. Changing immigration policies have injected volatility into population growth…so we now live in a world where trend growth is more volatile than it was historically. This year, we have a much different picture. Curbing immigration has been a top priority for the Trump administration and estimates suggest net migration in 2025 will be close to zero or negative…compared to over +3 million in 2023. THIS IS A HUGE STRUCTURAL SHIFT…dramatically impacting labour supply and leading to the sharp reduction in levels of payroll growth seen in recent months. Market participants have been conditioned to assume that sub-100k NFP is considered weak…when in reality, the breakeven is likely 30-50k. More importantly, with trend growth lower, slack is reduced…and the implications of this are profound…the NAIRU – the unemployment rate that is consistent with stable inflation – is likely to be higher than previously estimated…and the quantum of inflation created per unit of economic growth is higher. Set against the backdrop of loose financial conditions, late-cycle fiscal stimulus, easier monetary policy, and a deregulation agenda designed to boost growth further…inflation risks are greater than markets appreciate – the capacity for the economy to create inflation at ~2% growth is more than it has been in recent years. The Fed has done a good job of taking out insurance in the face of spot labour market weakness. But they may have much less room to cut in 2026 than they realise.

US Growth gap, US CPI gap

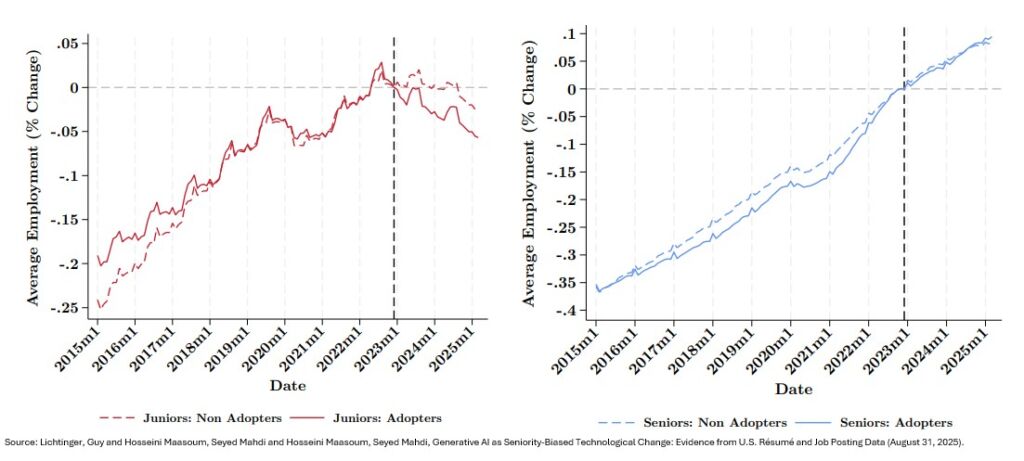

Impact of AI on hiring at Junior and Senior levels

IT IS HUMAN NATURE TO APPLY MORE WEIGHT TO RECENT EXPERIENCE…so I’m concerned that the market is over-indexing to the high growth, immaculate disinflation era – which was driven by structural changes that have not only faded but aggressively reversed. This comes at a time when underlying inflation already sits in the region of 3% (1% above target), leaving very little room for comfort for the Fed. Moreover, if reduced net migration has driven weakness in hiring and labour supply (research shows immigrant labour is a complement rather than a substitute to domestic labour), then weak payroll growth should not be considered cyclical but in fact structural. Any central bank will tell you that monetary policy is designed to address cyclical rather than structural factors in an economy. On that note, a first of its kind study from researchers at Harvard University uses big data (job openings & resume data covering 62 million workers across 285,000 firms) to capture the impact of AI on the labour market. The researchers track companies that hired “generative-AI integrators” and measure how employment changed at these firms vs firms that did not hire them…they found firms integrating AI saw a 7.7% steeper decline in hiring for junior roles relative to non-adopter firms but note no discernible difference for hiring at the senior level and no increase in layoffs (just lower hiring; charts above). As the AI story plays out in coming years, it will continue to muddy the waters for policymakers as it pertains to structural changes in the labour market. If the Fed cuts twice more this year taking policy rates to 3.5%, they will sit just 50bps above their neutral estimate from the SEP’s long-term dot…with underlying inflation above target and a labour market likely to see recovery in cyclical hiring as jobs growth picks up with fading tariff uncertainty, a massive FCI impulse, and front-loaded fiscal stimulus.

US Labour market

Source: Bloomberg, Citadel Securities

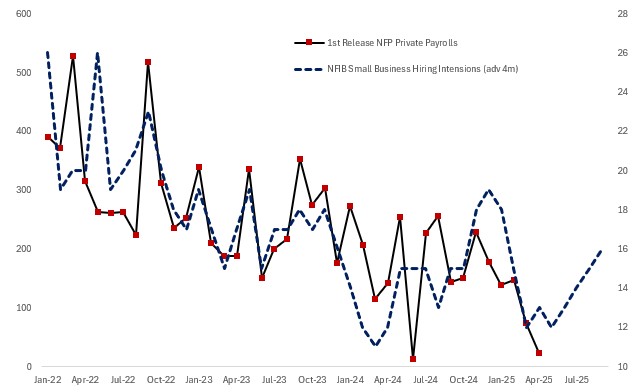

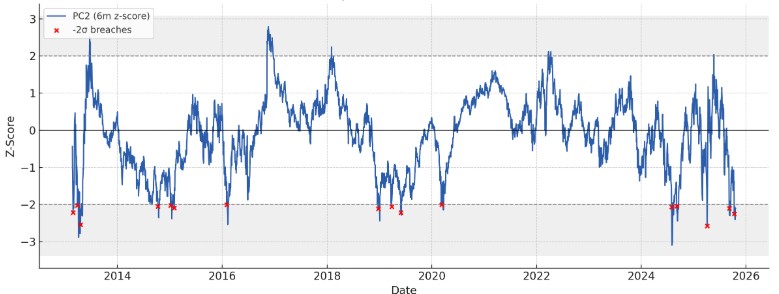

SO, WHAT ABOUT MARKETS? Friday’s core CPI report was perceived by investors to be benign due to a downside surprise in the shelter category. However, I continue to think the market misunderstands current inflation risks…it’s not necessarily tariff-induced…but a more classical inflation process. Each month the market breathes a sigh of relief that inflation didn’t sharply accelerate due to a spike in core goods pricing…but it seems to miss that the slow climb higher in goods prices (68% of components increased in Sep; highest since Aug 2022) comes alongside stickier supercore services sitting at persistently elevated levels and underlying inflation close to 3%…all of which creates a vulnerable starting point for a demand-induced cyclical upswing. Nevertheless, investors will likely only get concerned about inflation once some relief in the jobs data transpires…on that front, it appears that private sector job growth may be sequentially improving based on the evolution of private sector indicators (chart above) in the absence of BLS data. Turning to my favoured FCI framework, since 2000, there have been three instances in which the 6 month easing in FCI-G (Fed’s measure of financial conditions) has reached current levels…2003 (post dot-com), 2009 (post GFC) and 2020 (post COVID)…and every time FCI has loosened this much, inflation has been below rather than above target. In effect, this is the single largest easing in financial conditions relative to the inflation outlook in 25 years (h/t Frank Flight). The Fed seems fine to keep financial conditions easy, despite above target inflation (at least until we’re through any extended labour market weakness) with implied lower forward real yields the result. So far, so good for risk assets. But…if we decompose financial conditions into its macro factors (risk on/risk off + the policy impulse) we find that when the policy factor gets this easy, it tends to tighten back (chart below)…typically led by higher yields in the bond market. Of course, FCI can tighten through many channels: first, stocks….have been nervous in recent weeks, but ultimately if I’m right on the forward growth outlook (bullish), it will be difficult for equities to do the leg work. Second, credit…is highly correlated to broader risk assets, and as I noted last week, might see elevated valuations rejected, but it’s hard to see a meaningful widening if growth remains solid. Fraud may be a concern…and we need to keep an eye on NBFI lending, but it’s likely not a systemic issue. Third, the dollar…is certainly a potential channel, based on valuations and the recent correction in gold prices…but I see too many crosscurrents (hedging of US exposure, diversification, concerns around US institutional independence) to believe in a structural move higher enough to tighten FCI. So…that leaves bonds as the natural release valve – in line with the historical analogues. 10y UST yields below 4% look disconnected to the underlying growth and inflation data and are over-indexed to spot labour market weakness and the perception of an extremely dovish Fed well into 2026. Though the FCI-Inflation gap may persist for some time, bonds may be the asset class to close it.

Policy Factor within the FCI model

Source: Citadel Securities, Bloomberg

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Market Insights - What We Do