-

Who We Are

- What We Do

Series: Macro ThoughtsTail Risks Reduce, but Macro Headwinds Remain

By Nohshad Shah

THIS WEEK SAW A STABILIZATION OF MARKETS…with SPX now around +10% from the lows (8 April) and VIX levels at ~26, having reached double that number at the peak. These moves are largely a reflection of the Trump Administration’s walking back of some of the more extreme pronouncements around both tariffs and Fed independence. On Tuesday, President Trump tweeted that he had “no intention of firing” Chair Powell and Secretary Bessent admitted that a US-China trade war was “not sustainable” and with current tariff rates we’re effectively in a trade “embargo”…something which I had highlighted in this note two weeks ago. All of this represents a reduction in tail-risk for market participants, which is why we’ve also seen a steadying of the price action in US Treasuries. Whilst welcome, this is only a partial reprieve…the economic damage from a re-ordering of global trade and the broader ramifications of tarnishing “Brand USA” should remain at the forefront of investors’ minds.

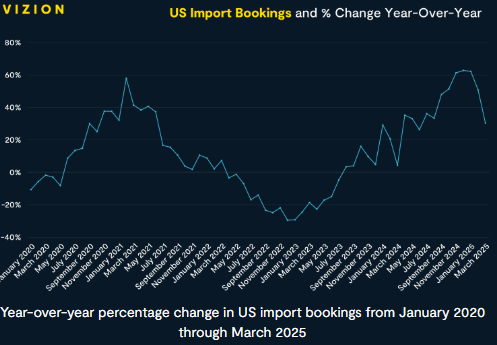

Source: Vizion, 11apr25

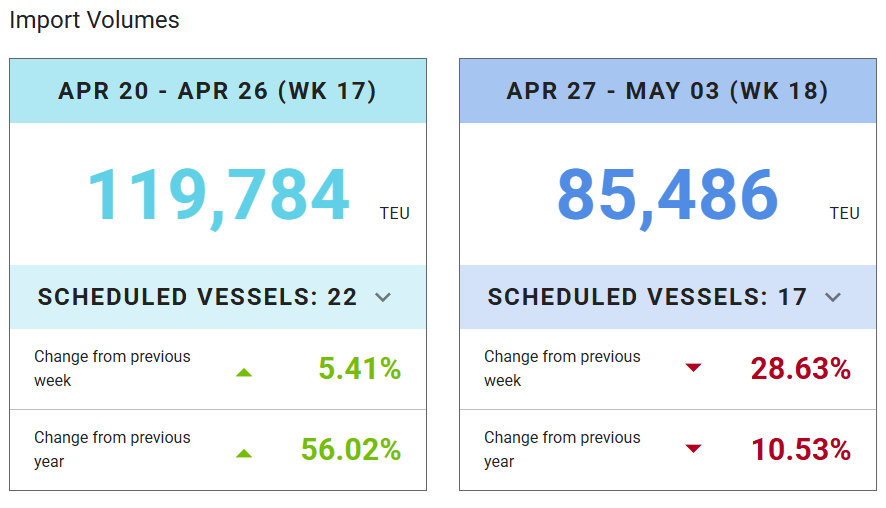

Source: The Port of Los Angeles, Wabtec, 25apr25

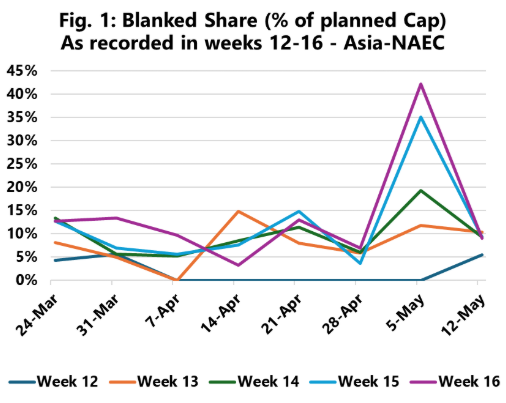

ENTERING INTO A TRADE WAR…with your largest trading partners (all at the same time) has profound implications for both the US and the global economy. Tariffs are a supply-side stagflationary shock…the re-shoring labour-intensive supply chains will come at the cost of higher value-add activities. In the medium-term, a less efficient allocation of capital and labour will lead to lower productivity, lower trend growth and higher inflation…for a given level of GDP growth. But even in the short-term, the supply shock from a shortage of goods is likely to be very substantial, perhaps even Covid-Esque. The impending impact is most clearly observable in US import bookings (chart above; Vizion)…following a surge in Q4’24, we have seen a sharp decline since Jan 2025. This likely represents shippers moving quickly to front-load shipments in anticipation of tariffs…followed by volumes collapsing as uncertainty hits and we’re closer to implementation. Indeed, when looking at The Port of Los Angeles data (above), we can see a 28% week-on-week decline in TEUs (twenty-foot equivalent unit) for the week of 27 Apr, compared to the week prior. Similarly, Sea Intelligence analyses blanked capacity (as a percentage of planned capacity) in Transpacific trade…which shows continued major spikes in blank sailings, going up to 42% in the most recent week (chart below). This is the real-time impact of the current policy landscape – business investment dries up and consumer confidence cracks. The recent strength in durable goods orders likely reflects pre-tariff front-loading…and whilst this can persist into some of the April data, its reasonable to expect a precipitous decline soon, mirroring the shipping data (and indeed weak consumer sentiment). Whilst a change in tone from President Trump may be helpful…and even assuming that there’s a tariff deal with China around the mid 50% mark (20% + 34% reciprocal)…we’re still looking at a minimum effective tariff rate for the US economy of ~17% (versus ~28% under current proposals)…and that’s with a conservative assumption on sectoral tariffs of 10%. This leaves YoY Core CPI at ~4.5% and Core PCE ~4.3% (the Fed’s preferred measure), according to Durham Abric, our inflation expert. Enough to make the Fed more than a little concerned. In my mind, the US administration has likely overplayed its hand and is now left in a position where they’re trying to negotiate trade deals with multiple countries…something that typically takes many months…within a 90-day pause, which itself was forced by market pressure. This is a far-from-ideal negotiating stance.

Source: Sea Intelligence, 24apr25

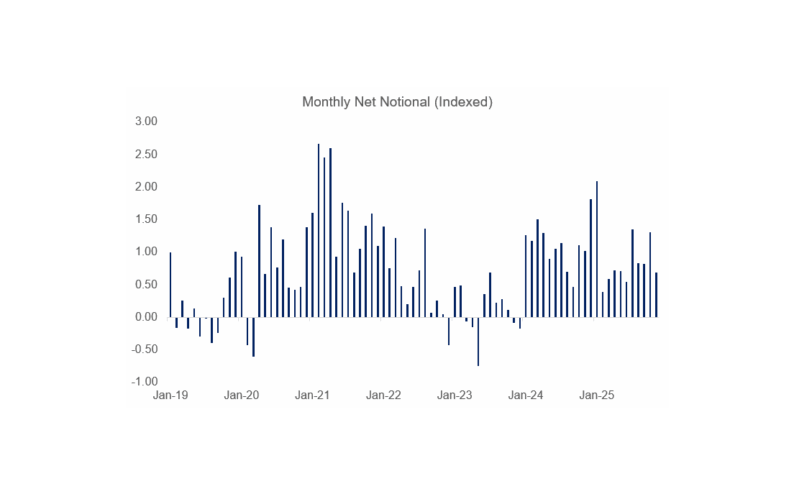

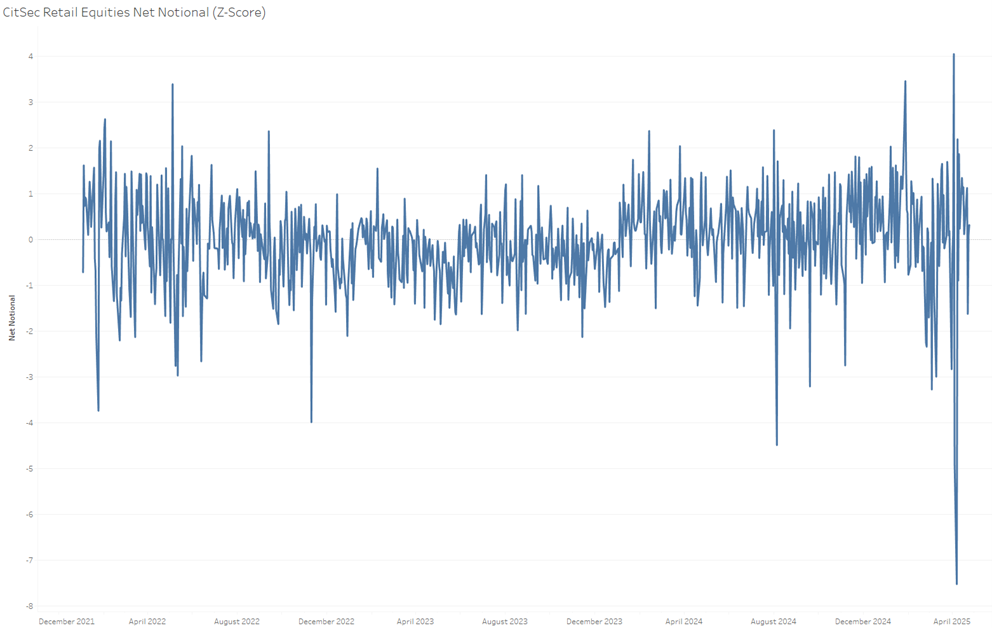

WHERE DOES THAT LEAVE MARKETS? The course correction on Fed independence and tariff rhetoric has sharply reduced the extreme tail risk for markets. Relative to the growth outlook, US long-end rate valuations are attractive – risk-off correlations were neutralized by the combination of increased term-premium and sale of US assets narrative. If those risks are now somewhat diminished, the more traditional dynamic can reassert itself and long end rates can rally materially. The same can be said of UST swap spreads. Month-end should also be supportive. Moreover, there is some expectation in the market for issuance adjustments in the upcoming Quarterly Refunding Announcement (QRA)…whilst it’s difficult to reduce issuance in any meaningful way given the fiscal outlook, there is a chance of a few clever tweaks to take the pressure of long-end bonds, such as more long-end buybacks or hints of a future shortening of WAM. Ultimately, this is yet another reminder that fiscal authorities remain the dominant force in determining market pricing, rather than their monetary siblings…something which I have argued has been the case since the 2020-Covid era. Whilst rates markets can exhibit risk-premium compression, the same cannot be said for equities and fx, in my opinion. We’re still staring down the barrel of a wholesale re-evaluation of global trade and with it the risk of a sharp slowdown in both US and global growth…this is not an environment that’s conducive to valuation multiples and earnings projections, both of which continue to remain elevated. So, whilst we can see sharp rallies at the index level around positive headlines, the medium-term outlook remains challenging, at least until we get much further clarity on where tariffs land (to provide certainty for businesses) and the economic implications thereafter (which will determine Fed policy). Interestingly, our own flows at Citadel Securities continue to show retail buying appetite over recent weeks, after experiencing the largest day of net selling that our retail platform has seen in over three years on 7 April. Since then, in aggregate our retail flows show that net buying has nearly surpassed how much was sold between 3rd and 7th April during much of the tariff-driven volatility (chart below; h/t: Thomas Sozzi). For the dollar, the reliability of the US as a trading partner remains diminished, and with it, investor appetite for US assets. This is not only a natural consequence of less dollars that need to be recycled back due to reduced trade deficits…but also a simple reflection of the fact that US economic growth is likely to underperform in coming quarters under current policies. US exceptionalism is a multi-faceted construct based on a combination of factors – both blunt and nuanced – cheap energy, world class R&D across sectors, global talent, and deep capital markets. Ecosystems are delicate by nature and thrive on a fine balance between their many interconnected parts. Risk it at your peril. I expect the US dollar to remain under pressure. Where there is value is inflation markets…as outlined above, in most tariff scenarios, realized inflation will trend upwards from here…and unless the Fed acts to control this, one can expect inflation expectations to ultimately reflect this. 5Y inflation swaps are at 2.50%, barely above target for the Fed (in CPI terms)…this is largely driven by the fact that inflation tends to trade in correlation to risk assets, which have been under pressure. I believe this represents good medium-term value in most outcomes.

Source: Citadel Securities Internal Data, 25apr25

Source: Bloomberg, 25apr25

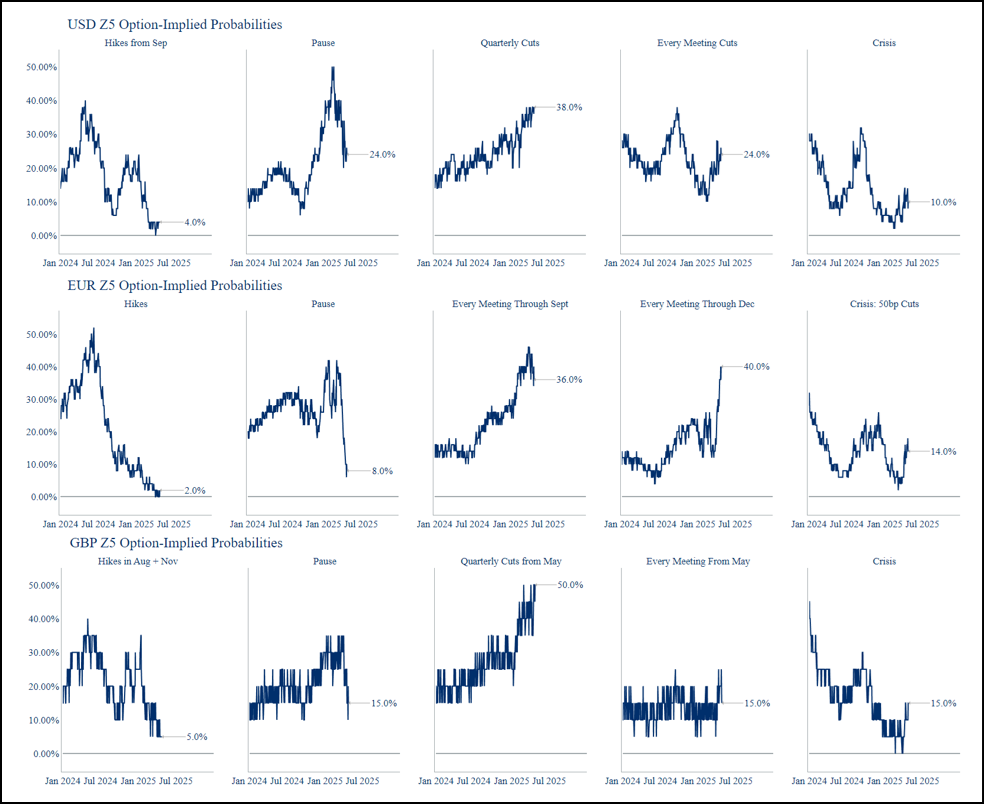

THE FED REMAINS ON THE SIDELINES FOR NOW. The playbook for stagflation is tough…let alone one that incorporates high levels of government policy uncertainty. The market is not incorrect to price 86bps cuts by the end of this year…this is just a weighted average of various plausible outcomes (charts below; h/t: Grant Wilder). Given the landscape outlined above, my sense is that the Fed will wait as long as possible – perhaps through summer – until they have more clarity on tariff policies and the economic implications…knowing they can cut aggressively and deeply should the data warrant. Chair Powell will not want to be the first central banker in decades to lose control of US inflation. Following this week’s back-track, he has the upper hand.

Perhaps more interestingly, the BOE and ECB have a much clearer playbook. Both the UK and Eurozone economies are exhibiting clear signs of weakness, which will only be exacerbated by tariffs and the deflationary impulse from strengthening currencies. Cheaper imports (especially from China), lower input costs and competitive pressure for domestic producers will all contribute to getting inflation back to a comfortable position, allowing central banks to cut rates…first to neutral (UK: 3.5%, ECB 2%)…then to accommodative territory. Both central banks are sounding dovish, and I would expect the BOE to cut 100bps in short order (the most compelling opportunity, relative to market pricing) and the ECB to continue their downward trajectory well through 2% (currently 2.25%) in coming months.

Source: Citadel Securities, Bloomberg, 25apr25

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Market Insights - What We Do