-

Who We Are

- What We Do

Series: Macro ThoughtsThe Upside Risk Comes Into Sharper Focus

By Nohshad Shah

THE MARKET HAS TAKEN A MAJOR STEP TOWARDS RE-RATING US GROWTH. Last week I noted that FCI (financial conditions) had eased substantially from the peak, largely driven by a normalization in the initial hawkish monetary impulse stemming from elevated risk-premium in bonds following Liberation Day. And I argued that if there was more good news on tariffs, there was further to run in the repricing of US cyclical growth, given FCI tightening is no longer a constraint. This is exactly what has started to play out this week. The equities up / yields up / dollar up triumvirate reflects a market that is re-rating the forward path of growth higher with asset price correlations confirming that a “growth up” theme was driving the market. The news flow has compounded the early signal that equity markets sniffed out (as usual before the rest of the macro markets)…with an ongoing softening of the US administration’s stance on trade resulting in a UK-US deal and Geneva trade talks with China (more on this below). Market participants have remarked at the loose/bare bones nature of the UK deal and the two-sided risks relating to the Geneva talks. However, this sentiment was not matched by the price action, which in my view is justified with the current information set. These deals and talks suggest that i) the worst is behind us, ii) agreements can be quick and “in principle” and iii) don’t require (any) concessions on sticking points like VAT or other non-tariff barriers. Markets are forward looking, and whilst there are still hard yards to cover, such progress is driving the growth upgrade as it reduces uncertainty. Furthermore, as the tails of the most extreme outcomes have been curtailed in recent weeks, the market has rightly focused on the fact that given the starting point of the US economy (Q1 core GDP 3%, U-rate 4.2%), we are unlikely to enter a full-blown recession. If uncertainty continues to dissipate, the hit to growth will be much less than most investors expect. Given defensive positioning in both equity and rates markets from the macro community, some might not want to hear it…but there is more upside to risk-on here.

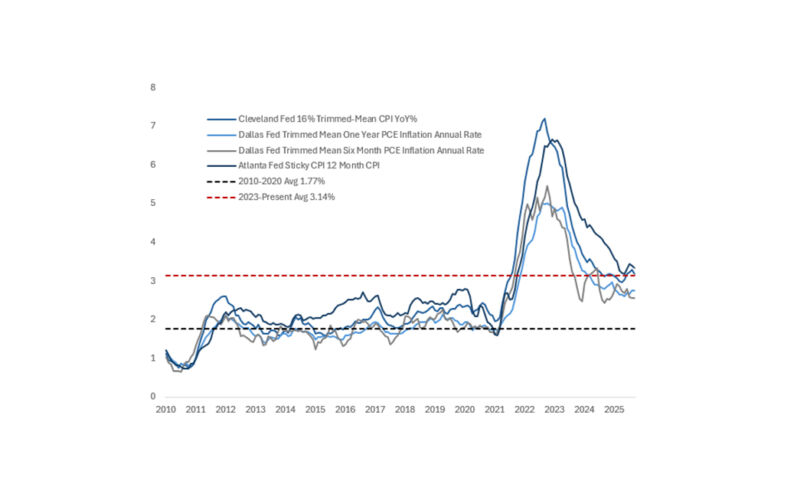

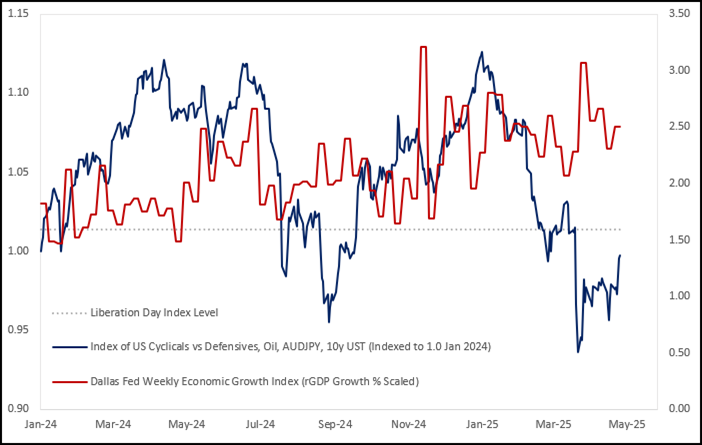

Source: Dallas Fed, Bloomberg, 09may25

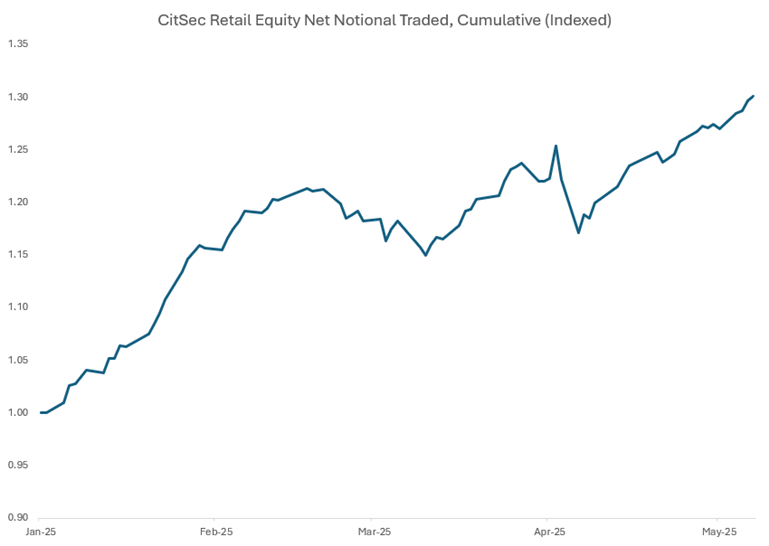

If we take a few common proxies for growth…Oil, AUDJPY fx, Cyclicals vs Defensives and 10y UST…then index and average across them, we can derive a simplistic market-based growth factor (chart above). This indicates that the market is re-rating growth…with potentially further to go, should headwinds continue to recede. The pushback will be that the soft data has been very weak, and the hard data is about to turn extremely sour as we move beyond front-loading and the true tariff impacts come to the fore. This may well be the case…but it’s crucial to remember that asset markets are forward looking, so the emphasis will always be on the 6m outlook…on that front, we are in a much better place than two weeks ago. And if the outlook improves, so will the soft data. This has been an unloved rally in stocks given reduced discretionary positioning, low systematic leverage and depresssed (though rapidly improving) sentiment. Whilst most clients have reduced risk in equities in recent weeks, retail investors have been consistently adding exposure – data from our market-leading US equities franchise (where we execute ~25% of daily equity volumes) suggests continued buying throughout April, except for a few days following Liberation Day (chart below).

Source: CitSec Internal Data

TURNING BACK TO TRADE…April data on China exports showed an increase of +8.1% YoY, likely reflecting substitution effects with other Asian countries instead of the US – perhaps strengthening China’s hand in upcoming discussions. We got an insight into what deals will look like with the one agreed with the UK on Thursday…10% across the board with exemptions for specific sectors. Be in no doubt, this was not a fully-fledged trade agreement…indeed it was just the broad outlines of one, reflective of the time pressure. As argued last week, the likely outcome in many of these trade deals is likely to be a headline number (10% universal for most friendly countries) with large scale exemptions for consumer-sensitive sectors. In the case of the UK, this leaves the effective tariff rate below 10%, which can be considered moderate, under the circumstances. For China, there are hopes of a deal this weekend with Secretary Bessent leading negotiations with Chinese officials in Switzerland…the expectation is for tariffs to be lowered to ~50% (levels President Trump spoke about on the campaign trail) with exemptions. Whilst some of this is “in the price”, I would still expect equity markets to rally should a deal be announced this weekend…simply from the reduction in uncertainty…and looking at cross-asset pricing, front-end rates look dislocated, given the footprints of the growth upgrade elsewhere.

FOR POLICYMAKERS, MODERATE TARIFFS ARE A TRICKY OUTCOME. If we continue down this path in coming weeks (a big IF), the risk is that the economic damage is not great enough to crush growth completely…whilst at the same time, supply chain disruptions could lead to short-term inflation shocks (c.f. Mannheim Used Car Index +4.9% YoY; highest since Oct’23)…and traded inflation and inflation expectations could be at-risk of de-anchoring – without a recession there is unlikely to be enough economic slack to solve the inflation problem. The Fed knows this, which is why they remain on hold. For some time, I have been of the view that given tariffs are a supply-side stagflationary shock, the FOMC will be challenged on both sides of their dual mandate, so will not act pre-emptively (in reaction to weak soft data), but will wait until they have certainty on tariffs and their economic impact (not to mention risks emanating from upcoming fiscal policy), knowing they can cut quickly and deeply should they need to. Chair Powell confirmed this in Wednesday’s presser with the comments “not a situation where we can be pre-emptive because we actually don’t know what the right response to the data will be until we see more data” and “we have a record of [moving] quickly when that’s appropriate. But we think right now the appropriate thing to do is to wait and see how things evolve”. Ultimately, I can see a scenario where tariff negotiations continue in a positive direction (largely because the Administration seems boxed-in at this point)…and those outcomes don’t crush growth but are inflationary…then President Trump shifts emphasis onto the pro-growth part of his agenda, namely deregulation and tax cuts. That’s not an environment in which I can see the Fed cutting rates meaningfully.

Having spent time at the Milken conference this week, what struck me is the depth of commitment from long-term capital allocators to US assets. There was a palpable sense that the innovation, dynamism, and intellectual firepower embedded within US companies is second to none. Investors have spent decades getting to know these firms and the many stewards of capital they invest through – and it has been a phenomenal experience – so unlikely to change anytime soon. Moreover, there was a sense that over a multi-year horizon, President Trump’s attempt to re-order trade will be a blip, when compared to the core factors that will likely drive economic growth. Indeed, even if there was a greater desire to allocate more capital to other large blocs like the EU, the capital markets infrastructure (securitization, VC firms, asset managers, private credit, PE, etc.) simply does not exist in anywhere near the same size to accommodate large scale investment…a total of $16tn sits in EU deposit accounts! Beyond this, the AI revolution that’s coming (with accelerating timelines) will dramatically change the way all businesses function…the first layer will be gains in efficiency in processes…but the greater innovation will be through agentic AI and companies (and perhaps industries) that are yet to emerge. This will have a dramatic impact on productivity and serve as an amplifier to economic growth as the monumental R&D spend from mega tech reaps dividends. Investors will not want to miss out.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Macro Thoughts - What We Do