-

Who We Are

- What We Do

Series: Macro ThoughtsThe Fed Recalibrates

By Nohshad Shah

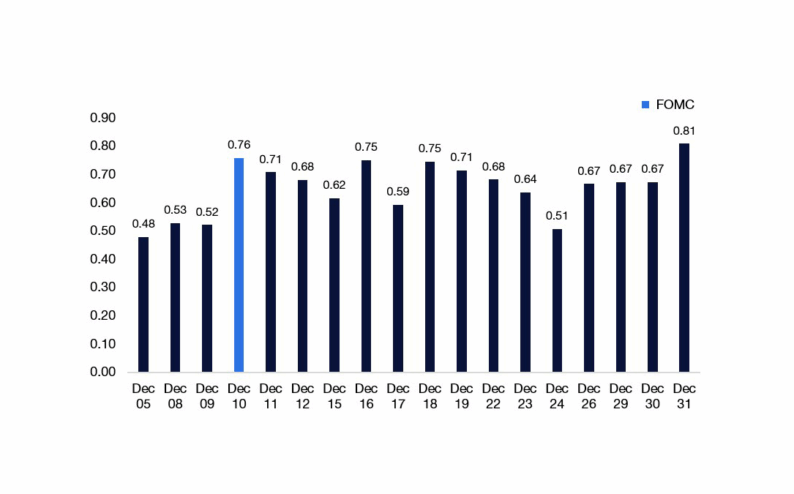

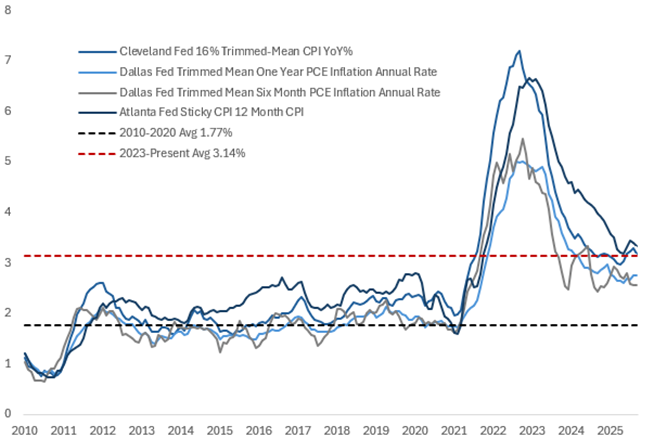

FED CHAIR POWELL STRUCK A HAWKISH TONE THIS WEEK AT THE FOMC PRESSER…despite delivering an expected 25bp cut to policy rates. Specifically, he chose to highlight that a December cut was “not a foregone conclusion” and noted “strongly differing views” on the committee, suggesting both significant pushback to more rate cuts and likely further dissents to come (we had two this time – on either side of the divide). With the phrase “when you are driving in the fog, you slow down” he flagged to markets that we might soon be coming to the end of this phase of insurance cuts. Whilst it’s been clear since September that Powell wanted to undertake a series of rate cuts given labour market concerns, my view has always been that markets were wrong to extrapolate this well into 2026…and it now seems that even the December meeting remains undecided. This should come as no surprise given the macroeconomic backdrop. The Fed’s primary mandate – the labour market – is showing signs of stabilisation…weekly ADP data (+62k in Oct; rise in private hiring) and initial claims (~220k; far from recessionary levels) suggest ‘breakeven’ levels of payroll growth…and our own labour market tracker displays improving job creation, albeit from weak levels. As I’ve been highlighting for some time, the biggest story in the labour market has been the large reduction in net migration and its impact on the supply of workers…a structural not cyclical factor…which Powell acknowledged in his comments: “a big part of the whole story is that supply side”. On the inflation front, he sounded far too sanguine in my view – underlying inflation is running at ~3%, already a full percentage point above target and well above the pre-pandemic average of 1.77% (chart below). Moreover, whilst the FOMC seems committed to overlooking tariff impacts on goods, services inflation remains at elevated levels and on some measures is even accelerating (e.g. Supercore Services Ex Housing). With financial conditions the easiest they have been in years, late cycle fiscal stimulus incoming and AI capex surpassing all expectations…it’s no surprise that the Fed are carefully considering their next steps. If economic growth picks up (as I expect), then with employment slack less than most anticipate, a rise in hiring could quickly lead to demand-induced inflationary risk – a big problem given the starting point. The committee seems to be shifting in the direction of Governor Hammack…who has been most concerned about inflation risks. December’s FOMC meeting seems ‘in-play’.

Source: Bloomberg, Federal Reserve Banks (Cleveland, Dallas, Atlanta) Citadel Securities, Oct-25

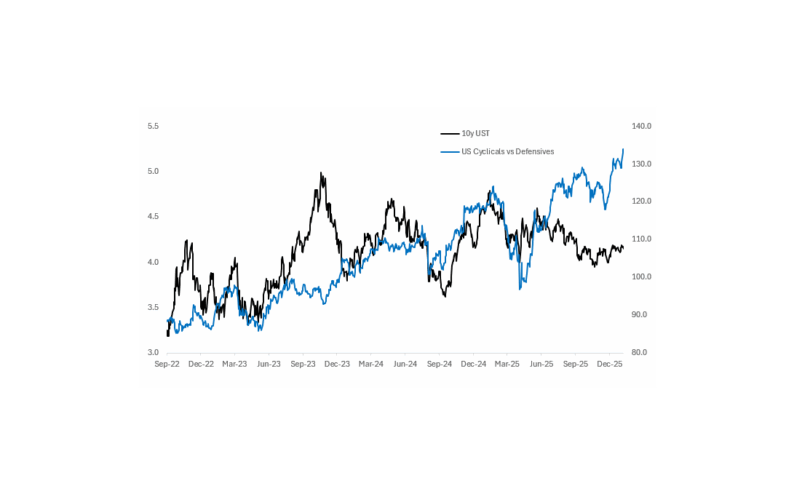

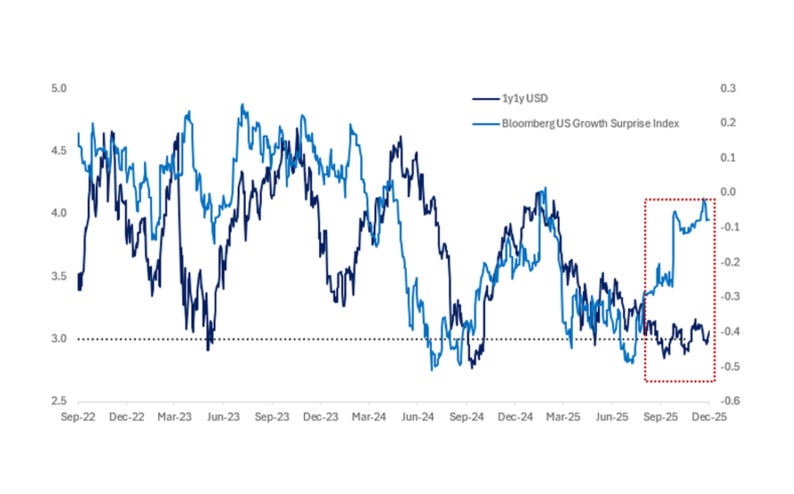

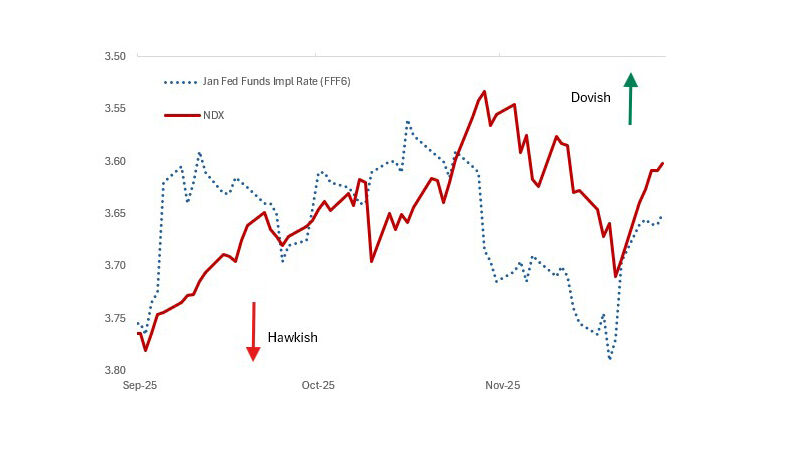

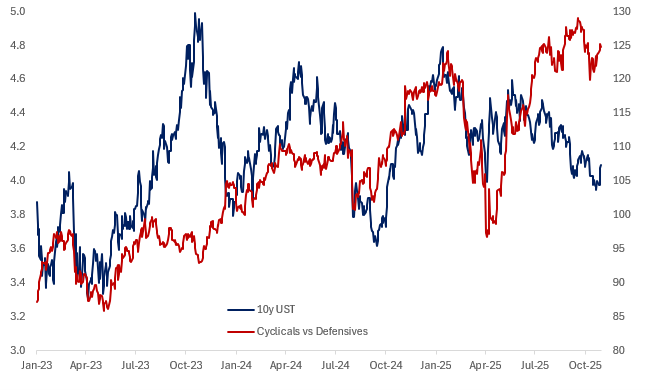

ONE OF MY OFT-STATED VIEWS IS THAT EQUITY MARKETS HAVE BEEN PRESCIENT ABOUT THE POSITIVE FORWARD GROWTH OUTLOOK AND EARNINGS EXPANSION FROM AI INTEGRATION…whereas bond markets have over-indexed to spot labour market weakness and the expectation of an overly dovish Fed reaction function. This week’s FOMC meeting was a timely reminder that a persistently dovish Fed is not a done deal and the subsequent sell-off in rates was overdue given rich valuations – something I wrote about last week. As mentioned, long-end rates are acting as the release valve for FCI. If we take estimates of the relative weights of stocks vs bonds embedded within a typical FCI framework, then make some assumptions around continued equity market performance, we can back out how much 10y rates need to move to keep FCI constant. Using Scott Rubner’s historical seasonality estimates – SPX typically rallies 3% from November through to year end – FCI would ease a further 14.5bps, other things equal…but to keep FCI the same, 10y yields would need to rise 32bps. As a reminder, the recent 6m easing in financial conditions has been especially large…I’d even say post-recessionary in nature…with the ~70bps of easing worth approximately the same in terms of real GDP impact. The natural next question is: if 10y rates selloff 30-40bps, is that a problem for equity markets? A sharp, violent move higher in yields would certainly be disruptive…but my sense is that a steady move higher due to reduced concerns around unemployment and economic growth (rather than immediate inflation risks) – from rich valuations – would not be harmful to corporate earnings growth and momentum.

Source: Bloomberg, Citadel Securities

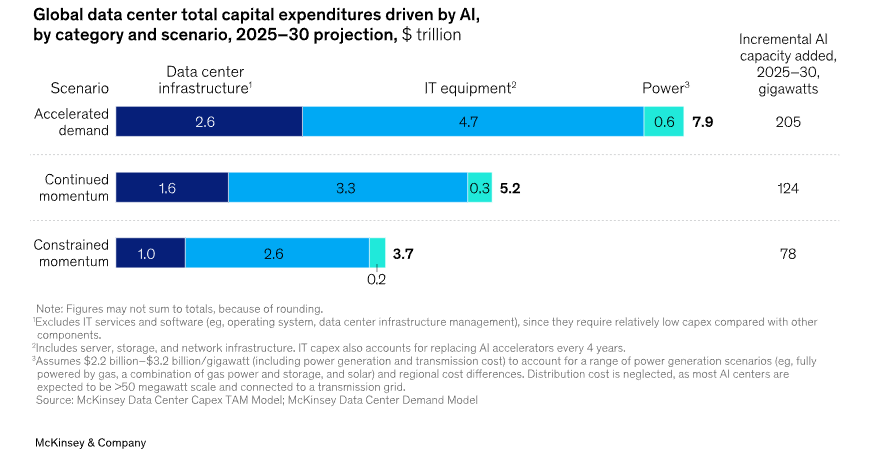

AN IMPORTANT PUSHBACK TO THE BEARISH DURATION VIEW IS THAT AI WILL BE A LARGE DEFLATIONARY FORCE. This is a big call to make…whilst it’s certainly possible in the long-term, the short-term impacts remain unclear and are not yet enough to be a market driver. For now, the capex and associated data centre build out may have the opposite effect on rates markets. Take for example this week’s $30bn bond issuance by META…which was 4.5x oversubscribed and the 5th largest IG issuance in history…whilst easy to brush off by looking at subscriptions, if these deals keep coming, investors should be open to the idea that IG issuance will weigh on global bond duration. The scope of this theme shouldn’t be underestimated…we are on track for the largest amount of IG issuance in history for the month of November, as well as the largest Q4 issuance month ever. Escalating capex volumes could lead to a flood of bond issuance that the market finds increasingly tough to digest. Whilst it’s hard to pin down an exact number, estimates for 2026 IG issuance look like they will be in the region of $1.6-1.7tn, likely an increase of around 5-10% YoY. An interesting McKinsey study suggests that the investment requirement into AI data centres could potentially reach $7tn by 2030…that’s an extra $1.4tn per year (including 2025) or the equivalent of nearly an entire year of US IG issuance. Of course, not all of this will be debt funded, but bond bulls should beware that as AI investment proliferates beyond the hyperscalers, there will be less earnings from which to fund capex, which means more debt. More debt means more duration…and we already sit at rich valuations. There is an additional concern Jeff Eason highlights: the expected ROI of AI capex projects will not be deterred by a 25-50bp change in cost of capital…something Chair Powell himself referred to. Watch this space.

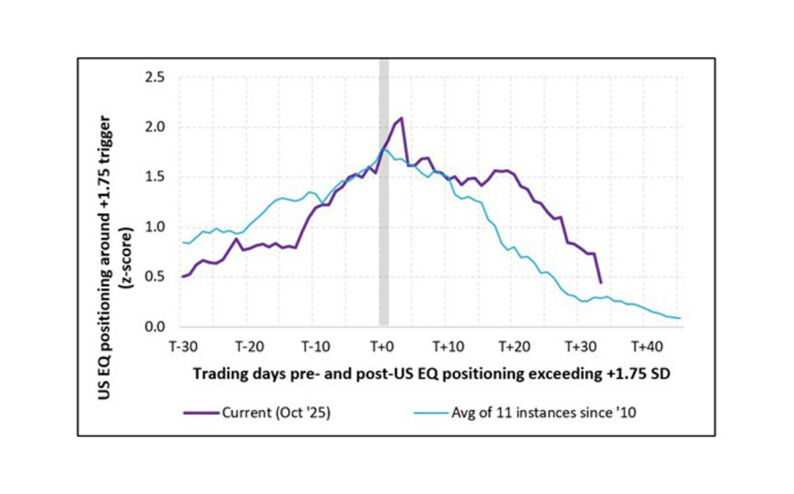

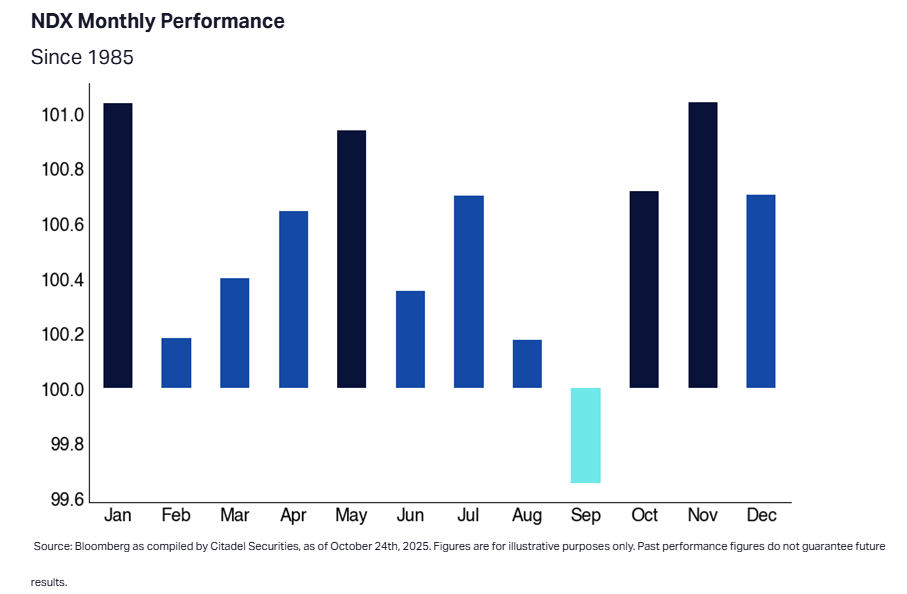

BLOW OFF TOP…is the phrase Scott Rubner and I have been using the most to describe the equity markets outlook (including in our Cross Asset call). Alphabet, Meta, Microsoft and Amazon all beat Q3 EPS estimates and each lifted guidance for AI capex spend, reminding us that these companies see this as existential to their future operating model. Scott flags some key upside factors: the previously mentioned seasonality analysis suggests the risks are tilted towards a powerful rally through to the end of the year. The Nasdaq has risen 12 of the past 13 Novembers (averaging +3.8%!), and our franchise flows show 26 consecutive weeks of net bullish retail option demand (remember this community is THE price setter in the market now). US corporates are also on pace to authorize a record $1.3 trillion in buybacks this year…once reporting season ends, the buyback window reopening is a historically supportive flow dynamic, and with vol resetting lower our systematic models predict mechanical re-leveraging demand. This all comes at a time when institutional discretionary exposure remains light, creating the risk of investors getting ‘stopped-in’ to buy as the market grinds higher. These bullish undercurrents in our flow of funds analysis coincide with a macro context that needs to rerate growth higher. The labour market looks to be improving…we have the composite tailwind of fiscal and monetary stimulus in the pipeline (combined these could be worth between 1-1.65% of GDP depending on which estimates you take)…risk appetite indicators aren’t stretched…and we are about to go through the Wall St economic forecast season during which every “year ahead outlook” will need to ask the hard question of why they’re assuming a persistent drag from tariffs and uncertainty when retail risk appetite is this ferocious and our flow metrics are euphoric.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Market Insights - What We Do