-

Who We Are

- What We Do

Series: Some Macro ThoughtsThe Biggest Risk Taker

By Nohshad Shah

THE FUNDAMENTALS OF THE US ECONOMY REMAIN SOUND…with this week’s retail sales data (control group 0.5% vs 0.3% exp.) suggesting a resilient consumer and initial jobless claims trending lower at 229.5k (4-week moving avg.) reflecting a stable labour market. Inflation continues to remain elevated with the combination of Core CPI (2.9% YoY) and PPI, leaving estimates of the upcoming Core PCE at 2.7% YoY, which is still meaningfully above the Fed’s 2% target. Tariff pass-through is starting to show up in Core Goods inflation, which came in at 0.20% MoM, materially stronger than last month (-0.04%), reflecting rising prices in clothing, appliances, and furnishings – much of which is imported. All told, when looking at the annualised trend in Core CPI (chart below), it’s clear that the disinflationary trend has not only stalled but is now turning upwards – something I have been concerned about for some time. Similarly, 1y CPI inflation swaps have rallied over 40bps this month to 3.50% (chart below), suggesting a market concerned about the pipeline of tariff inflation that is building up and expectations of pass-through that are more widespread. Given this inflation backdrop…with stocks at all-time highs…the easiest financial conditions (FCI) we’ve had in almost three years…and an upcoming large positive fiscal impulse…this is not an environment where the Fed should be cutting rates. Chair Powell agrees and has been steadfast in his view that policy rates should remain unchanged until there is a clearer picture. As I’ve argued before, in recent years the US economy has become accustomed to a higher level of policy (and long-end) rates and can sustain itself accordingly…so current policy rates are not all that restrictive. With Powell’s Fed, do not expect rate cuts anytime soon…

Source: Haver, 18jul25

USD 1y ZC Inflation Swap

Source: Bloomberg, 18jul25

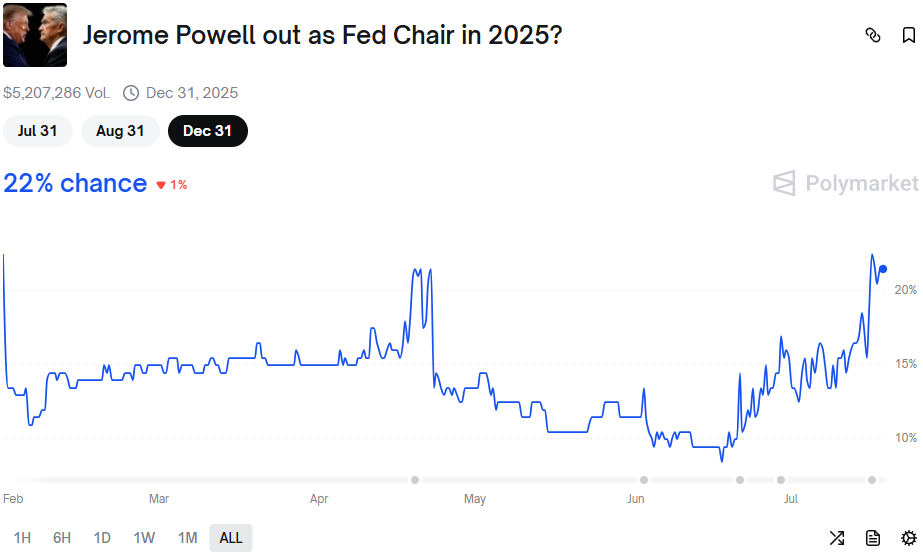

THE RISKS TO THE US ECONOMY AND ASSET MARKETS DO NOT EMANATE FROM FUNDAMENTALS, BUT FROM PRESIDENT TRUMP’S POTENTIAL REMOVAL OF CHAIR POWELL AND EROSION OF THE FEDERAL RESERVE’S INDEPENDENCE. Polymarket odds of this happening rose as high as 30% on Wednesday following reports that the President had floated the idea with Republican lawmakers. Whilst he followed this with a denial of anything imminent in an Oval Office presser, I’m concerned that this is not the end of the matter – an independent central bank is structurally at odds with what I suspect is President Trump’s view that POTUS should control all levers of government, including the ability to set interest rates. This is reflected in his continued and escalating criticism of Powell on social media and the desire for rates to be three percentage points lower than they are now. Make no mistake, this is still a very live issue…and will have profound implications for markets should it materialise. For investors, Central Bank independence is sacrosanct and the core pillar of US and global markets. This is largely because operating without political interference implies a high level of credibility, allowing central bankers to do the right thing for the economy regardless of politics. It’s exactly this credibility which has allowed the Fed to step into the fray in various crises…the GFC of 2008-9…the COVID pandemic…and numerous other times when the global financial system has needed a liquidity backstop. If this credibility were eroded, the Fed’s ability to insulate the global economy from these shocks would be severely curtailed, leading to a structurally more volatile environment…both for the economy and markets.

Source: Polymarket, 18jul25

SO, CAN POWELL BE REMOVED? I found the language from President Trump telling: “I don’t rule out anything, but I think it’s highly unlikely, unless he has to leave for fraud, and it’s possible there’s fraud”. In my mind, this likely represents a pivot by the Administration away from trying to fire Powell directly but instead looking to dismiss him for “cause”. As a reminder, in May the Supreme Court specifically signalled that the Fed would be shielded from a broader review of President Trump’s ability to fire officials of independent agencies: “The Federal Reserve is a uniquely structured, quasi-private entity that follows in the distinct historical tradition of the First and Second Banks of the United States.” Accordingly, the emphasis has now shifted to a clause in the Federal Reserve Act of 1913, which allows the Chair to be fired for “cause”. This could give the President an avenue to oust Powell, ostensibly not for his rate policy, but for wrongdoing. Administration officials have been highlighting cost overruns of $600-700mio for the $2.5bn renovation of the Fed’s Eccles building in Washington, D.C., as a potential excuse. The Fed Inspector General was made aware of the extra costs as well as some changes made to the designs of the building following approval by the National Capital Planning Commission (NCPC) in 2021. The Fed’s recently updated Q&A on their website does not dispute that some changes to the plan were made, but ultimately, the decision on whether there was a breach of process will reside with the NCPC following any investigation into the matter. Intriguingly, just ten days ago, three new members were appointed to the NCPC – James Blair (White House Deputy Chief of Staff), Will Scharf (WH Staff Secretary), and Stuart Levenbach (Aide in the Office of Management & Budget) – all heavyweight Trump loyalists, serving on a relatively obscure planning board. Time will tell if the intention is to use this mechanism to remove Powell – and the legality, or otherwise, of it. Or indeed, if it is simply a way to exert pressure for a resignation. This is uncharted territory, so there is little legal precedent, but one would assume that the process would involve some form of official letter from Trump following an investigation…then a legal challenge from Powell for unfair dismissal. Crucially, it remains unclear if Powell would remain in post throughout the process. What is clear, however, is that the market impact would be dramatic – we had a preview when Wednesday’s news broke…front-end yields rallied 13bps (SFRH6) whilst 30y bonds sold off 11bps, reflecting a twist of the yield curve. At the same time, both the US dollar and equities sold off sharply. These moves were an entirely logical reaction…a move to oust Powell would create lasting harm to the US economy, destabilising inflation expectations and leaving it open to significant outflows across all asset classes. Indeed, if we extrapolate a continuation of such moves, we could easily see 30y bond yields head towards 6%, a further 7-10% correction in the broad dollar index, and 5-10% correction in equities…and that would be in an environment where front-end yields would be sharply lower in expectation of imminent rate cuts. Moreover, as the inflation-busting credibility of the central bank gets eroded, I would expect breakeven inflation to widen significantly…even more so given the likely ~20% total depreciation of the currency YTD, resulting in forward imported inflation…in addition to the tariff-induced shock. Inflation expectations would almost certainly become unhinged, and a new Fed Chair would have their hands full – not only with this environment, but also a likely divided FOMC. And this is the crucial point – eroding the independence of the Fed has no meaningful economic upside…policy rates are only one tool in a complex ecosystem which is delicately maintained by central bankers (and the Treasury), buttressed by credibility. President Trump’s objective of reducing interest rate payments on debt would not be met, given the likely sell-off in long-end bond yields…something which would have profound implications for the broader functioning of the US and global economies. In tandem with the US, it’s likely that 30y bond yields across major economies would rise at a time of reduced structural demand for duration, accelerating concerns around debt sustainability and potentially engineering a global recession. In sum, it would be one of the largest acts of economic self-harm in recent history. So why would President Trump embark upon a route that would cause such damage to the trust and confidence of US institutions – the mainstay for the global economy and markets for much of the last century? Because he is a massive risk-taker. Looking back through Donald Trump’s history, one can easily observe an outsized appetite for risk…whether in real estate, the media, or politics. Sometimes it has worked, other times not…but in sum, it has brought him to the Presidency of the United States of America…twice. Since taking on the Presidency, he has continued in this vein, taking large gambles across the spheres of international trade, geopolitics, and fiscal policy. Like all risk-takers, he can quickly “stop out” of trades at any point. Let us hope in this case he does. Otherwise, all bets are off.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Some Macro Thoughts - What We Do