-

Who We Are

- What We Do

Series: Macro ThoughtsThe Upside Case Emerges

By Nohshad Shah

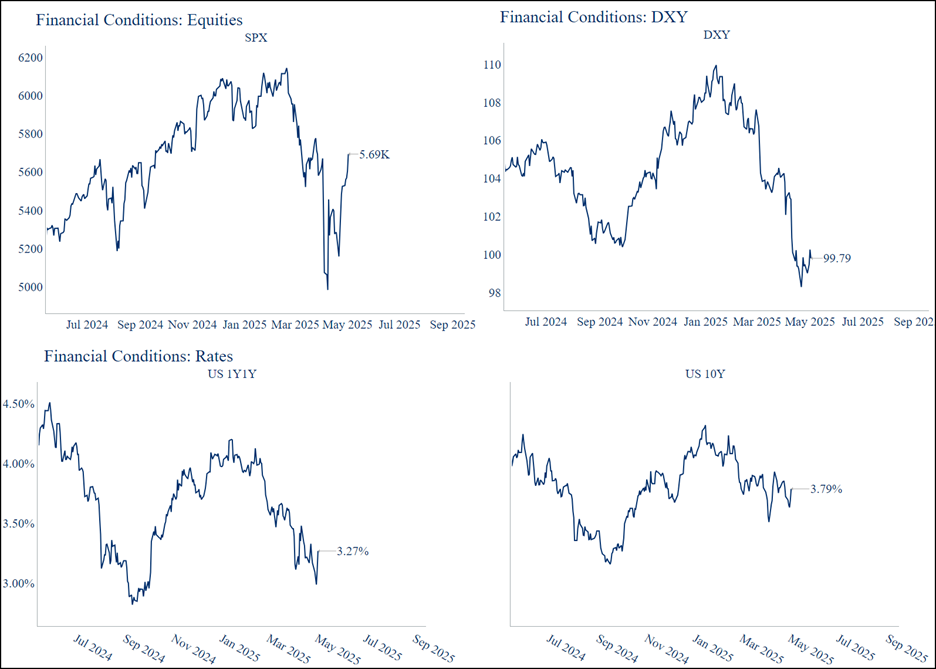

EQUITY MARKETS CONTINUED TO PERFORM STRONGLY…with SPX erasing the entirety of losses driven by “liberation day”, rallying a full 14% from the lows. At this juncture, one could argue that Oil, DXY (broad dollar index) and 1y1y US rates are pricing in a US recession…whilst the equity market certainly is not. What’s going on? Using a Financial Conditions Index (FCI) framework is intuitive here…having tightened sharply at the beginning of the month after the tariff announcements, it has now eased all the way back to unchanged (chart below). Looking under the hood, we can learn much more by analysing which assets have driven the move. In rates, the market initially applied a higher risk-premium to bonds, reflecting the stagflationary impulse from tariffs – lower trend growth and higher inflation. Given the large factor-weighting of 10y rates in FCI, this had a dramatic tightening impact on financial conditions…which is logical given the importance of long-end yields in the US economy. Effectively, this was a tightening impulse via the rates channel that cut in the opposite direction to the re-rating lower of growth. At the same time, equity markets sold off sharply, reflecting both uncertainty around business investment and margin compression, further tightening conditions – a classic “growth re-rating” that would normally have seen bonds rallying. As the Trump Administration course corrected on tariffs with the 90-day pause and on Fed independence, the bond premium has compressed again, allowing for an easing of FCI via the US asset/term premium channel, as evidenced by the stock-bond correlation persisting (rates rallying/spx rallying). This is important, because the correlations (up till Thursday) suggest the market has not upgraded growth expectations for the US economy…instead, it has simply removed the initial hawkish monetary impulse, allowing FCI to ease. Importantly, looking forward if we do get a further “normalization” of the tariff agenda (perhaps towards an effective tariff rate in the mid-teens) and the US economic growth outlook improves…then there is materially more upside to risk assets because tight FCI is now no longer a problem.

Source: Bloomberg, 02may25

Source: Citadel Securities, Bloomberg, 02may25

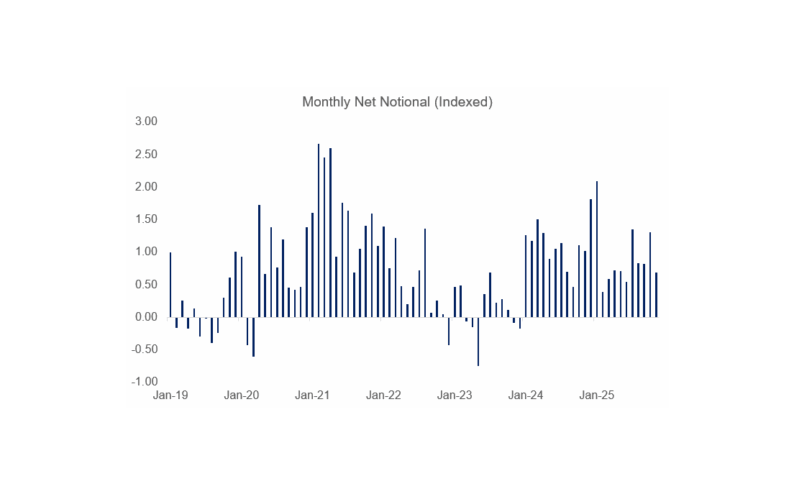

THIS WEEK BROUGHT SECRETARY BESSENT’S INAUGURAL QUARTERLY REFUNDING ANNOUNCMENT (QRA). Despite some market expectations of adjustments to favour long-end bonds or a shortening of WAM, Bessent chose not to alter the mix, keeping the line “Treasury anticipates maintaining nominal coupon and FRN auction sizes for at least the next several quarters”. The broader challenge here is the lack of demand for long-end bonds, something which is becoming structural to the US Treasuries market. With the absence of QE and foreign central banks (and private investors) reducing their appetite…as well as the new heightened focus on the implications of re-ordering global trade – reduced demand for US dollars, US assets and higher inflation – not to mention the continued increase in fiscal deficits, this is a problem that is not going away anytime soon. As I’ve mentioned before, keeping 10y rates controlled is a crucial aspect of ensuring US economic growth remains on track…as a former hedge fund manager, Scott Bessent will be as familiar as anyone with the FCI framework. So how to ensure long-end yields remain controlled? One potential avenue is to cut policy rates aggressively with a good old-fashioned recession (not straightforward, more on this below), reduce deficits (unlikely and undesirable ahead of mid-term elections) or utilize extra-normal tools to create a greater incentive structure for investors to buy USTs. In recent years, the combination of a highly-regulated banking sector, plus record amounts of issuance to fund fiscal deficits has left the market reliant on leveraged buyers of US Treasury bonds – hedge funds and the broader shadow banking sector. This just a just a natural consequence of the current structure of markets and regulatory backdrop. Recent wobbles have shown that this is not without risk…so the open question for policymakers remains as to whether they should act to adjust the incentive structure in a favourable way for market participants to create greater demand.

THE NARRATIVE AROUND TARIFFS IS SOFTENING…with signs of a thawing of tensions with China who’s officials stated that the US had “conveyed messages to China through various channels, expressing a desire to engage in discussions” and “China is currently evaluating this”. This follows last week’s comments from the US Administration suggesting a desire to move forward with negotiations. Interestingly, China has quietly exempted some US goods from tariffs to the tune of $40bn worth of imports (24% of Chinese imports from US) to reduce the impact on their economy…effectively mirroring President Trump’s exemption for smartphones and electronics from reciprocal tariffs. Large scale exemptions like this represent an easy path to soften the impact on both economies and are likely a pre-cursor to trade talks. Moreover, there are early signs of a deal with Japan, potentially in June…the first time a date has been set for any trade deals since the 90-day pause was announced. Talks with India seem to be progressing and even the EU have been making strides to address the current impasse with Trade Commissioner Maros Sefcovic suggesting “certain progress” towards a deal with ~EUR 50bn on the table. In my mind, the nature and scale of the early deals will likely be replicated across the board for most countries…so it’s something to watch closely. On China, I can see a scenario where overtures turn into a deal…something like 10% universal + 50% headline with large exemptions for sensitive consumer sectors…pretty much the levels President Trump had intimated on the campaign trail. This would reduce the effective tariff rate for the US economy…rolling it back closer to levels the market had originally expected prior to 2 April. As per my statement from a few weeks back “the market is the greatest self-correcting mechanism in the world”. Investors tend to deploy a forensic analysis for every aspect of the macro economy and asset pricing…something that is typically warranted. But sometimes, this means that you can lose sight of the big picture and not have the imagination to expect extreme outcomes (think brexit, covid, svb). I would argue that this is a risk here – in the same way that President Trump announced a dramatic attempt at re-ordering global trade one month ago in the Rose Garden without a detailed plan around how to execute the plan and its true implications…he could just as easily roll back much of it very quickly and conclude the whole saga. This is not a prediction, but certainly an increasingly probable outcome.

THE FED? As I’ve been consistently stating since re-starting this note in January, the backdrop of substantially above-target inflation, highly uncertain outcomes with respect to tariffs…and a starting point for the labour market that is close to full employment…is not one where the Fed will want to act pre-emptively to ease. With risks to both sides of the dual mandate, the messaging from Chair Powell and the core of the FOMC has been very clear – they are on hold, until they can assess where tariffs land and the true economic implications. The spot data just isn’t weak enough to warrant cuts…Friday’s NFP report leaves the 3m avg. at 155k and u/e rate at 4.2%. At a minimum, the Fed will need two weak labour market reports (and Claims data to reflect the same) before changing course. At that point, they can act decisively and quickly – but we are not there. The US economy will experience a supply-side stagflationary shock…the depth of which remains unknown until we find a landing zone for tariffs. Lower productivity and trend growth with higher inflation is the result…a la Brexit. My view has been that they will remain on hold through summer, then look to address the prevailing outlook and respond at that time. Ultimately, the recent upheaval in decision-making atop the US government has allowed the market to call into question their credibility. Not so, for the Fed…investors continue to treat them as the adult in the room.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Market Insights - What We Do